|

|

Recent Articles

-

Our Favorite Biotech Vertex Pharma Powers Ahead, Leaps 6%+

Our Favorite Biotech Vertex Pharma Powers Ahead, Leaps 6%+

Jan 30, 2022

-

Image: Vertex Pharma continues to soar toward our fair value estimate.

The biotech arena is difficult to navigate, which is why we tend to play it a bit more conservative than most. Vertex Pharma has an established, cash-flow generating portfolio of cystic fibrosis therapies, which has helped to establish a net cash rich balance sheet and a steady stream of robust free cash flow, unlike many biotechs that need external capital and are at risk of never reaching commercialization. We’re excited about Vertex’s clinical pipeline of potentially transformative genetic therapies, and we like its exposure to CRISPR gene-editing technology, which could be a huge business in the years ahead. Vertex Pharma remains our favorite biotech play and an idea in the simulated Best Ideas Newsletter portfolio.

-

Visa Remains One of Our Favorite Ideas

Jan 28, 2022

-

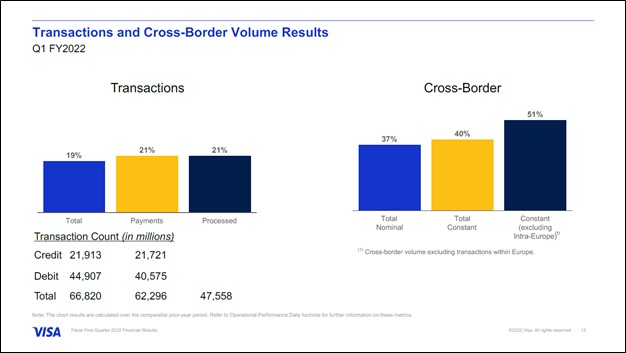

Image Shown: Visa Inc, one of our favorite companies, has been growing robustly of late. Image Source: Visa Inc – First Quarter of Fiscal 2022 IR Earnings Presentation.

On January 27, Visa reported first quarter earnings for fiscal 2022 (period ended December 31, 2021) that beat both consensus top- and bottom-line estimates. Shares of V shot higher after its results were made public. We include Visa as a “top-weighted” idea in the Best Ideas Newsletter portfolio and remain huge fans of the company. Our fair value estimate sits at $255 per share of V, well above where Visa is trading at as of this writing, indicating the payment processing giant has ample room to run higher from current levels. Shares of V yield a modest ~0.7% as of this writing.

-

Dividend Increases/Decreases for the Week January 28

Dividend Increases/Decreases for the Week January 28

Jan 28, 2022

-

Let's take a look at companies that raised/lowered their dividend this week.

-

Apple Blows Past Expectations in Fiscal First Quarter!

Jan 27, 2022

-

Image Source: Valuentum.

On January 27, 2022, Apple put up one of the best quarters by any company in history and a record for the Cupertino-based iPhone-making giant. Revenue for the quarter ending December 25, 2021, of $123.9 billion advanced 11% on a year-over-year basis, while quarterly earnings per share came in at $2.10. The top line beat expectations by more than $5 billion, even with supply chain hurdles, and the bottom-line beat of $0.20 per share was more than 10%, a huge delta considering the size of the company. We’re viewing the report very positively, and we think the strong performance may ease some broader market concerns. Apple’s gross and operating margins looked healthy, and only performance in its iPad division came in a bit light, but this was almost entirely driven by supply chain issues. Apple generated a solid $19.5 billion in revenue from its ‘Services’ division during the period, up from $15.8 billion in the year-ago quarter, showcasing its ever-growing and “sticky” installed base. Warren Buffett is a big owner of Apple’s stock, and we continue to be in favor of buybacks at Apple, too, even at these price levels. Though Apple’s market capitalization is sizable, we value shares close to $190 each at the high end of our fair value estimate range. Apple remains one of our favorite ideas in the Best Ideas Newsletter portfolio and Dividend Growth Newsletter portfolio.

|