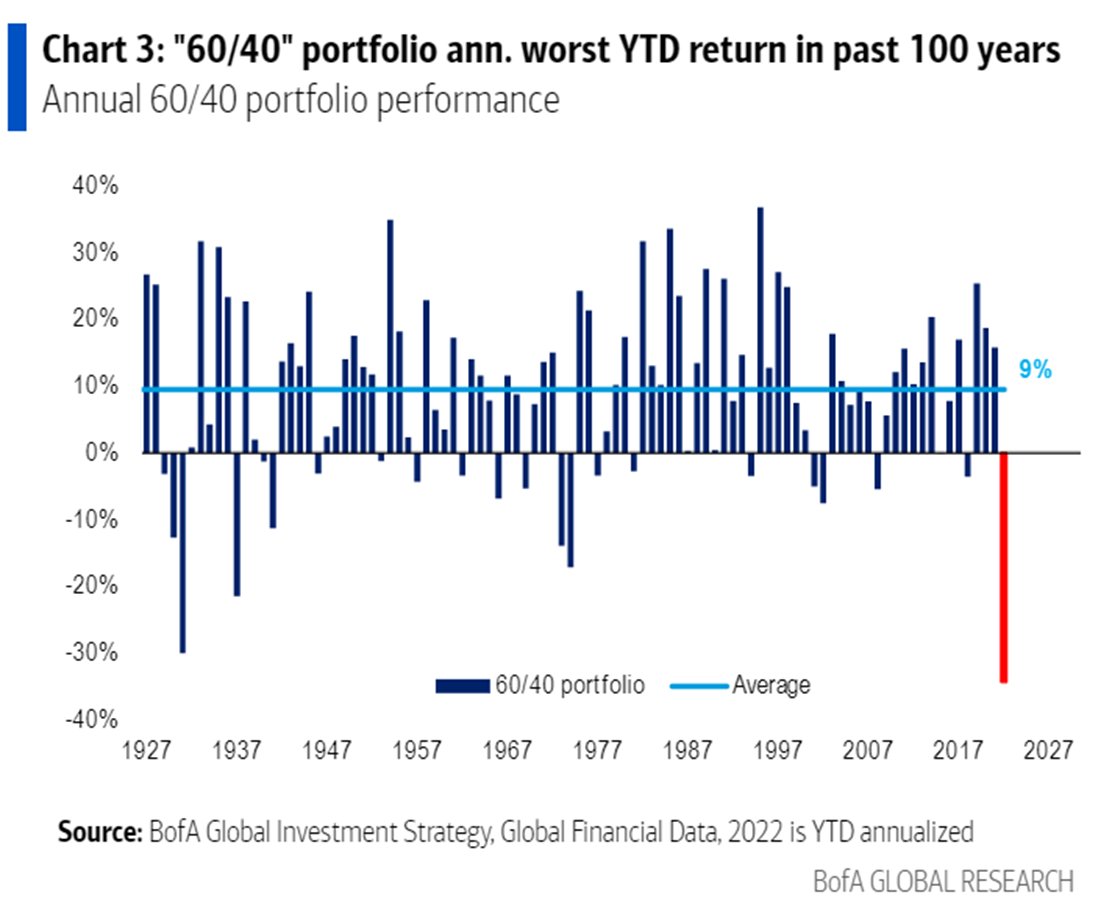

“When I highlighted my concerns about MLPs years ago, we were doubted, but we ended up being right. When we warned about the value factor, we were told the quants had solved the market, but we ended up being right, with the quant factor having its worst year in 2020 in history. We called the COVID-19 crash and highlighted opportunities for dollar cost averaging near the March 2020 bottom. We were bullish on the huge upswing in 2021, and we avoided the worst areas of 2022 to the point where our publishing suite is doing fantastic this year, if not “outperforming.” When I highlighted the second edition of the book Value Trap, our team released a press release warning about the 60/40 stock/bond portfolio in August 2020…” — Brian Nelson, CFA

Image: The year-to-date simulated estimated performance of the High Yield Dividend Newsletter portfolio, which continues to hold up well during 2022, while offering an attractive forward estimated dividend yield. Simulated estimated performance is calculated by Valuentum and has not been externally audited. Inquire about the High Yield Dividend Newsletter. The next edition will be released December 1, 2022.

Summary

—

Based on our estimates, the simulated High Yield Dividend Newsletter portfolio is down ~4.4% on a price-only basis so far in 2022 on an interim basis, using data from the trading session November 29 (retrieved from Seeking Alpha).

By comparison, according to data from Morningstar, the Vanguard 60/40 stock/bond portfolio (VBIAX) is down more than 15% so far this year (on a price-only basis), the Vanguard Real Estate ETF (VNQ) is down 26% year-to-date (on a price-only basis), while the iShares Mortgage Real Estate Capped ETF (REM) is down ~30% on a year-to-date basis.

Each simulated newsletter portfolio at Valuentum targets a different strategy, whether long-term capital appreciation, dividend growth, income/high yield, and the like. Generally, for the simulated Best Ideas Newsletter portfolio, it targets long-term capital appreciation potential (not in one year or a couple years, but in the long run).

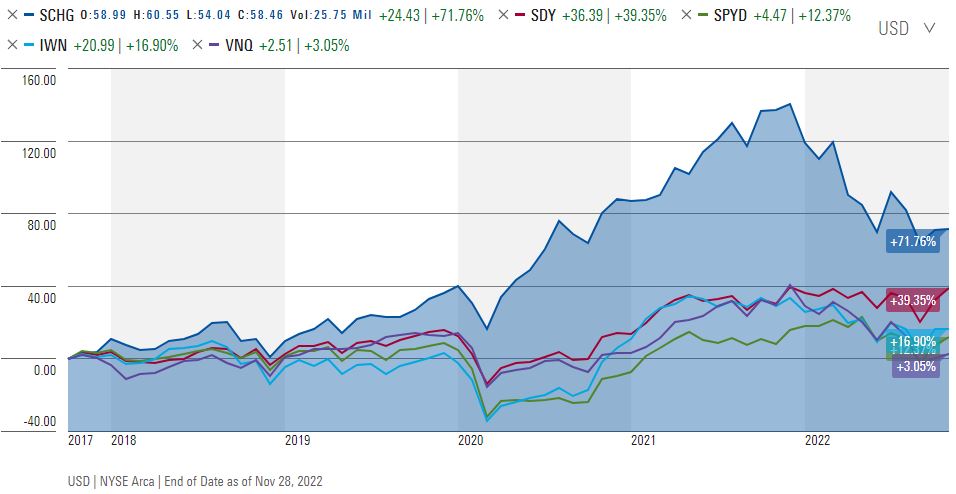

During the past five years…an ETF that tracks the area of large cap growth is up more than 70%, while an ETF that tracks the area of dividend growth has advanced ~40%, an ETF that tracks small cap value is up ~17% during the past five years, while an ETF that tracks the area of the highest-yielding S&P 500 companies is up just 12% — according to data from Morningstar. REITs, as measured by the VNQ, are up just 3% over the past five years.

We nailed the call on the drawdown in the 60/40 stock/bond portfolio this year, and readers should continue to question the merits of modern portfolio theory, not merely state that now the 60/40 stock/bond is cheap (after the huge decline)! It’s extremely important to continue to test whether something makes sense or not. If interest rates continue to rise, we think bond prices will continue to face pressure.

Sometimes, a few of our best ideas don’t work out (as in any year), but that’s why we use the simulated (and diversified) Best Ideas Newsletter portfolio to measure the success of the VBI. We’re not a quant shop. We believe in the qualitative overlay. For example, there are highly-rated ideas that don’t make the cut for the simulated Best Ideas Newsletter portfolio and there are low-rated ideas that find their way into the newsletter portfolio because they add a diversification benefit.

Given the massive up years in the broader markets in 2019, 2020 and 2021, with the simulated Best Ideas Newsletter portfolio estimated to be down in the low-double-digits so far this year (approximately ~10%-12%, by our latest tally) — and this estimate includes the missteps in Meta Platforms (META), PayPal (PYPL), and Disney (DIS) — this is actually pretty awesome, in my view —especially considering all that went wrong in other areas such as crypto, REITs, mortgage REITs, disruptive innovation stocks, Chinese equities, and the list goes on and on.

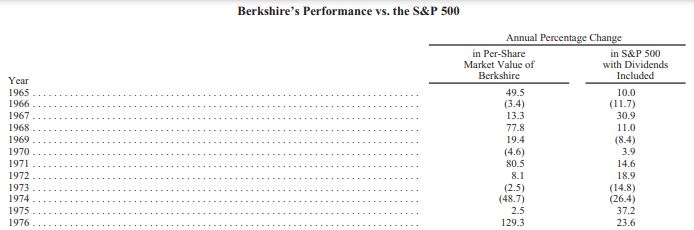

A low double-digit estimated percentage decline, as that “experienced” in the simulated Best Ideas Newsletter portfolio so far in 2022 after huge up years, can be viewed as just part of a long-term journey that targets capital appreciation. For context, Berkshire Hathaway’s stock price was nearly halved in 1974. It’s okay to time the markets a bit as we did last August, but staying engaged with investing over the long haul is a key part of the recipe for success, as it was for Berkshire investors.

For readers seeking income and high yield dividend ideas, please consider subscribing to our High Yield Dividend Newsletter. 2022 hasn’t been an up year for a lot of investors, but it shouldn’t have been a disaster either, and we’ve done a really great job avoiding the worst areas. I’m interested in hearing how you are using our service, so that we can continue to get better. All told, we’re excited about 2023, and we hope you are too!

—

By Brian Nelson, CFA

—

I hope everyone had a nice holiday weekend with family and friends!

—

Sunday, I did a short audio video here on so many things that have gone Valuentum’s way this year, from the 1) efficacy of the Dividend Cushion ratio, with Lumen Tech (LUMN) as one example, 2) the amazing success rates of ideas in the Exclusive publication, 3) year-to-date relative “outperformance” of the simulated Best Ideas Newsletter portfolio, and 4) fantastic resilience of the simulated High Yield Dividend Newsletter portfolio (the calculation shown in the image above). We’ll talk more about our dividend growth strategy soon!

—

But in this article, let’s talk more about the simulated High Yield Dividend Newsletter portfolio. This simulated portfolio is included in the High Yield Dividend Newsletter that we publish on the first of each month for members that are interested in high dividend paying stocks. Please make sure that you are getting everything you want from Valuentum! Inquire about adding this newsletter to your subscription if high dividend paying stocks are your cup of tea.

—

Based on our estimates, the simulated High Yield Dividend Newsletter portfolio is down ~4.4% on a price-only basis so far in 2022 on an interim basis, using data from the trading session November 29 (retrieved from Seeking Alpha). The biggest drivers behind the success of the simulated High Yield Dividend Newsletter portfolio this year have been the addition of Chevron (CVX) and Exxon Mobil (XOM) to the portfolio last year. With the forward estimated dividend yield of this simulated newsletter portfolio at ~5%, those that were following it closely may have had a very, very resilient year with respect to total estimated return.

—

But let me explain why I think this “performance” from the simulated High Yield Dividend Newsletter portfolio is actually fantastic. By comparison,according to data from Morningstar, the Vanguard 60/40 stock/bond portfolio (VBIAX) is down more than 15% so far this year (on a price-only basis), the Vanguard Real Estate ETF (VNQ) is down 26% year-to-date (on a price-only basis), while the iShares Mortgage Real Estate Capped ETF (REM) is down ~30% on a year-to-date basis. These areas are largely this particular portfolio’s comps — and when compared to these areas, it’s hard to say our high yield dividend ideas haven’t done great!

—

Each simulated newsletter portfolio at Valuentum targets a different strategy, whether long-term capital appreciation, dividend growth, income/high yield, and the like. Generally, for the simulated Best Ideas Newsletter portfolio, it targets long-term capital appreciation potential (not in one year or a couple years, but in the long run). Given the massive up years in the broader markets in 2019, 2020 and 2021, with the simulated Best Ideas Newsletter portfolio estimated to be down in the low-double-digits so far this year (approximately ~10%-12%, by our latest tally) — and this estimate includes the missteps in Meta Platforms (META), PayPal (PYPL), and Disney (DIS) — this is actually pretty awesome, in my view —especially considering all that went wrong in other areas such as crypto, REITs, mortgage REITs, disruptive innovation stocks, Chinese equities, and the list goes on and on.

—

Let’s talk more about why we’re okay with this. Again, adding Exxon Mobil and Chevron to the simulated Best Ideas Newsletter portfolio last year gave the newsletter portfolio tremendous resilience, while Vertex Pharma (VRTX) was a key bright spot in 2022. We think it’s informative to look at Berkshire Hathaway’s first decade or so in business to get a handle on what long-term investors seeking capital appreciation can sometimes expect. Here’s Buffett’s performance below — Berkshire Hathaway had a very rough year in 1974, a year in which the per-share market value of the company was nearly cut in half (not down a little, but down a lot). That’s right — Berkshire’s stock price was nearly halved in 1974. It’s okay to time the markets a bit as we did last August, but staying engaged with investing over the long haul is a key part of the recipe for success, as it was for Berkshire investors.

—

Image: An excerpt of Buffett’s returns at Berkshire Hathaway. Image Source: Berkshire Hathaway’s 10-K.

—

In my humble view, this type of volatility, while notable, can be (or rather should be) considered par for the course for the greatest investors seeking long-term capital appreciation. Stocks are going to go up, and stocks are going to go down. Markets are going to surge, and markets are going to fall. Where we grow concerned about market volatility, as outlined in my book Value Trap, is if equity markets, in aggregate, start exhibiting the characteristics of the likes of equities associated with the GameStop frenzy. A low double-digit estimated percentage decline, as that “experienced” in the simulated Best Ideas Newsletter portfolio so far in 2022 after huge up years, is just part of a long-term journey.

—

It’s also important to note that we have a different perspective on each newsletter portfolio. We’re okay with a low double-digit pullback in the simulated Best Ideas Newsletter portfolio this year after three absolutely fantastic years in 2019, 2020, and 2021. This volatility is “normal.” We like that the simulated Dividend Growth Newsletter portfolio is doing well, too (more on this later), and we focus on dividend growth with that particular portfolio. When it comes to high yield, we’re targeting high-yield dividend payers, but we’re not willing to lose our shirts by chasing lofty dividend yields like many that chased too many equity and mortgage REITs this year. Given the eroding nature of the dividend to capital appreciation and in the context of a rising interest rate environment, some high-yielding areas may never recover!

—

Furthermore, readers could be forgetting that many of the areas that are doing well in 2022 were actually left out of the big market upswing the past few years. During the past five years, for example, an ETF that tracks the area of large cap growth is up more than 70%, while an ETF that tracks the area of dividend growth has advanced ~40%, an ETF that tracks small cap value is up ~17% during the past five years, while an ETF that tracks the area of the highest-yielding S&P 500 companies is up just 12% — according to data from Morningstar. REITs, as measured by the VNQ, are up just 3% over the past five years (image shown below). Even with the pull back in 2022, large cap growth continues to dominate the investing landscape, and we still like this area over the long run.

—

Image: Large cap growth has dominated the past five years. Image Source: Morningstar

—

We all know that disruptive innovation stocks and cryptocurrencies have been obliterated this year, with the ARK Innovation ETF (ARKK) and Bitcoin down more than 60% and 65% year-to-date, respectively. Part of being a financial publisher is that we can never know what our members and readers are doing. It’s also a key part of our independence. We can only put out great work. We nailed the call on the drawdown in the 60/40 stock/bond portfolio this year, and readers should continue to question the merits of modern portfolio theory, not merely state that now the 60/40 stock/bond is cheap (after the huge decline)! It’s extremely important to continue to test whether something makes sense or not. If interest rates continue to rise, we think bond prices will continue to face pressure.

—

The thing perhaps I like most about Warren Buffett is that he is open and willingly talks about things that he gets wrong because he knows his readers look at things from a holistic standpoint. Buffett has talked about his unforced error on airlines in the past, and he’s had some missteps on IBM (IBM) and Kraft Heinz (