Image Source: TradingView

By Brian Nelson, CFA

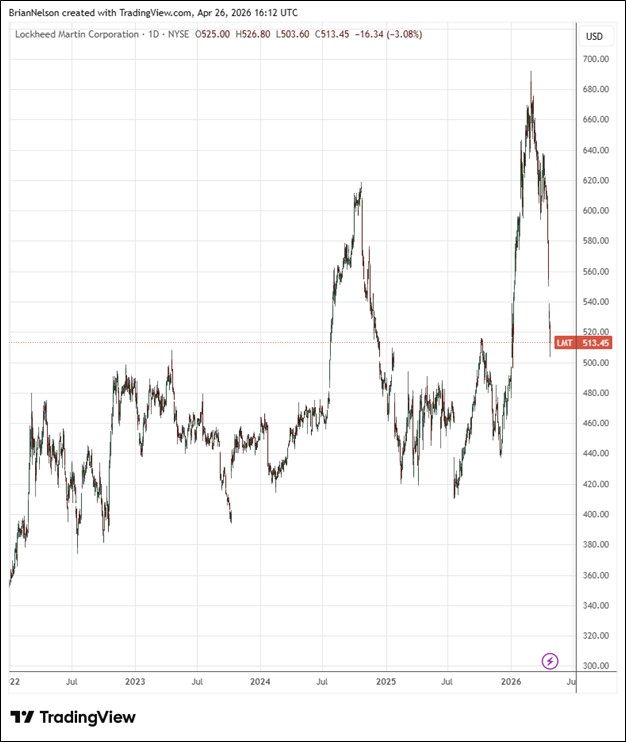

On April 23, Lockheed Martin (LMT) reported weak first quarter results that missed expectations on both the top and bottom lines. Revenue was essentially flat on a year-over-year basis, to $18.02 billion, missing estimates by $230 million, while GAAP earnings per share of $6.44 missed the consensus estimate by $0.25 and compared to $7.28 in the first quarter of 2025. Cash flow from operations was $220 million in the first quarter, while free cash flow dipped into the red at -$291 million, compared to $955 million in the first quarter of 2025.

Management had the following to say about the results:

Lockheed Martin’s superior capabilities in delivering advanced defense technology and systems and in space exploration have been proven again and again in 2026. Our Orion spacecraft safely carried the crew farther from Earth than ever before during NASA’s historic Artemis II mission, concluding with a precisely executed re-entry and splashdown. Our superior fifth generation fighter jets, the F-35 and F-22, continue to operate with great effectiveness in contested and difficult missions. Additionally, our layered missile defense architecture, including phased array radars, Aegis integrated command and control system, and the THAAD and advanced Patriot Missile interceptors, protected both military assets and civilians.

Given the high level of demand for many of these systems, we also pioneered a number of commercially inspired, long-term business arrangements with U.S. government leadership. In the first quarter, we signed several framework agreements to accelerate and scale munitions production, including advanced Patriot Missile, THAAD, and PrSM. We anticipate that these groundbreaking agreements will benefit both industry and the government and serve as the example for future contracting initiatives. The multi-year demand commitments defined in these framework agreements will in turn support strategic investments in production infrastructure, bolster our supply chain, and enhance our workforce to increase production rates of these critical systems by 3-4 times current rates.

Our first quarter revenue of more than $18 billion, segment operating profit of $1.8 billion, and substantial backlog were a result of both strong customer demand, our continued commitment to operational performance and focused risk management.

On the operating line, consolidated operating profit in the first quarter dropped to $2.06 billion from $2.37 billion in the year-ago quarter, while net earnings fell to $1.5 billion from $1.7 billion in last year’s period. Management reaffirmed its 2026 outlook. Sales are expected in the range of $77.5-$80 billion, with business segment operating profit of $8.425-$8.675 billion. Diluted earnings per share for the year is targeted in the range of $29.35-$30.25, with free cash flow expected in the range of $6.5-$6.8 billion. We like Lockheed as key defense exposure in the Dividend Growth Newsletter portfolio, and shares yield 2.7% at the time of this writing.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, QQQM, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, QQQM, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.