Early Wednesday morning, the Mortgage Banker’s Association (MBA) announced that refinancing activity declined 20% from one week earlier. Adjusted for the Labor Day weekend, total mortgage applications dropped 13.5% from the previous week. Consistent with the dramatic upward movement in interest rates, refinancing activity is down 71% since it peaked during the week of May 3, 2013.

Why Do We Monitoring Refinancing Activity?

When homeowners refinance, a couple outcomes can occur that pump more dollars into the economy.

First, with a refinanced mortgage, owners may choose to take equity out of the home, allowing for large purchases like vehicles or even home remodeling. CoreLogic recently reported that 2.5 million more residential properties have returned to positive equity in the second quarter of 2013 alone.

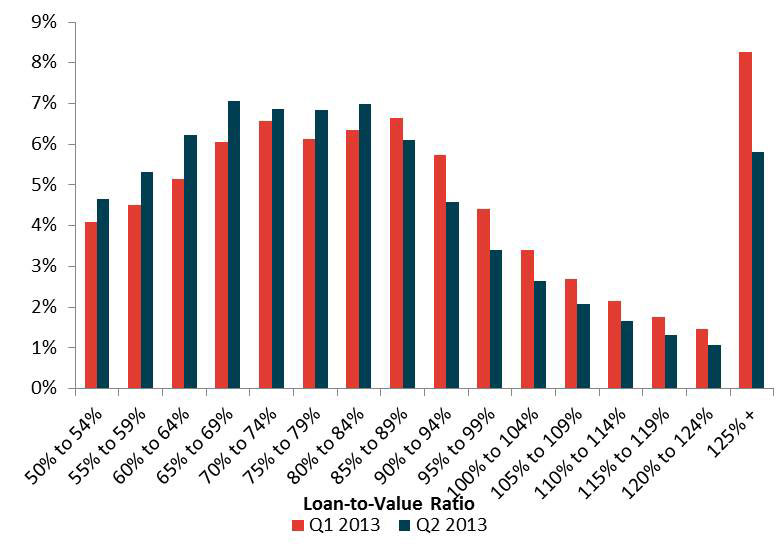

Image Source: CoreLogic

The total number of mortgaged residential properties with equity currently stands at 41.5 million, while houses “underwater” came in at 7.1 million homes for the period (down from 9.6 million in the first quarter of 2013). CoreLogic added further detail regarding the composition of residential properties with positive equity:

“Of the 41.5 million residential properties with positive equity, 10.3 million have less than 20 percent equity. Borrowers with less than 20 percent equity, referred to as “under-equitied”…Under-equitied mortgages accounted for 21.1 percent of all residential properties with a mortgage nationwide in the second quarter of 2013. At the end of the second quarter of 2013, 1.7 million residential properties had less than 5 percent equity, referred to as near-negative equity.”

Though there are still a large number of homeowners that owe 25% more on their house than what it is worth (see large bar to the right in image above), the distribution continues to shift to the left (as housing prices rise). Said differently, the housing “ATM” is starting to replenish itself, as equity builds in more and more residences across the country. Cashing in at the housing “ATM” is one way refinancing activity stimulates the economy.

Another way comes from interest-rate savings, which enable homeowners to use the “saved” dollars on home remodeling/improvement or for other consumer spending. Homeowners can simply spend more on durables and consumables when they have to allocate less of their earnings to mortgage interest costs.

With interest rates rising, however, the ability for homeowners to extract interest savings is substantially reduced, which is why mortgage refinancing activity has hit a large speed bump (as interest rates have risen quite a bit). It’s possible that the lion’s share of refinancing activity has already occurred (at levels below current interest rates) since mortgage interest rates sat near historic lows for a number of years.

Primary Mortgage Market Survey (PMMS)

Image Source: http://www.freddiemac.com/news/finance/?intcmp=AFMREH

How Does the Decline in Mortgage Refinancing Activity Impact Banks?

Declining refinancing activity will impact large originators such as JP Morgan Chase (click ticker for report: ) and Wells Fargo (click ticker for report: ), which may see related fee income face pressure. However, with higher interest rates, banks should experience higher returns on new investments and wider spread income. However, investors have to be cognizant of banks’ large securities portfolios that may need to be marked down under a significantly higher interest rate environment. And, of course, the relationship between short- and long-term rates cannot be ignored.

Though we don’t hold any large bank individually on the basis of these four reasons here, we do hold shares of the Financial Select Sector SPDR ETF (click ticker for report: ) and the SPRD S&P Bank ETF (KBE) in the portfolio of our Best Ideas Newsletter for diversification and valuation reasons.

Valuentum’s Take

Declining refinancing activity could be a slight economic headwind going forward, but we think housing purchases have a stronger economic multiplier, and fundamentals driving housing remain strong. Interest rates are unpredictable to a degree, especially since the Federal Reserve remains imprecise with respect to the end of its bond-buying program. However, we think our Best Ideas Newsletter portfolio is well-positioned for any interest rate environment.