|

|

Recent Articles

-

Gilead’s 4%+ Dividend Yield Covered Nicely with Free Cash Flow

Gilead’s 4%+ Dividend Yield Covered Nicely with Free Cash Flow

Apr 3, 2024

-

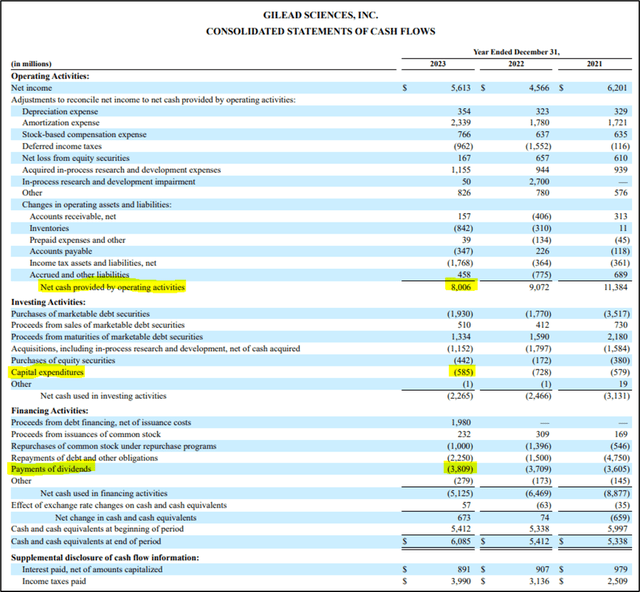

Image: Gilead’s coverage of its dividend with free cash flow remains rock-solid.

What we like about Gilead is that the company remains a very strong free cash flow generator, with the measure coming in at $7.4 billion during 2023 versus dividend payments of $3.8 billion. On a free cash flow coverage basis, Gilead 4%+ dividend yield looks rock-solid, and for this, we think investors may be wise to get paid to wait for upcoming catalysts within Gilead’s HIV and oncology pipeline.

-

Phillips 66 Raises Dividend 10%!

Apr 3, 2024

-

Refiner and High Yield Dividend Newsletter portfolio idea Phillips 66 declared on April 3 a quarterly dividend of $1.15 per share on its common stock, reflecting a 10% payout increase. We continue to like shares and will update our dividend report on the company soon.

-

PVH’s Weak Guidance Sends Shares Tumbling

Apr 3, 2024

-

On April 1, PVH Corp. reported better than expected fourth quarter results, but the company’s cautious outlook sent the stock tumbling. The Street didn’t like its first quarter guidance that calls for revenue to decline 11% (10% on a constant currency basis) compared to the first quarter of last year, inclusive of the reduction from the sale of its Heritage Brands women’s intimates business. Earnings per share for the first quarter is targeted to only be marginally higher and come in at $2.15 versus $2.14 in the same period of 2023, well below what the Street was looking for.

-

Best Buy’s Free Cash Flow Comes Up Short in Covering Dividend

Apr 2, 2024

-

Image Source: Mike Mozart.

For fiscal 2024, Best Buy generated ~$1.47 billion in operating cash flow and spent $795 million in capital spending, resulting in free cash flow of $675 million, below what it paid in dividends on the year ($801 million). That didn’t stop Best Buy from upping its dividend 2%, however, and the company continues to buy back stock. Best Buy yields ~4.6% at the time of this writing, but capital spending and volatile operating cash flow are two considerations top of mind for income-oriented investors.

|