Key Takeaways:

· US housing prices are on the rise…and in a big way, according to the most recent data from S&P’s Case-Schiller Index.

· The “wealth effect” (people feeling better about their financial situation) and increased household formation (thanks to improving employment trends) will have a tremendous impact on spending across the US economy, bolstering the fortunes of companies ranging from appliance makers and building-materials suppliers to aggregates firms and investment banks.

· Our favorite housing-related plays in no particular order: Whirlpool (WHR) thanks to higher appliance sales, United Technologies (UTX) via its residential HVAC exposure (indirectly, we like its aerospace exposure, too), Louisiana Pacific (LPX) on valuation, Ford (F) due to increased contractor activity, and diversified financials exposure: Financial Select SPDR ETF (XLF) and the SPDR S&P Banks ETF (KBE) due to enhanced loan performance and capital markets activity.

· That said, we continue to believe the best ideas in the market are held within our Best Ideas portfolio and Dividend Growth portfolio, respectively. We recently added protection (via put-option exposure) to our Best Ideas portfolio and are looking to add a few new dividend growth gems to our Dividend Growth portfolio. For more details on our recent portfolio moves, please see here: “The Market Doesn’t Go Straight Up.”

Tickers mentioned: BLK, BBY, SHLD, HD, WHR, UTX, IR, LII, JCI, LOW, LL, MAS, DEL, LPX, USG, HGG, AMZN, TGT, SNE, WMT, SWK, CX, VMC, MLM, F, GM, TM, HMC, TSLA, AZO, ORLY, AAP, XHB, DHI, JOE, KBH, LEN, MDC, MTH, NVR, PHM, RYL, SPF, TOL, JPM, WFC, BAC, PNC, STI, USB, C, XLF, KBE, MS, GS, AAPL, MSFT, INTC

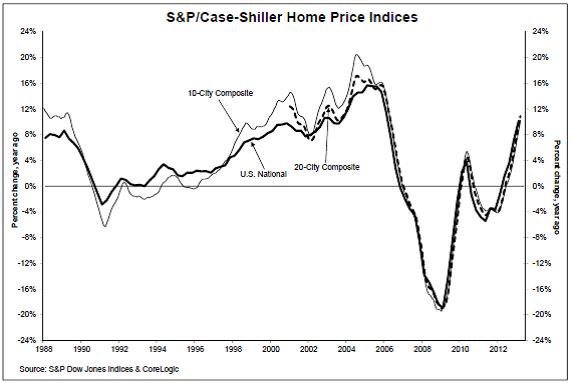

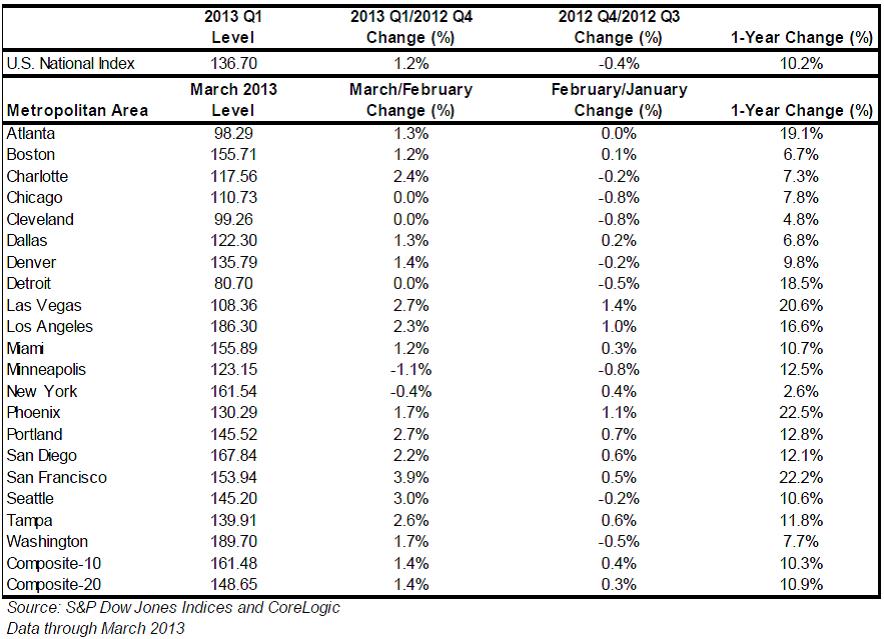

Housing Takes a Huge Turn Upward in March

After a half-decade of uneven price retreats, declining interest rates, and a whole lot of litigation, the US housing market appears to be on solid footing. In fact, one could argue the bull market is back in housing, especially after March home prices jumped 10% year-over-year as measured by S&P’s Case-Schiller Index (both for the 10-city and 20-city composites).

Image Source: http://www.standardandpoors.com/servlet/BlobServer?blobheadername3=MDT-Type&blobcol=urldocumentfile&blobtable=SPComSecureDocument&blobheadervalue2=inline%3B+filename%3Ddownload.pdf&blobheadername2=Content-Disposition&blobheadervalue1=application%2Fpdf&blobkey=id&blobheadername1=content-type&blobwhere=1245352206396&blobheadervalue3=abinary%3B+charset%3DUTF-8&blobnocache=true

Even more impressive: virtually all of the metro markets measured by Case-Schiller showed robust price increases, with Las Vegas, Phoenix, and San Francisco all showing prices up over 20%. Las Vegas and Phoenix were some of the hardest hit cities by the recent real estate bubble, so prices are still well below previous all-time highs (so an even greater retracement can be expected in coming periods).

Image Source: http://www.standardandpoors.com/servlet/BlobServer?blobheadername3=MDT-Type&blobcol=urldocumentfile&blobtable=SPComSecureDocument&blobheadervalue2=inline%3B+filename%3Ddownload.pdf&blobheadername2=Content-Disposition&blobheadervalue1=application%2Fpdf&blobkey=id&blobheadername1=content-type&blobwhere=1245352206396&blobheadervalue3=abinary%3B+charset%3DUTF-8&blobnocache=true

The Drivers Behind Improving Housing Fundamentals

We’ve long been bullish on the US housing market recovery (see the January 2012 edition of our Best Ideas Newsletter here), and there are several factors that have contributed to our bullish stance.

Increased Affordability

The Federal Reserve’s low interest rate policy driven by unlimited quantitative easing (QE) has had a tremendous impact on the US housing market from several angles. For one, low interest rates have diminished the attractiveness of holding cash and government debt significantly. The current 10-year Treasury note yield sits at approximately 2%, but that is after languishing in the mid 1% range since July of 2012.

In fact, there is reason to believe the real yield on most Treasury debt instruments is negative (even as yields move higher). We believe these low interest rates have spurred home purchasing from both individuals and investors.

Individuals

For many individuals, it’s almost a no-brainer to re-finance a mortgage payment at the lower rate, or for a new buyer to borrow at such cheap rates. Money has become so “cheap” that the market is drawing individuals who may have preferred to rent, simply because the cost savings are too compelling. Trulia released an interesting study showing that purchasing a home–after factoring in low down payments, the mortgage interest deduction, and even home maintenance–is cheaper than renting in almost every market in the United States. The following is some pretty compelling data (Image Source: Trulia).

Investors

While the cost of money is driving trends in homeownership (which have returned to levels last seen in 1995-1996: Residential Vacancies and Homeownership in the first quarter 2013, US Census Bureau), it is also drawing investors’ interest. The yield on most debt instruments, even junk-rated debt, is so low that buying rental properties has become a source of yield for large investors. Asset manager Blackstone (click ticker for report: ) has spent over $4.5 billion on housing purchases during the past year alone. Such buying action likely wouldn’t impact the stock market much, if at all, but with Blackstone and other asset managers chasing distressed housing, it has had a positive impact on housing price performance.

Falling Unemployment

The national unemployment rate continues to fall (7.5% in April 2013, down from a peak of 10% in October 2009), and we’re also seeing improvement from one of the largest impediments to the recovery in housing: youth and young adult unemployment. As the table shows below, unemployment in the critical 20-24 age group has fallen to 13.1% in April of this year (the latest reading) from 14.2% in January—still elevated, but it has declined more than a percentage point in but a few months!

Image Source: Bureau of Labor Statistics

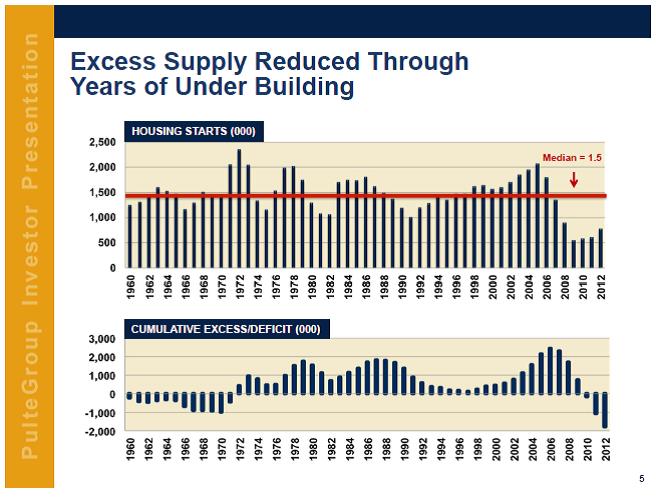

Improving Household Formation

As more people in this age group move out of their parents’ homes and into their own places (and maybe get married), household formation (raw data), which advanced by 490,000 in March 2013 from the same month a year-ago, should continue to be positive and perhaps accelerate in coming months. Importantly, years of underbuilding have left a significant cumulative deficit of homes (see bottom chart).

Image Source: PulteGroup

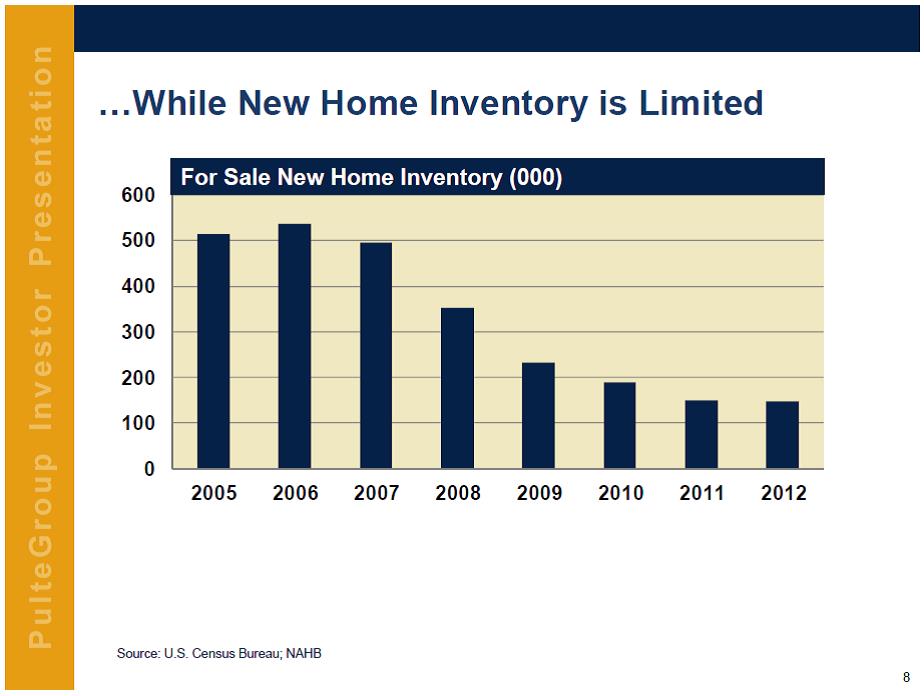

Limited Inventory

Pent up demand has already been accruing for years, and new home inventory is limited, which makes for an environment conducive to driving further housing price improvements (as a result of simple supply/demand dynamics). Though we acknowledge the concept of “shadow inventory”—sellers currently without a ‘for sale’ sign in their front yard—overall inventory trends continue to move in the right direction.

Image Source: PulteGroup

First: Housing Derivative Ideas

Higher housing prices as a result of a “wealth effect” coupled with increased household formation will have a tremendous impact on spending across the US economy. People feeling better about their financial situation due to higher housing prices will be a driver behind residential remodeling activity, while new household formation thanks to more favorable employment will inevitably drive upgrades or amenities within a new residence.

Appliances

Appliance sales have recovered nicely in recent quarters, and we believe major appliance sellers such as Best Buy (click ticker for report: ), Sears (click ticker for report: ), and Home Depot (click ticker for report: ) will continue to benefit. Whirlpool (click ticker for report: Categories Member Articles