Image Source: Digital Realty Trust Inc – Third Quarter of 2021 IR Earnings Presentation

By Callum Turcan

On October 26, Digital Realty Trust Inc (DLR) posted third quarter 2021 earnings that beat both consensus top- and bottom-line estimates. The data center real estate investment trust (‘REIT’) saw its GAAP operating revenues come in at $1.1 billion (up 11% year-over-year) and its non-GAAP core funds from operations (‘FFO’) per share come in at $1.65 per share (up 7% year-over-year) last quarter. Digital Realty also increased its guidance in conjunction with its latest earnings report, which we appreciate, as that signals the REIT is growing confident that it will exit 2021 on a high note.

Digital Realty’s business is steadily recovering after taking a meaningful hit during the initial phases of the coronavirus (‘COVID-19’) pandemic. We continue to like shares of DLR as an idea in both our Dividend Growth Newsletter portfolio and our High Yield Dividend Newsletter portfolio (more on that here). Shares of DLR yield ~3.0% as of this writing and in our view, the REIT has ample room to grow its payout going forward as its financial performance bounces back from the subdued levels seen in 2020.

When taking into consideration Digital Realty’s ability to tap capital markets at attractive rates (something we cover in this article), we give the REIT a “GOOD” Dividend Safety rating as its adjusted Dividend Cushion ratio is near parity at 0.7, which factors in expected dividend growth over the coming years. Additionally, we give Digital Realty a “GOOD” Dividend Safety rating, underpinned by its bright cash flow growth outlook. The top end of our fair value estimate range sits at $186 per share of DLR, well above where Digital Realty is trading at as of this writing.

Guidance Boost

Digital Realty recently boosted its full-year guidance for 2021 and now expects to post $4.4 billion-$4.425 billion in total revenue (up 13% from 2020 levels at the midpoint) and $6.50-$6.55 in core FFO per share (up 5% from 2020 levels at the midpoint) this year. Please note that Digital Realty has adjusted its 2021 guidance several times so far this year, and that its current outlook represents a nice improvement from the guidance it put out back in February 2021.

Balance Sheet Update

When Digital Realty announced a secondary equity offering in September 2021, shares of DLR initially took a hit though its stock price has since recovered, even in the face of rising interest rates. Once the forward sale agreements associated with the secondary offering has been completed, something that is expected to occur by March 2022, Digital Realty will have raised ~$1.0 billion net through this offering.

The REIT had $14.1 billion in total debt outstanding, inclusive of short-term debt, at the end of September 2021. As a capital market dependent entity, Digital Realty is constantly issuing debt and equity to raise funds to cover its refinancing needs, growth ambitions, and to keep making good on its payout obligations. For instance, in July 2021, Digital Realty issued the equivalent of ~USD $0.6 billion in Swiss “green bonds” with a weighted-average coupon of just under 0.4% and a weighted-average maturity of roughly 6.6 years. Based on recent capital market activities, we see Digital Realty retaining solid access to debt and equity markets at attractive rates going forward.

Image Shown: Digital Realty’s debt maturity schedule remained well-staggered at the end of September 2021, which should make future refinancing activities easier to manage. Image Source: Digital Realty – Third Quarter of 2021 IR Earnings Presentation

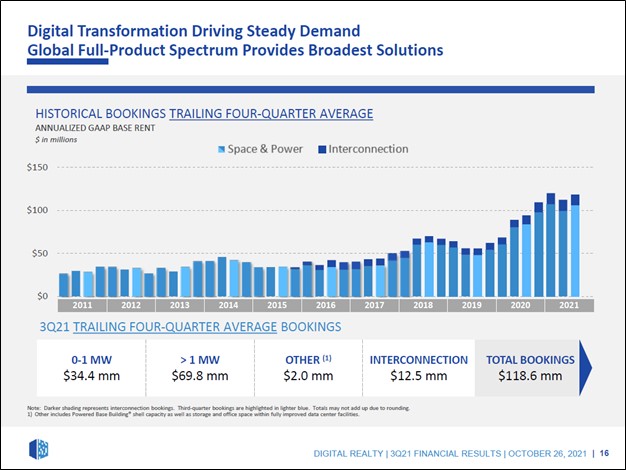

Bookings Performance Coming in Strong

Digital Realty’s bookings performance has held up well in recent quarters as it concerns both signing new leases and renewing existing leases. As we have noted in the past, Digital Realty faces headwinds from legacy leases expiring as it concerns its rental rate performance, though those headwinds should eventually fade.

Last quarter, the REIT signed total bookings that are expected to generate $113 million in annualized GAAP revenue, which includes a $12 million contribution from its interconnection offerings. Additionally, the REIT signed lease renewals worth $223 million in annualized GAAP revenue last quarter, though its cash and GAAP rental rates both rolled down by single-digits as legacy leases were replaced.

Image Shown: Digital Realty has done a solid job securing new business and renewing existing leases in recent quarters. Image Source: Digital Realty – Third Quarter of 2021 IR Earnings Presentation

International Expansion

We covered some of Digital Realty’s international growth ambitions in our September 2021 article Digital Realty Is a Stellar Income Growth Idea (link here) and encourage our members to check out that article. In this note, we will focus on new developments that have been announced since that article was published.

Digital Realty closed its India-focused joint venture with Brookfield Infrastructure Partners LP (BIP) last quarter. In our view, this joint venture should significantly extend Digital Realty’s growth runway given India’s promising growth outlook as its economy continues to modernize. Currently, Digital Realty does not own or operate any data centers in India.

Early on in the fourth quarter of 2021, Digital Realty announced it had made a strategic investment in AtlasEdge Data Centres which is billed as “a European edge data center provider.” Additionally, Giuliano Di Vitantonio (Executive Vice President, Strategy & Business Segments at Digital Realty) is set to become CEO of AtlasEdge starting in January 2022. Here is what the press release announcing the deal had to say:

AtlasEdge delivers seamless, localized and ultra-low latency digital infrastructure through an extensive network of more than 100 facilities across Europe located close to consumer and enterprise end users, at the edge of the last-mile network. The company aims to serve the growing demand from cloud providers, streaming services and enterprises for high-performance, scalable and secure facilities through which they can distribute low-latency applications and services such as 5G, gaming and IoT.

AtlasEdge is an ideal partner for Digital Realty’s edge strategy, given the unique last-mile network reach of AtlasEdge’s assets in addition to their highly distributed reach across Europe. As interconnection and other data center solutions move towards the edge, Digital Realty’s expertise in designing and operating solutions at scale enhances the value of partnerships for both parties.

Digital Realty also announced in October 2021 that it had formed a joint venture with Pembani Remgro Infrastructure Fund (an infrastructure fund focused on Africa) that aims to acquire Medallion Data Centres. The press release billed Medallion as “Nigeria’s leading colocation and interconnection provider” and had this to say on the venture:

Medallion operates two data centers, one in Lagos, the most populous urban metropolitan area in Africa with approximately 15 million people, and one in Abuja, the capital of Nigeria. Medallion’s Lagos data center is the leading connectivity hub in Western Africa with over 70 carriers and internet service providers, over 80% of the public peering traffic on the Nigerian Internet Exchange, and a peering point for all subsea cables currently operating in Nigeria with plans to serve as a peering point for the nine new subsea cables scheduled to be in operation in Lagos by 2023.

With a population of over 200 million, Nigeria is Africa’s most populous country and the seventh most populous in the world. Its GDP is the largest in Africa and was the 26th largest globally in 2019. With a large and young population, a growing and diversifying economy as well as a maturing regulatory environment, Nigeria has experienced strong economic growth in recent years.

In conjunction with that announcement, Digital Realty also announced that Pembani Remgro Infrastructure Fund and their partner iColo, a Kenyan data center operator (the partnership has been around since 2019), were expanding into Mozambique. iColo intends to build a data center in Maputo, its first in Mozambique. Additionally, iColo recently expanded its campus in Nairobi, Kenyan, via a land acquisition that should support its growth efforts in its home country.

According to Digital Realty’s 2020 Annual Report, the REIT acquired a controlling stake in iColo last year. We are big fans of Digital Realty’s growth ambitions in Africa and India as that complements its expansion strategy in its core markets of North America and Europe.

During Digital Realty’s latest earnings call, management noted that “as of September 30, (it) had 44 projects underway around the world, totaling almost 270 megawatts of incremental capacity, with over 250 megawatts scheduled for delivery before the end of 2022.” Europe, the Middle East, and Africa (‘EMEA’) represented 27 of those projects with around 150 megawatts of incremental capacity.

Management noted in the REIT’s latest earnings call that Digital Realty was “being a bit more selective in North America” with an eye towards growth projects in Portland (Oregon), Northern Virginia, New York, and Toronto. The REIT expects to bring additional capacity online in Hong Kong this quarter and in early 2022, Digital Realty aims to bring a carrier-neutral data center facility online in Seoul.

Looking ahead, Digital Realty’s management team noted that “we’re optimistic in terms of where our same store [net operating income] growth goes for 2022” during the REIT’s third-quarter earnings call, aided by some of its recent acquisitions in attractive markets entering the same store category. On a side note, here is what management had to say regarding the recent surge in energy prices seen in Europe and elsewhere during Digital Realty’s latest earnings call (emphasis added):

“While on the topic of energy, I’m pleased to report that Digital Realty experienced only a small negative impact from the substantial rise in energy costs during the third quarter. In Europe, where concerns of an energy crisis were most acute, we typically contract for energy supplies a year or more in advance, providing price feasibility and certainty for our customers.

Elsewhere around the world, energy costs are typically passed through to customers, minimizing our direct exposure. We continue to keep a close eye on energy prices, but given the resiliency of our business model, we do not expect rising energy costs to impact our reported results by more than a few pennies.” — Bill Stein, CEO of Digital Realty

We appreciate the resiliency of Digital Realty’s business model.

ESG Considerations

A major theme we have written about in the recent past is the rise of “sustainable” and “ethical” investing practices, specifically the proliferation of environmental, social, and governance (‘ESG’) investing strategies. The proliferation of ESG investing is impacting corporate board rooms and reporting practices around the world, and this trend extends into equity, debt, and structured credit markets. Digital Realty is actively capitalizing on the proliferation of ESG investing strategies. For instance, as mentioned previously, the REIT was able to issue out Swiss green bonds with a relatively low coupon last quarter.

During Digital Realty’s latest earnings call, management noted that the REIT utilized proceeds from a Euro green bond issued out in 2020 to fund “sustainable data [center] development projects in 4 countries across 3 continents, certified in accordance with leading sustainable rating standards.” The REIT first started issuing out green bonds in 2015, according to its website. Generally speaking, green bonds often have a slightly lower cost of capital than traditional bonds, though the proceeds need to be allocated towards certain projects instead of general corporate purposes.

Looking ahead, Digital Realty has made several changes to its business to bolster its ESG reporting practices and to ensure it appeals to fund managers, individual investors, and other entities with ESG credentials in mind. In the upcoming graphic down below, Digital Realty highlights some of its recent accomplishments in the realm of ESG.

Image Shown: Digital Realty is doing what it can to appeal to investors with ESG practices in mind. Image Source: Digital Realty – Third Quarter of 2021 IR Earnings Presentation

Digital Realty is making the right call by taking the proliferation of ESG investing practices seriously. As a relevant aside, we recently launched our ESG Newsletter and related ESG Newsletter portfolio and interested members can read more about that publication by clicking this link here.

Concluding Thoughts

We liked what we saw in Digital Realty’s latest earnings report. The data center REIT is steadily expanding its global growth runway, heavily aided by its various strategic partnerships, which in turn supports its long-term cash flow growth outlook. Digital Realty is well-positioned to capitalize on numerous secular growth tailwinds going forward such as the Internet of Things (‘IoT’) trend, the proliferation of 5G technologies and e-commerce, and surging data consumption. We continue to be huge fans of Digital Realty and its impressive income generation upside.

To read more about the data center REIT industry please check out our latest article covering CyrusOne (CONE), which is included as an idea in our High Yield Dividend Newsletter portfolio. That article is titled High-Yield Idea CyrusOne Considers Selling Itself and can be viewed here.

—–

Real Estate Investment Trust Industry – CONE, DLR, FRT, O, REG, SPG, WPC, PEAK, HR, LTC, OHI, UHT, VTR, WELL, PSA, EQIX, CUBE, EXR, IRM

Technology Giants Industry – FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI

Other: BIP, VNQ, KIM, NNN, PLD, DRE, REXR, FR, EGP, CBRE, JLL, XLRE

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Apple Inc (AAPL), Cisco Systems Inc (CSCO) and Microsoft Corporation (MSFT) are all included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares, Facebook Inc (FB), Korn Ferry (KFY), PayPal Holdings Inc (PYPL) and Visa Inc (V) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. CubeSmart (CUBE), CyrusOne Inc (CONE), Digital Realty Trust Inc (DLR), Public Storage (PSA), and Vanguard Real Estate Index Fund ETF (VNQ) are all included in Valuentum’s simulated High Yield Dividend Newsletter portfolio. Digital Realty Trust Inc, Oracle Corporation (ORCL), Qualcomm Inc (QCOM), and Realty Income Corporation (O) are all included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Facebook Inc, Oracle Corporation, and Taiwan Semiconductor Manufacturing Company, Limited (TSM) are all included in Valuentum’s simulated ESG Newsletter portfolio. Long put options on the SPDR S&P 500 ETF Trust (SPY) with an expiration date of December 31, 2021, and strike price of $412 are included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.