February 23 was met with intense selling as investors digested news that the crude oil (USO) markets won’t become rational anytime soon. As we had outlined in our opening piece to the Best Ideas Newsletter a few days ago, “,” Saudi Arabia is not going to back down, and the Oil Minister of the member nation of OPEC even went so far as to say he “welcomes new additional supplies,” suggesting that the global glut of crude oil will continue for the foreseeable future. Commodity-oriented equities led the selling pressure.

For those that have been reading our work for the past several months, none of this is new “news.” We’ve been warning about the risk for some time, and we believe “the lower for longer” scenario is the most probable one, with any sort of snapback to $100 per barrel crude oil a pipe dream. Of more important news, however, we did get note of the increasingly ominous environment midstream pipeline companies are facing as upstream independents look to cut costs. Regardless of what management has told you or what you’ve read from others, the midstream space is levered to commodity prices, if not directly in a 5%-10% manner but indirectly through their customer base, and we’ve been witnessing the fallout for some time.

Quite critically, Reuters reported that “within weeks, two low-profile legal disputes may determine whether an unprecedented wave of bankruptcies expected to hit US oil and gas producers this year will imperil the $500 billion pipeline sector as well (source: Reuters).” Sabine Oil & Gas and Quicksilver Resources are looking to leverage the court system via Chapter 11 bankruptcy protection to break the long-term contracts of its pipeline partners. Sabine is looking to drop its contract with Cheniere (LNG), while Quicksilver is looking to break terms with Crestwood Energy. Again, this is not new “news” for anyone reading Valuentum’s research, and we believe that in the event of a rising wave of defaults, truly no midstream player is immune. No contract is completely safe due to counterparty credit risk.

Pipelines – Oil & Gas: BPL, BWP, DPM, ENB, EPD, ETP, EVEP, HEP, KMI, MMP, NS, PAA, SE, SEP, WES

As we stated in our intro piece to the Best Ideas Newsletter, the rising risk of bad loans in the energy space is growing more and more severe. February 23, CEO of JP Morgan (JPM) Jamie Dimon noted that it would add another half billion to energy-related loan-loss reserves, perhaps a drop in the bucket compared to what may be ahead of the SIFI. We believe things will get worse before they get better, and bank executives tend to have a difficult time gauging the severity of events, underestimating them by leaps and bounds. We saw this during the Financial Crisis, and we saw it again post Dodd-Frank with the London Whale incident. Seeking Alpha reported that JP Morgan’s CFO Marianne Lake suggested that “in a stress scenario where oil stays at $25 for 18 months – will need to take another $1.5 billion in reserves.”

All of the big banks traded off on the session, including Bank of America (BAC) and Wells Fargo (WFC), which together with JP Morgan have more than $324 billion in assets tied to Texas alone. We think the smaller regional banks may be most at risk in coming years, particularly those levered to shale-rich energy resource production. Shares of Texas Capital BancShares (TCBI) and Prosperity Bancshares (PB) have been under tremendous stress the past few months, and they register as two of the biggest lenders in the state of Texas, after Comerica (CMA) and USAA Federal. The top 100 banks in Texas by asset size can be downloaded here (pdf). Though the list doesn’t have the traditional national heavyweights, we’re also watching banking activity in the Dakotas, with the largest banks in North Dakota here. We can’t easily forget that the Savings & Loan crisis of years gone by was stimulated in part by failed energy loans, and a wave of defaults and upstream bankruptcies could hurt local economies and generate material regional economic weakness.

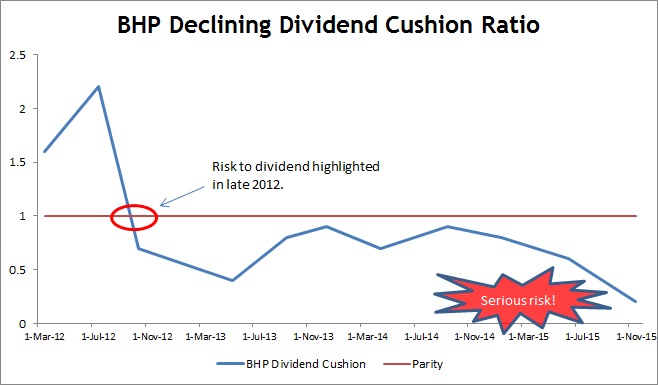

The Dividend Cushion ratio did it again. Global miner BHP (BHP) slashed its payout by 74% to $0.16 per share. We’ve been concerned about the health of the payout for some time, and the company’s Dividend Cushion ratio of 0.2 outlined the risks in full sight, well in advance of the cut. The header of the company’s dividend report, dated November 18: “We’ve grown very concerned about the health of BHP’s dividend. A dividend cut has become likely, unfortunately.” The news followed a cut by Rio Tinto (RIO), both disappointments supporting our thesis that commodity-linked equities are very difficult to hold for income purposes. Even the best of management teams have difficulty handling their boom and bust cycles. We’ll have updated reports available shortly.

Quite the opposite of Fitbit’s (FIT) quarterly report, which sent shares tumbling more than 20% February 23, recent addition to the Dividend Growth Newsletter portfolio Cracker Barrel (CBRL) was a source of “green” in an otherwise across-the-board “red” day. The “Old Country Store” grew total revenue just over 1% in its fiscal second quarter from the year-ago period. The slight revenue growth was driven by strong comparable retail sales growth of 2.6% and boosted by the firm’s pricing initiatives in its restaurants as its average menu price grew nearly 3% from the comparable period. Comparable restaurant sales crept up 0.6% from the second quarter of fiscal 2015, as average check growth of 3.4% was able to more than offset a 2.8% decline in traffic.

Though traffic trends weren’t great in the second quarter of fiscal 2016, lower gasoline prices may ultimately offer a nice tailwind for casual diners in this area, especially Cracker Barrel when considering such a high amount of its restaurants are conveniently located near interstate off-ramps (should lower prices at the pump stimulate “road trips”). The restaurant’s operating margin fell to 9.2% in the quarter from 9.4% in the comparable quarter of fiscal 2015 as increases in other store operating expenses were only partially offset by a reduction in labor and related expenses. Cracker Barrel delivered earnings at the high end of its guidance range with $1.91 in adjusted earnings per diluted share for the period, though this was slightly down from $1.93 on a comparable basis in the year-ago quarter.

Cracker Barrel expects comparable store restaurant and comparable store retail sales growth of 1.5%-2.5% and total revenue between $2.9-$2.95 billion for the full fiscal year, representing top-line growth of ~2%-4% from fiscal 2015. The firm will also try its hand in the fast-casual market before the end of fiscal 2016, though the results from the new concept–to be named Holler & Dash–are not likely to impact results for the year.

However, the real star of the show for the run in Cracker Barrel’s shares may be the nation’s chicken flocks. As the avian flu outbreak concerns of 2015 have waned, expectations for egg prices–a major input cost for Cracker Barrel–have fallen. The company has reduced its expectation for food commodity inflation to 1% for fiscal 2016 from previous guidance of 2.5%-3%.

The expectation for lower input costs coupled with Cracker Barrel’s geographic pricing initiative has led it to expect a full-year operating margin of 9.5%, an improvement from previous guidance of 9%-9.5%, and the company has also raised its annual earnings expectations to a range of $7.40-$7.50 in adjusted earnings per diluted share from original guidance of $7.15-$7.30. We think this guidance increase is nothing to balk at, and Mr. Market agrees. Cracker Barrel yields ~3% after finishing up more nearly 5% February 23. We continue to like shares.

Please be sure to visit the website at valuentum.com/. We cannot possibly deliver all of our research and analysis via email. We’re available for any questions.

Image Source: Mike Mozart