Image Shown: American Tower Corporation operates the tower structure and related land parcel of cell tower assets, while its tenants handle the remainder. Image Source: American Tower Corporation – Third Quarter of 2021 IR Earnings Presentation

By Callum Turcan

Rising geopolitical tensions, inflationary headwinds, supply chain hurdles, and pressures from the rising interest rate environment are all weighing negatively on equity markets. Through the end of normal trading hours on February 19, the S&P 500 (SPY) is down over 9% and the Vanguard Real Estate Index Fund ETF (VNQ) is down over 11% year-to-date on a price only basis. In our view, this selloff presents an opportunity for investors with a longer term focus to consider high-quality REITs such as American Tower Corporation (AMT), which is now trading at a significant discount to our estimate of its intrinsic value.

At the start of February 2022, we added AMT as an idea to the High Yield Dividend Newsletter portfolio. Shares of AMT yield ~2.4% as of this writing and the cell tower REIT has a nice dividend growth track record, a trajectory we expect will continue in earnest going forward given its stellar free cash flow generating abilities and bright long-term growth outlook. Our fair value estimate for American Tower sits at $281 per share, well above where AMT is trading at (~$228 per share) as of this writing.

Overview

American Tower’s portfolio consisted of ~219,000 communications-related real estate sites across the globe at the end of September 2021, including over 43,000 sites in the US and over 75,500 in India. The REIT’s asset base includes towers that American Tower owns and operates or operates under long-term lease agreements, distributed antenna system (‘DAS’) networks, land parcels that are leased out to operators of telecommunications assets, fiber networks, and telecommunications infrastructure. American Tower also manages third-party rooftop and tower sites. Virtually all the REIT’s sales are generated from its rental revenues. American Tower also offers tower-related services in the US. Its services include site application, zoning and permitting analysis, and structural analysis.

Image Shown: American Tower’s vast communications-focused real estate portfolio includes assets across the globe, providing the REIT with significant scale in numerous geographical markets. Image Source: American Tower – Third Quarter of 2021 IR Earnings Presentation

American Tower is a highly acquisitive entity. In January 2020, the REIT closed on its purchase of Eaton Towers Holdings for ~$1.85 billion in total considerations when including debt, adding roughly 5,700 communications sites to its African portfolio. American Tower also paid $0.5 billion to MTN Group Limited (MTNOY) for its non-controlling interest in two joint-ventures operated by American Tower in Ghana and Uganda through a deal that closed in 2020. The REIT’s focus on international growth opportunities and establishing sizable positions in each market in which it operates underpins why we view American Tower’s longer term growth runway so favorably.

The REIT has also been steadily bulking up its North American presence through acquisition activities in recent years. In December 2020, American Tower closed on its deal for InSite Wireless Group for ~$3.5 billion in total closing considerations, adding ~3,000 communications sites to its asset base. That included 1,400+ owned towers in the US, 200+ owned towers in Canada, ~70 DAS networks in the US, along with 600+ land parcels and ~400 rooftop sites. American Tower is also expanding organically, and we will cover those efforts later in this article.

In late December 2021, American Tower acquired data center operator CoreSite Realty through a ~$10.1 billion all-cash deal when including debt, adding data center and interconnection assets to its business. Pushing into the data center space should enable material operational synergies at American Tower, which we appreciate. These represent a few of the many deals American Tower has completed in recent years, and we expect the REIT will continue pursuing M&A opportunities going forward.

Financial Overview

We are tremendous fans of American Tower’s ability to generate sizable free cash flows in almost any operating environment. From 2018-2020, the REIT generated ~$2.8 billion in free cash flow per year on average. Its free cash flows have historically fully covered its total dividend obligations (‘distributions to noncontrolling interest holders, net’ plus ‘distributions paid on common stock’ plus ‘distributions paid on preferred stock’) and then some.

From 2018-2020, American Tower generated ~$1.2 billion in “excess” free cash flow per year on average (its free cash flow after covering total dividend obligations). The upcoming graphic down below highlights American Tower’s stellar excess free cash flow generating abilities.

Image Shown: On a historical basis, American Tower’s free cash flows have fully covered its total dividend obligations and then some. We expect this will continue being the case going forward, highlighting why we are big fans of the REIT. Image Source: Valuentum, with data from American Tower (I, II)

At the end of September 2021, American Tower had $33.5 billion in total debt (inclusive of short-term debt) along with sizable operating lease liabilities on the books. Its cash and cash equivalents position (exclusive of restricted cash) sat at $3.3 billion at the end of this period, providing the REIT with ample liquidity to meet its near term funding needs. American Tower also has revolving credit facilities it can tap to as needed, which combined had ~$5.4 billion in remaining borrowing capacity at the end of September 2021.

Looking ahead, American Tower should be able to continue tapping capital markets as needed at attractive rates to refinance maturing debt and fund its acquisition activities, in our view. The REIT has an investment grade credit rating (Baa3/BBB-/BBB+) with stable outlooks from each of the ‘Big Three’ rating agencies, ample liquidity on hand, and is a stellar generator of excess free cash flow, which should support its ability to tap debt markets. Historically, American Tower has also utilized a combination of secondary equity issuances and at-the-market (‘ATM’) equity issuance programs to raise funds to cover its growth efforts, refinance debt, and for other corporate purposes.

Cash Flow Growth Outlook

American Tower’s business model comes with tremendous operating leverage (revenue growth generally leads to meaningful margin expansion over time), particularly as it concerns its tower operations as one can see in the upcoming graphic down below. By adding additional tenants to its existing tower assets, American Tower’s revenue, gross margin, and return on investment per tower surges higher. These figures in the upcoming graphic down below are for illustrative purposes, though it’s clear American Tower benefits immensely from multi-tenant economics.

Image Shown: The REIT’s tower business comes with significant operating leverage which supports American Tower’s company-wide outlook over the long haul as it concerns margin expansion upside and ultimately cash flow growth. Image Source: American Tower – Third Quarter of 2021 IR Earnings Presentation

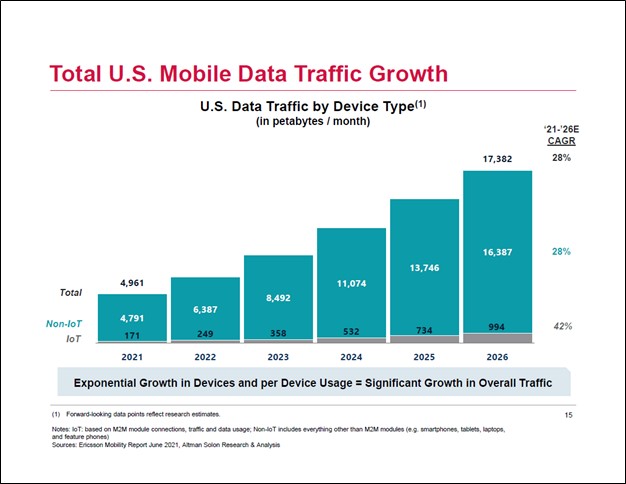

The REIT expects US mobile data consumption will surge higher in the coming years, which in turn should make it easier for American Tower to find multiple tenants for each of its domestic cell towers and other telecommunications assets. American Tower notes that a combination of expected increases in internet-connected mobile devices along with forecasted growth in data consumption per device could see US mobile data traffic more than triple by 2026 versus 2021 levels, citing third-party data to justify its reasoning.

The Internet of Things (‘IoT’) trend, such as the proliferation of smartwatches and internet-capable appliances, and increased functionality from smartphones in the 5G era (which makes it easier to stream high-quality videos and play mobile games on smartphones) will help drive data consumption up considerably. American Tower is incredibly well-positioned to capitalize on this upside.

Image Shown: The IoT trend along with growth from smartphones in the wake of the 5G era should lead to enormous growth in US mobile data traffic over the coming years, a boon for American Tower. Image Source: American Tower – Third Quarter of 2021 IR Earnings Presentation

Internationally, the outlook for mobile data traffic growth is also incredibly bright as one can see in the upcoming graphic down below. American Tower expects mobile data consumption growth to be widespread on a geographic basis, citing third-party data to back up its reasoning. Looking ahead, there is ample room for American Tower to continue scaling up its business in key markets around the globe while bulking up its domestic presence to enable the ongoing rollout of 5G wireless services.

Image Shown: The outlook for American Tower’s international operations is incredibly bright and supported by numerous secular tailwinds. Mobile data consumption is expected to surge around the world over the coming years. Image Source: American Tower – Third Quarter of 2021 IR Earnings Presentation

Organic Growth Opportunities

During American Tower’s third quarter of 2021 earnings call, management had this to say as it concerns the REIT’s organic growth efforts (emphasis added):

“…[W]e have significantly ramped up our new build program given the tremendous need for entirely new infrastructure. In fact, if you take the nearly 5,900 sites we built last year and add our expected 7,000 sites at the midpoint of our outlook to be constructed this year, it would represent almost as many sites as the previous 5-years combined. And as we laid out a few quarters ago, we are targeting the construction of up to 40,000 to 50,000 new sites over the next 5 years.” — Tom Bartlett, President and CEO of American Tower

American Tower is building new cell towers and other communications assets as demand from telecommunications services providers to lease those kinds of real estate remains robust. In 2021, American Tower intended to step up its capital expenditures to ~$1.6 billion from ~$1.0 billion in 2020 to bring additional communications-focused real estate assets online. Please note that management views the lion’s share of that budget as discretionary in nature, meaning that most of its capital expenditures are going towards growth endeavors. American Tower’s maintenance-related capital expenditure obligations are modest, and this dynamic supports its free cash flow outlook over the longer haul. Here is additional management commentary provided during American Tower’s third quarter earnings call (emphasis added):

“Consistent with our prior comments, we anticipate growing our dividend by at least 10% annually in the coming years. Moving on to CapEx, we reiterate our expectations of spending nearly $1.6 billion at the midpoint with nearly 90% being discretionary in nature. Driving a good portion of this discretionary CapEx is our continued expectation to construct 7,000 sites at the midpoint this year, with the vast majority in our international markets.” — Rod Smith, EVP, CFO, and Treasurer of American Tower

American Tower remained a free cash flow generating powerhouse last year (through the first three quarters of 2021), even as its capital expenditure expectations shifted higher, as its net operating cash flows have grown nicely of late. The REIT aims to grow its dividend by double-digits annually going forward as its cash flows swell higher, and we appreciate management’s commitment to rewarding income-seeking investors.

Concluding Thoughts

We are huge fans of American Tower. The REIT’s business model includes a significant amount of operating leverage, and secular tailwinds should enable American Tower to find multiple tenants for most of its cell towers as telecommunications services providers seek to scale their capacity to meet growing mobile data consumption. American Tower’s growth runway is immense with opportunities all over the globe and in the US.

Due to its stellar excess free cash flow generating abilities and bright outlook, we expect strong growth in American Tower’s per share payout over the long haul. Our adjusted Dividend Cushion ratio, which takes American Tower’s ability to tap capital markets into account, sits well above parity (at 1.6). We give the REIT a “GOOD” Dividend Safety rating and an “EXCELLENT” Dividend Growth rating.

American Tower is set to report its fourth quarter 2021 earnings before the market opens on February 24 and will host an earnings call shortly thereafter. The REIT should provide an overview of its 2022 guidance in conjunction with its upcoming earnings report. We are keeping a close eye on American Tower.

—–

Real Estate Investment Trusts (REITs) Industry – CONE, DLR, FRT, O, REG, SPG, WPC, PEAK, HR, LTC, OHI, UHT, VTR, WELL, PSA, EQIX, CUBE, EXR, IRM

Related: MTNOY, VNQ, UNIT, DBRG, VPN

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares in FB and XLE. American Tower Corporation (AMT), CubeSmart (CUBE), Life Storage Inc (LSI), Digital Realty Trust Inc (DLR), Public Storage (PSA), and Vanguard Real Estate Index Fund ETF (VNQ) are all included in Valuentum’s simulated High Yield Dividend Newsletter portfolio. Digital Realty Trust and Realty Income Corporation (O) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.