|

|

Recent Articles

-

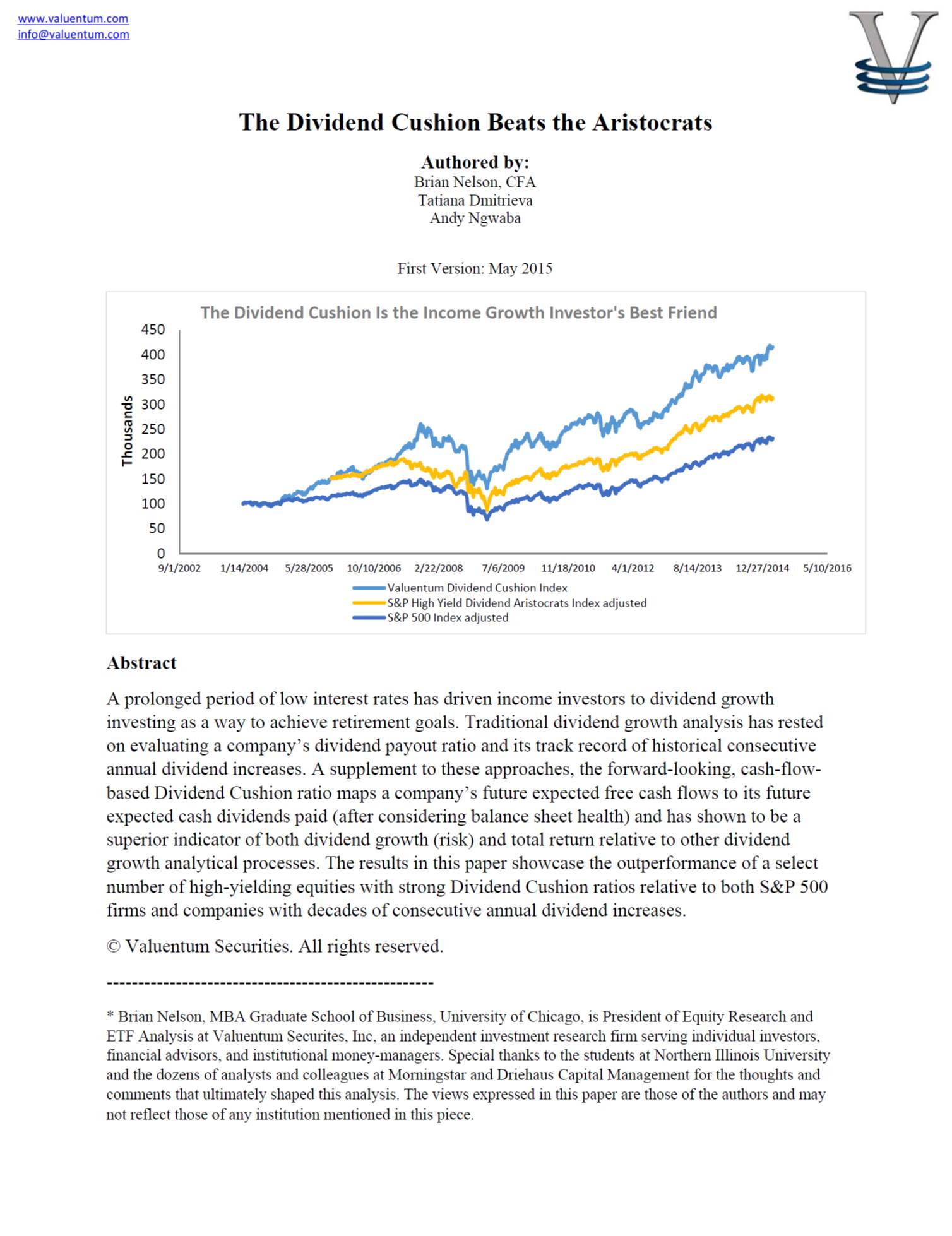

The Dividend Cushion Beats the Aristocrats

The Dividend Cushion Beats the Aristocrats

Apr 5, 2024

-

A prolonged period of low interest rates has driven income investors to dividend growth investing as a way to achieve retirement goals. Traditional dividend growth analysis has rested on evaluating a company’s dividend payout ratio and its track record of historical consecutive annual dividend increases. A supplement to these approaches, the forward-looking, cash-flow-based Dividend Cushion ratio maps a company’s future expected free cash flows to its future expected cash dividends paid (after considering balance sheet health) and has shown to be a superior indicator of both dividend growth (risk) and total return relative to other dividend growth analytical processes. The results in this paper showcase the outperformance of a select number of high-yielding equities with strong Dividend Cushion ratios relative to both S&P 500 firms and companies with decades of consecutive annual dividend increases.

-

Dividend Increases/Decreases for the Week of April 5

Apr 5, 2024

-

Let's take a look at firms raising/lowering their dividends this week.

-

ConAgra’s ESG Initiatives Noble; Near-5% Dividend Yield Supported By Free Cash Flow

ConAgra’s ESG Initiatives Noble; Near-5% Dividend Yield Supported By Free Cash Flow

Apr 4, 2024

-

Image Source: ConAgra.

ConAgra’s third-quarter fiscal 2024 results were decent, with the company showcasing strong free cash flow generation and further debt reduction. Year-to-date free cash flow at ConAgra totaled ~$1.2 billion versus $436 million during the same period a year ago. Cash dividends paid were $492 million over the same time, so ConAgra is doing a good job covering its dividend obligations with traditional free cash flow. We view this as a distinct positive for a company yielding ~4.8% at the time of this writing and think ConAgra is a consideration for investors seeking free-cash-flow covered yields and strong ESG initiatives.

-

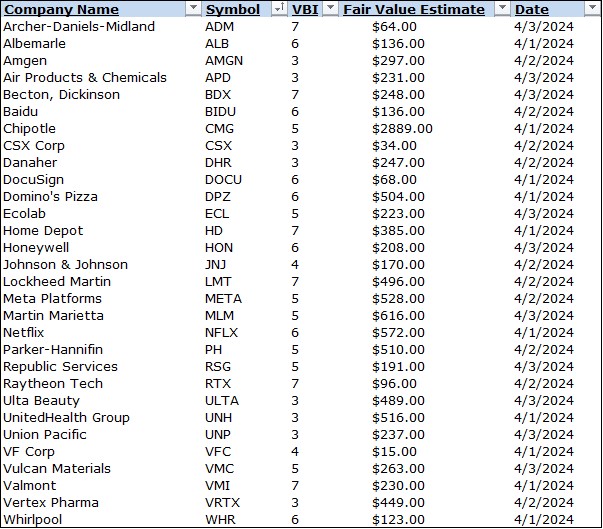

Latest Report Updates

Apr 4, 2024

-

Check out the latest report updates on the website.

|