|

|

Recent Articles

-

Meta Platforms’ Shares Remain Cheap; Long Term Focus Required

Meta Platforms’ Shares Remain Cheap; Long Term Focus Required

Jul 29, 2022

-

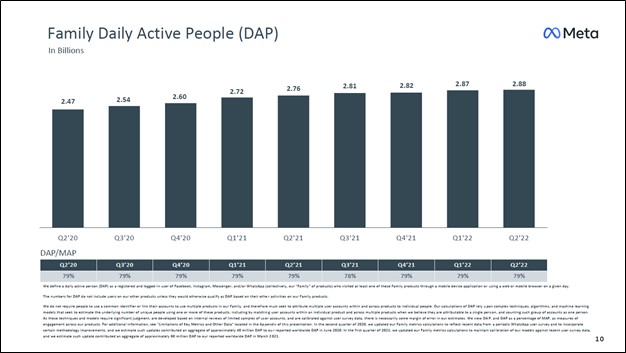

Image Shown: Meta Platforms Inc’s family of apps continued to grow its active user base last quarter. Its social media networks are used by billions of users every single day. Image Source: Meta Platforms Inc – Second Quarter of 2022 IR Earnings Presentation.

On July 27, Meta Platforms reported second quarter 2022 earnings that missed consensus top- and bottom-line estimates. We appreciate that its active user base across its family of apps (Facebook, Instagram, WhatsApp, and Messenger) and its ad impressions continued to trend in the right direction last quarter, though recent softness in its pricing power is concerning. Meta Platforms is responding by scaling back its targeted operating expense growth, which we appreciate. We continue to like Meta Platforms as an idea in the Best Ideas Newsletter portfolio, though we recognize that near term headwinds are weighing quite negatively on investor sentiment towards the name.

-

Dividend Increases/Decreases for the Week of July 29

Dividend Increases/Decreases for the Week of July 29

Jul 29, 2022

-

Let's take a look at firms raising/lowering their dividends this week.

-

High Yielding Philip Morris International’s Growth Runway Remains Intact

Jul 27, 2022

-

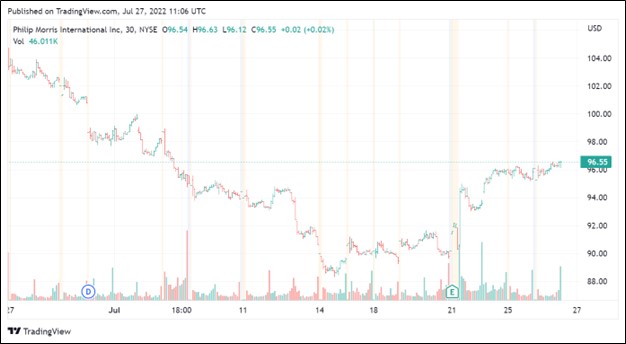

Image Shown: Shares of Philip Morris International moved higher in the wake of its second quarter earnings report.

Philip Morris International reported second quarter 2022 earnings that beat both consensus top- and bottom-line estimates. The company raised its full-year revenue and adjusted EPS guidance for 2022 on a pro forma basis (excluding its operations in Russia and Ukraine) versus previous estimates in conjunction with its latest earnings update. Now Philip Morris International expects to generate 6%-8% net revenue growth on an organic basis and 10%-12% diluted EPS growth in 2022 versus 2021 levels (these are non-GAAP metrics). We include Philip Morris International in the High Yield Dividend Newsletter portfolio as we are big fans of its resilient business model and ample pricing power.

-

Lockheed Martin Facing Near Term Headwinds; Longer Term Outlook Remains Bright

Jul 27, 2022

-

Image Source: Lockheed Martin Corporation – Second Quarter of Fiscal 2022 IR Earnings Presentation.

Lockheed Martin Corp reported earnings for the second quarter of fiscal 2022 (period ended June 26, 2022) that missed consensus top- and bottom-line estimates, largely due to delays in securing another domestic F-35 contract and supply chain hurdles. In our view, these are near term headwinds that are resolvable. Reportedly, Lockheed Martin is nearing a deal worth ~$30 billion with the US Department of Defense (‘DoD’) covering orders for around 375 F-35 aircraft. As it concerns supply chain hurdles, the resumption of normal economic activities (as the worst of the COVID-19 pandemic is put behind the world economy) should steadily allow industrial supplies and global logistics networks to catch up. These headwinds forced Lockheed Martin to reduce its guidance for fiscal 2022 in conjunction with its latest earnings update, specifically as it concerns its revenue and diluted EPS forecasts, though the defense contractor maintained its free cash flow and ‘segment operating profit’ guidance. We continue to like Lockheed Martin in the Dividend Growth Newsletter portfolio. The geopolitical backdrop (with an eye towards the Ukraine-Russia crisis, rising tensions between the US and China, and Western concerns with Iran and North Korea’s nuclear programs) is conducive for increased national defense spending in the U.S. and Western aligned nations across the globe. Lockheed Martin is well-positioned to meet those needs. Shares of LMT yield ~2.8% as of this writing.

|