Member LoginDividend CushionValue Trap

|

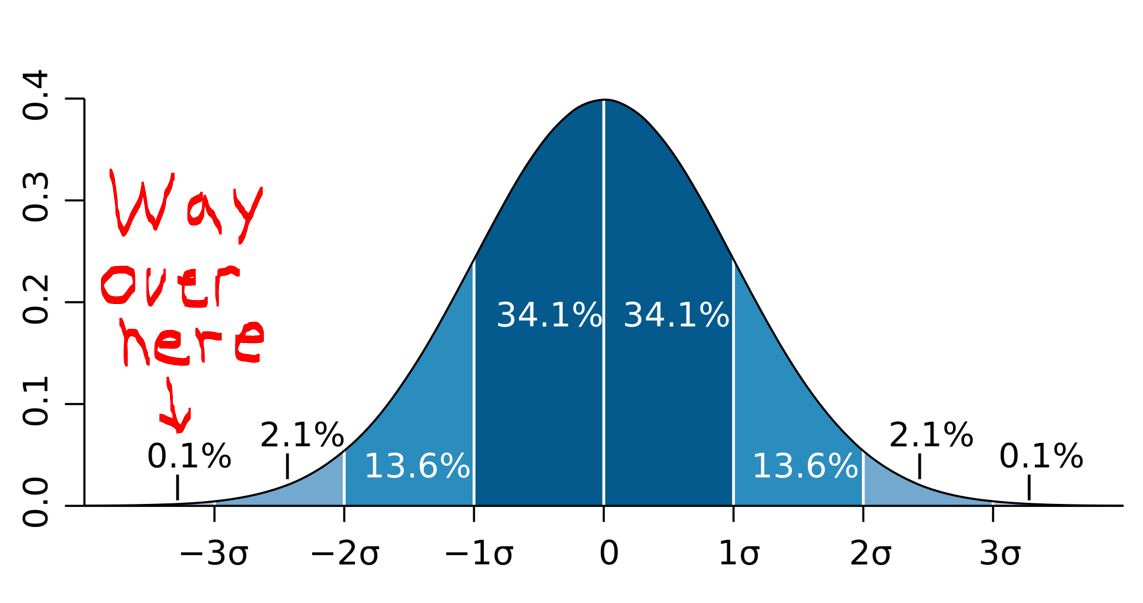

A ~0.1% Probability Since 1896

publication date: Mar 4, 2020

|

author/source: Brian Nelson, CFA

|

Next

Image Source: Wikipedia Commons

By Brian Nelson, CFA

It was mid-June 2015, and our team released our case on why the midstream MLP space would collapse. To us, it just made sense. We've been practicing enterprise valuation for a long time, and to this day, we've updated over 20,000+ discounted cash flow models. I used to head up the methodology and valuation infrastructure of a department of over 100 analysts across several continents and all sectors when I used to work at Morningstar. Baptism by fire as they say. This was about 10 years ago now.

Since our call in mid-June 2015 through March 2, 2020, on a price basis, the S&P 500 (SPY) has advanced 46%, while the Alerian MLP ETF (AMLP) declined nearly 58%. According to data from CBRE Clarion through September 2019, there have now been 111 distribution/dividend cuts. Many more have occurred since then, too. To me, this call is so remarkable because what were the odds that a small research shop from Dekalb, Illinois, would be the ones to identify such a large mispricing? One in a thousand? One in tens of thousands? How many CFA charterholders and PhD's were looking at the same thing and just missed it?

Even Former Executive Editor John Kimelman at Barron's had this to say, with a healthy dose of skepticism:

---

"I first heard of Brian Michael Nelson when he reached out to me in 2015 to pitch me on his bearish thesis on Kinder Morgan, a major energy pipeline stock with a big dividend yield that was then a darling of the income-seeking crowd. I decided to run his views on the Barron's website, along with rebuttal views from the Wall Street establishment. Bearish calls are often wrong, but when Kinder eventually cut its dividend sharply, sending the stock spiraling, I took notice. Suddenly, the bloom was off the rose of an entire sector and Brian was one of the first sounding a warning signal."

---

This note this morning isn't about how we made a call in the middle of last decade on Kinder Morgan and the MLPs, and how that has worked out fantastically for our members, to this day. In some ways, this note may be about something even bigger, even more fantastic, even more unbelievable. I picked up the following quote from Howard Marks' latest memo, and I truly want you to think about this:

The market crash in the past two weeks has been truly historic: its probability of occurrence is ~0.1% since 1896; the velocity of the plunge and of the VIX surge is the fastest on record; and the 10-year [Treasury yield] is at all-time low. (Hao Hong, BOCOM International, a subsidiary of Bank of Communications, March 1)

Now, what are the odds of us making that call on Kinder Morgan and the MLPs in mid-June 2015, and then getting our call on "crash protection" correct on an event with a probability of occurrence of ~0.1% since 1896? I could spend the afternoon calculating some probability of our research firm getting two of the biggest crashes during the past 5 years "correct" in impeccable fashion, but I can tell you, the probability is very, very small.

You might think that Valuentum is some "perma-bear," a shop that is always negative on the economy or always expecting some calamity. That's not the case either. While 85% of US quant mutual funds underperformed in 2019, Valuentum's Best Ideas Newsletter portfolio did quite well, exceeding the market return, by our estimates. The success rates in the Exclusive continue to be fantastic, too, and how about writing Value Trap just before the painful collapse of the traditional quant value factor in 2019 and into 2020? Then calling this type of level of volatility that we've been witnessing?

We get some things wrong like anyone else. I guess, in some ways, I'm writing this note to thank you for being here, for giving us the opportunity to serve you, to get you these insights, and to simply have the opportunity to work hard each and every day. I don't believe there is a research shop out there that does enterprise valuation better than us, and I know that there's not one that combines enterprise valuation, quantitative theory and behavioral finance together into an efficacious methodology as well as we do. Most of finance continues to look backwards. I hope Value Trap changes this.

Frankly, we're not really sure what others are looking at, and what they're reading, but if you're reading our stuff and seeing what we're seeing, none of what many are making out to be surprising is actually that surprising to you. I guess that's a measure of a great research firm, just how dull major events can be when you are ahead of them. After all, you weren't surprised when Kinder Morgan and the MLPs collapsed. You weren't even surprised by an event that had a 0.1% chance of happening since 1896, the crash of the past week or so. You weren't surprised by the traditional quant value factor's terrible performance in 2019, and you're not surprised by the volatility we're seeing these days.

With all that said, thank you again for your membership, and please stay safe out there!

Kind regards,

Brian Nelson, CFA

President, Investment Research

Valuentum Securities, Inc.

brian@valuentum.com

|

1 Comments Posted Leave a comment