Image Source: Valuentum

By Brian Nelson, CFA

Readers should expect a substantial reduction in our fair value estimate of Meta Platforms (META). The company’s spending is out of control, and the impact on our expectations of free cash flow will be materially punitive.

As we have reiterated time and time again in our work, stock prices and returns are based in part on future expectations of free cash flow, and our expectations for Meta’s have changed. A look at how fast things fell apart at Meta is informative.

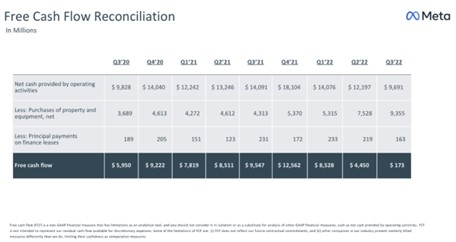

The company reported Q4’21 results in February 2022, and it’s only been a few months for the company to experience the considerable deterioration — for free cash flow to fall from $12.6 billion in the fourth quarter of 2021 to just $173 million in the third quarter of 2022.

Image: Meta Platforms’ free cash flow has fallen significantly in recent quarters. Image Source: Meta Platforms

A complete disaster, and one that very few could have anticipated, given the rapidity of the decline. Meta continues to be squeezed by the likes of TikTok with respect to short-form video, and from Apple (AAPL) in light of recent software privacy changes. We’re not looking back.

Apple’s fourth-quarter fiscal 2022 results (ends September 24, 2022), released October 27, weren’t bad, especially considering prior rumors that iPhone 14 demand may be hurting. The company noted that its “active installed base of devices (reached) all-time high(s) for all major categories,” and having such a valuable installed base is music to our ears, given the high-margin and recurring Services revenue associated with it.

Apple’s revenue advanced 8% on a year-over-year basis during the period, while quarterly earnings per diluted share edged up 4%. Clearly, management is showing that it can execute well in light of a challenging economic environment, and that consumers will continue to buy Apple products almost irrespective of budgetary pressures. The handheld phone has become so integral to our lives that perhaps some consumers may even miss a car payment before having their phones shut off. We liked Apple’s quarterly results, but we still remain cautious on consumer spending.

We don’t have to look any further than Amazon’s (AMZN) third-quarter performance to find reason to remain on high alert with respect to the economic environment. We have yet to see a negative wealth effect from declining stock and bond prices impact the broader economy, in our view, and Amazon is only targeting 2%-8% sales growth in the fourth quarter of 2022, with expectations for only marginal operating income generation. Amazon remains well-positioned to capitalize on enterprise/cloud spending and e-commerce proliferation, but as Amazon founder Jeff Bezos recently tweeted, “the probabilities in this economy tell you to batten down the hatches.”

Garbage hauler Republic Services (RSG) and data center REIT Digital Realty Trust (DLR)—two ideas in the simulated Dividend Growth Newsletter portfolio—reported their respective third-quarter results recently, and while Digital Realty continues to face pressure due to rising interest rates and declining REIT economics, we’re not overreacting to changing market conditions. REITs remain but a very small “weighting” in the simulated Dividend Growth Newsletter portfolio and High Yield Dividend Newsletter portfolio, with the group as measured by the Vanguard Real Estate ETF (VNQ) falling more than 28% year-to-date on a price-only basis. Shares of DLR yield ~4.9% at the time of this writing.

We like Republic Services a lot as it operates as an oligopoly in municipal solid waste disposal in the U.S., a position that gives it pricing power during this inflationary economic environment. During the third quarter of 2022, Republic posted 10.2% organic growth, with core price increases of 6.9%. Garbage haulers are notorious for raking in considerable free cash flow, with Republic pulling in $1.665 billion in the quarter, on an adjusted basis, a measure that advanced 22.8% versus the last year. Shares of RSG yield ~1.5% at the time of this writing.

Three of the best-performing equities in the simulated newsletter portfolios year-to-date in 2022 also reported third-quarter results recently. Shares of Vertex Pharma (VRTX) have advanced 35% so far this year, while Exxon Mobil (XOM) and Chevron (CVX) have done fantastic, too. We recently wrote up Vertex in the following note, “Best Idea Vertex Pharma Outperforming in 2022,” and we remain bullish on the outlook for crude oil, “2022 Oil & Gas Market Update: “The Outlook for Crude Oil Prices Remains Quite Bullish.”

Concluding Thoughts

Readers should expect a substantial reduction in our fair value estimate of Meta Platforms on the basis of materially reduced forecasts of free cash flow. Apple’s calendar third-quarter results were good, considering that many were worried about iPhone 14 demand heading into the report. Amazon’s results support a cautious tone with respect to consumer spending, while we remain bullish on three of our best-performing ideas so far in 2022 – Vertex Pharma, Exxon Mobil, and Chevron. We didn’t see anything in the Republic Services and Digital Realty reports that would warrant any material changes to our theses at this time.

———————————————

About Our Name

But how, you will ask, does one decide what [stocks are] “attractive”? Most analysts feel they must choose between two approaches customarily thought to be in opposition: “value” and “growth,”…We view that as fuzzy thinking…Growth is always a component of value [and] the very term “value investing” is redundant.

— Warren Buffett, Berkshire Hathaway annual report, 1992

At Valuentum, we take Buffett’s thoughts one step further. We think the best opportunities arise from an understanding of a variety of investing disciplines in order to identify the most attractive stocks at any given time. Valuentum therefore analyzes each stock across a wide spectrum of philosophies, from deep value through momentum investing. And a combination of the two approaches found on each side of the spectrum (value/momentum) in a name couldn’t be more representative of what our analysts do here; hence, we’re called Valuentum.

———————————————

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.