Image Source: Adobe Inc – December 2021 Financial Analysts Meeting IR Presentation

By Callum Turcan

On December 16, Adobe Inc (ADBE) reported fourth quarter earnings for fiscal 2021 (period ended December 3, 2021) that modestly beat consensus top- and bottom-line estimates. However, shares of ADBE plummeted in the wake of its latest earnings report as management signaled that the firm’s near term growth rate would slow down in fiscal 2022 versus levels seen in fiscal 2021. Investors were apparently hoping for more, though in our view, Adobe’s longer term growth outlook is still quite bright. Our fair value estimate sits at $576 per share of Adobe.

Earnings Update

The company’s GAAP revenues were up 20% year-over-year last fiscal quarter, reaching $4.1 billion, due to strength at its subscription sales which grew by 22% year-over-year, reaching $3.8 billion. Adobe’s ‘Digital Media’ segment (includes its Adobe Creative Cloud and Document Cloud offerings) posted 21% sales growth and its ‘Digital Experience’ segment (includes its Adobe Cloud Experience offerings) posted 23% sales growth during this period. Its performance got a modest boost from the closing of its ~$1.3 billion Frame.io acquisition on October 7, which provides cloud-based video collaboration offerings. This deal should support Adobe’s growth trajectory going forward as Frame.io is highly complementary to its existing suite of products and services.

Adobe’s GAAP operating income rose by 24% year-over-year last fiscal quarter, hitting $1.5 billion, aided by economies of scale and the high margin nature of its subscription revenues. Its remaining performance obligations (‘RPO’) exited the fiscal fourth quarter at $14.0 billion, up 23% year-over-year. Adobe’s annualized recurring revenue (‘ARR’) across its core business segments continued to trend in the right direction last fiscal quarter.

In the final quarter of fiscal 2021 alone, Adobe generated $2.0 billion in free cash flow and spent $1.0 billion buying back its stock. The company does not currently pay out a common dividend and prefers to reward shareholders by investing in the business and repurchasing stock. Adobe exited fiscal 2021 with a net cash position of $1.7 billion with no short-term debt on the books, though the firm does have a moderate amount of operating lease liabilities on the books to be aware of. Its balance sheet is pristine.

Guidance and TAM Growth

Within Adobe’s latest earnings press release, management noted that the firm is targeting “an estimated $205 billion addressable market” and that the firm is “well-positioned for significant growth in the years ahead with our industry-leading products and platforms.” Please note that this $200+ billion addressable market opportunity is what Adobe expects its TAM will be by 2024. However, the company provided near term guidance that likely underwhelmed the more optimistic forecasts that Wall Street was banking on, which is why shares of ADBE plummeted in the wake of its fiscal fourth quarter earnings update.

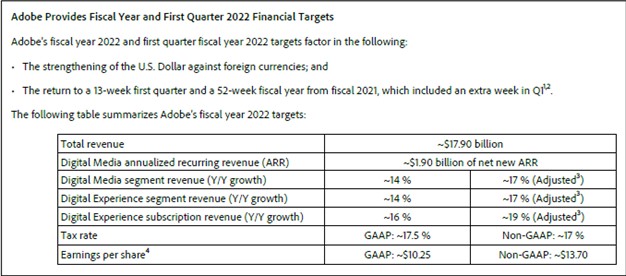

The upcoming graphic down below highlights Adobe’s guidance for fiscal 2022. For reference, the company generated $15.8 billion in GAAP revenue, $10.02 in GAAP diluted EPS, and $12.48 in non-GAAP adjusted diluted EPS in fiscal 2021. Adobe is guiding to generate ~13% annual revenue growth and ~10% annual growth in its non-GAAP adjusted EPS in fiscal 2022, which represents decent growth. Please note that during the first quarter of fiscal 2021, Adobe’s reporting period included an extra week, which makes year-over-year growth forecasts for fiscal 2022 less flattering (the firm noted that the additional reporting week added ~$0.25 billion to its total revenue in fiscal 2021).

Image Shown: An overview of Adobe’s forecasts for fiscal 2022. Image Source: Adobe – Fourth Quarter of Fiscal 2021 Earnings Press Release

Adobe’s revenue growth rate is expected to slow down in fiscal 2022 versus fiscal 2021 levels after its GAAP revenues boomed higher by 23% on an annual basis last fiscal year. However, double-digit revenue and non-GAAP adjusted diluted EPS growth on an annual basis would still represent decent performance if Adobe’s current forecasts are realized.

Expected growth at its total addressable market (‘TAM’) underpins Adobe’s more promising medium-term outlook. For instance, its Document Cloud offerings should benefit from the proliferation of e-signature activities, greater document workflow and process automation needs, and rising mobile use among other things. By 2024, Adobe views its Document Cloud TAM rising to approximately $32 billion.

Image Shown: Adobe expects that the TAM for its Document Cloud offerings should grow to ~$21 billion by 2023 and ~$32 billion by 2024. Image Source: Adobe – December 2021 Financial Analysts Meeting IR Presentation

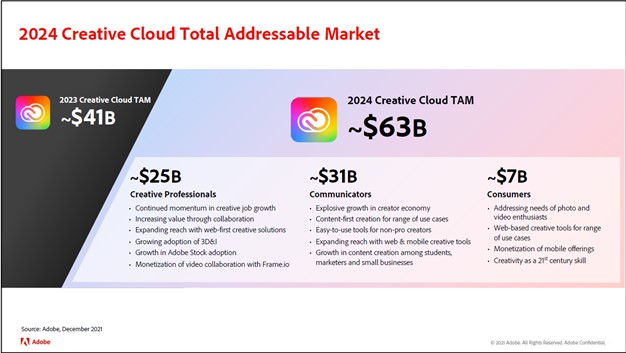

Pivoting to its ‘Creative Cloud’ offerings, Adobe expects TAM expansion to be driven by growing adoption of Adobe Stock (offers royalty-free images, photos, videos, graphics, and more), booming growth in the “creator economy” as social media enables new economic activities, adding addition capabilities to its Creative Cloud suite of products and services, and better monetizing its mobile offerings in this space. By 2024, Adobe expects its Creative Cloud TAM to grow to approximately $63 billion.

Image Shown: Adobe expects that the TAM for its Creative Cloud offerings should grow to ~$41 billion by 2023 and ~$63 billion by 2024. Image Source: Adobe – December 2021 Financial Analysts Meeting IR Presentation

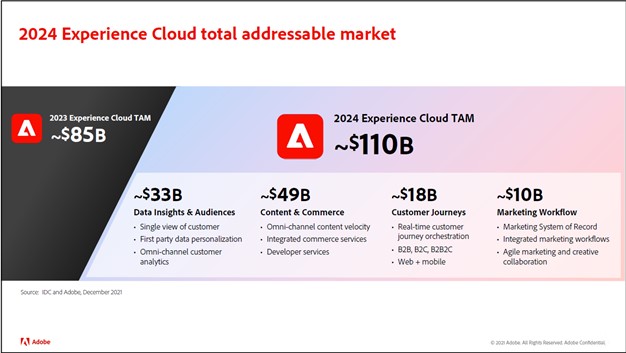

Finally, Adobe expects the TAM of its Experience Cloud offerings should hit ~$110 billion by 2024. The proliferation of e-commerce, the need to maintain well-run omni-channel selling capabilities (physical and digital), and the desire of its customers to have integrated solutions when it comes to selling, marketing, and customer data retention purposes underpins Adobe’s growth outlook on this front.

Image Shown: Adobe expects that the TAM for its Experience Cloud offerings should grow to ~$85 billion by 2023 and ~$110 billion by 2024. Image Source: Adobe – December 2021 Financial Analysts Meeting IR Presentation

Management Commentary

During Adobe’s latest earnings call management commented on the firm’s latest financial results and its longer term strategic goals. Management had a lot to say during the conference call, so we highlighted some noteworthy commentary worth keeping in mind (emphasis added, moderately edited):

“According to Adobe Analytics, online spending during the 2021 holiday season is projected to be $200 billion, and total e-commerce spending is projected to reach $1 trillion in 2022. It’s clear that digital is a requirement to conducting business today…

Companies [are] automating mission-critical document processes like HR and legal to drive increased efficiency and agility.At the same time, customers now expect rich personalized digital experiences that are relevant, engaging and consistent across any device. It’s well documented that digital first businesses drive greater long-term growth and customer loyalty…

With Document Cloud, we’re accelerating document productivity, modernizing how people view, share, and engage with documents and with Experience Cloud we’re powering digital businesses of all sizes, giving them everything they need to design and deliver great customer experiences. Underpinning our three clouds is the power of Adobe Sensei, our advanced AI/ML framework that enables us to deliver a steady stream of unparalleled innovation. Over the last year, we’ve seen the critical role that creativity has played in the world.

Creative Cloud is empowering everyone from the high school student to the social media influencer to the most demanding creative professional to tell their story. The Creative Cloud TAM is projected to be approximately $63 billion in 2024, $25 billion of that TAM comes from our core base of creative professionals who purchase Creative Cloud applications and services like Adobe Stock. New growth drivers in this segment include 3D and other immersive experiences, as well as web-first collaboration tools like Frame.io, $13 billion of the TAM is coming from communicators, non-professional creators, including small businesses, students and marketers…

We’re excited about the Document Cloud strategy and the large addressable market, which is projected to grow to $32 billion by 2024, $10 billion of that TAM is coming from knowledge workers, business professionals who typically use our core Acrobat desktop subscription offerings. Growth is expected to come from the expansion of digital document use cases, e-signatures and increase collaboration capabilities…

Our total addressable market for Adobe Experience Cloud is estimated to be $110 billion in 2024, $33 billion of the TAM is coming from the data insights and audiences category, which includes Adobe Experience platform, real time CDP, and Adobe Analytics, including our new customer journey analytics offering.” — Ann Lewnes, EVP of Corporate Strategy and Development, and CMO of Adobe

Powerful secular growth tailwinds support expected growth in the market opportunities Adobe is targeting. While Adobe has a lot on its plate, in our view, the firm is up to the task.

Concluding Thoughts

While Adobe’s near term growth trajectory is slowing down versus levels seen in the recent past, its longer term outlook remains quite bright as the TAM of its key business segments continues to grow. Recurring revenues provide for stronger cash flow profiles given the highly visible nature of those future sales, and Adobe’s capital-light business model (relatively modest capital expenditures are required to maintain a given level of revenues) better allows for the firm to generate sizable free cash flows. We are impressed with Adobe’s free cash flow generating abilities, and additionally, we are huge fans of its pristine balance sheet.

As of this writing, shares of ADBE are trading near our fair value estimate of $576 per share, keeping in mind the top end of our fair value estimate range sits at $691 per share. We do not include Adobe as an idea in any of our newsletter portfolios as we are already overweight large cap tech in our newsletter portfolios. To read more about our thoughts on big tech, check out our recent article covering Oracle Corporation’s (ORCL) latest earnings report which can be viewed here.

Adobe’s 16-page Stock Report (pdf) >>

—–

Technology Giants Industry – FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI, SIMO

Tickerized for ADBE, MSFT, CSCO, ORCL, MU, INTU, CRM, PANW, DDOG, MDB, CFLT, SNOW, WDAY, NOW, SPLK, VMW, ZS, ADSK, PATH, CHKP, ZEN, PLTR, ZETA, TDC

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Apple Inc (AAPL), Cisco Systems Inc (CSCO) and Microsoft Corporation (MSFT) are all included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares, Meta Platforms Inc (FB), Korn Ferry (KFY), PayPal Holdings Inc (PYPL) and Visa Inc (V) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Oracle Corporation (ORCL) and Qualcomm Inc (QCOM) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Meta Platforms, Oracle Corporation, and Taiwan Semiconductor Manufacturing Company Limited (TSM) are all included in Valuentum’s simulated ESG Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.