By Kris Rosemann

Praxair (PX) and Linde (LNEGY) have finally agreed to tie the knot.

After two years of on-and-off negotiations, and a good deal of demand headwinds, the second and third largest industrial gas companies in terms of annual sales have signed a nonbinding agreement to a merger of equals. This isn’t the first we’ve seen of consolidation near the top of the industrial gas space, however, after the completion of Air Liquide’s (AIQUY) purchase of Airgas for ~$13 billion in May 2016 pushed it past Linde as the big kahuna in the industry in terms of annual sales. Despite a return to the top spot in the industry, the deal might be too late in helping the firms battle this round of end market cyclicality, and regulatory pressures could prove to be too much in making the deal worthwhile. Let’s dig in.

The industry consolidation we’ve seen in the industrial gas space is not an unusual byproduct of prolonged weakness in its end markets served. Suppressed energy prices and a slowdown in industrial production in recent quarters have pressured demand for Praxair’s and Linde’s industrial gas products, which include helium and oxygen for consumer-based applications from food and beverage production to industrial-based applications such as oil drilling and refining and various industrial manufacturing processes. Praxair recently cut its guidance for 2016 earnings per share, citing weakness in upstream energy and manufacturing and metals volumes in North America as reasons for its recent struggles.

Both Linde and Praxair management teams have highlighted the benefits of a combination of “Linde’s long-held leadership in technology with Praxair’s efficient operating model,” and we don’t doubt that the combined entity would be a more powerful force in the industrial gas space as a result of increased scale and the operational synergies that might come with such an increase. Scale is precisely what Praxair needs to drive higher profitability and ROIC as production and distribution density are keys to the ongoing enhancement of its business.

The to-be-formed company, which will retain the Linde name, will have roughly $30 billion in annual sales prior to divestitures, and a market cap near $67 billion. In the terms of the deal, Linde shareholders will receive 1.54 shares of the new company for each share of Linde owned, while Praxair shareholders will participate in a 1-for-1 share transaction, resulting in 50/50 ownership for each shareholder base. The combined entity expects to generate ~$1 billion in annual synergies via scale benefits, cost savings, and efficiency improvements.

The realization of targeted synergies would clearly be a positive for the combined company’s financial leverage, as a large debt load could become a concern for the firm. As of the end of the third quarter of 2016, Praxair’s net debt balance was ~$9.2 billion, while Linde’s sat at ~€7.2 billion, good for nearly $16.7 billion in net debt on a combined basis. Realizing annual synergy targets will help the firm service its debt load as it aims to continue investing in the future of the business, and the standalone companies’ net debt-to-annualized EBTIDA are at reasonable levels of ~2.8x for Praxair and ~1.8x for Linde as of the third quarter of 2016.

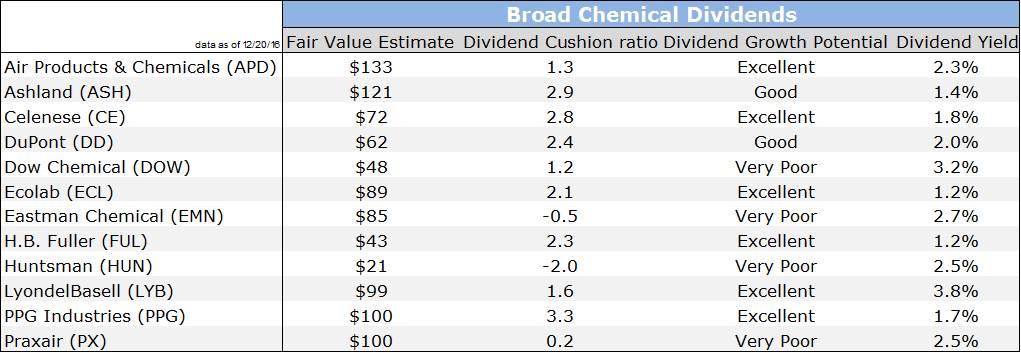

Though we expect the proposed company to be a fantastic free cash-flow generator, leverage will be worth watching closely in the context of dividend health. For example, Praxair’s Dividend Cushion ratio, a proprietary Valuentum measure, currently sits at 0.2, as the size of Praxair’s debt load weighs heavily on the coverage ratio. Shares of the company currently yield ~2.5%. Linde’s dividend coverage with free cash flow looks to be more robust than Praxair’s, based on recent results, and its financial leverage is slightly less concerning. However, a back-of-the-envelope calculation of its Dividend Cushion ratio does not paint a much brighter picture with a rough estimate coming in the ~0.3 range.

Linde’s ADRs currently yield ~2.4%, but it is important to note the impact currency translations can have on dividend payments of foreign entities. Hitting pro forma annual synergy targets would be necessary for us to have a positive opinion of the to-be-combined company’s dividend, but we are awaiting greater clarity into the terms of the deal and potential divestitures before forming a conclusion on its dividend profile. Industrial gas entities have fantastic business models, nonetheless.

Prior merger talks stalled two years ago after Linde issued profit warnings amid negotiations, and the German firm stopped discussions in September of this year over concerns of the deal structure, including the proposed headquarters and the state of German jobs. The companies have now agreed to be domiciled in a neutral member state of the European Economic Area, though Praxair CEO Steve Angel will fill his role as CEO of the new company from a separate corporate headquarters in Connecticut, and shares will be dual listed on the New York Stock Exchange and the Frankfurt Stock Exchange. Praxair has also agreed to terms that include protection from forced layoffs in Linde’s German workforce until 2022.

Since the current agreement is nonbinding, the two parties have yet to complete their internal approvals, and there is no assurance a definitive arrangement will be reached. The deal remains subject to customary shareholder and regulatory approvals, the latter of which may be easier said than done. Though the deal’s chances of getting approved in a Trump administration will be better than in an Obama administration, the regulatory fight will be a global one in this instance, and the EU has had its fair share of shine in terms of regulatory scrutiny. For example, EU regulators have halted their review of the Dow Chemical (DOW) and DuPont (DD) merger multiple times and are expected to send formal objections to the proposed creation of the world’s largest chemicals company to both parties sometime this month.

Though some are expecting strategic deal terms such as the dual listing and dual headquarters in the US and Europe to ease some regulatory pressures, the competitive landscape in the industrial gas industry may be already too concentrated near the top for the deal to get through. There are currently only four major players in the industrial gas space–Air Liquide, Linde, Praxair, and Air Products and Chemicals (APD)–so regulators should not have to look far to find cause for concern with respect to antitrust matters. Praxair generates only ~13% of total revenue in Europe, but concerns over its presence in Germany could prove to be an obstacle.

Synergy targets may also come under pressure as a result of regulatory scrutiny. Some early estimates have tabbed potential regulatory-appeasing divestitures of up to $5 billion in annual sales, and reports have already surfaced that Linde plans to separate its Engineering business–the segment accounted for nearly €2.6 billion (~$2.7 billion) in sales in 2015–into a separate legal entity. A $1 billion annual synergy target could prove to be too optimistic if early divestiture estimates are accurate, which would significantly deteriorate the appeal of the deal. Praxair has been adamant that cost cuts are core to its acquisition strategy. CFO Matthew White is on record saying, “We buy on synergies; we’re not going to buy on assumptions of growth.”

In any case, it appears as though the market is sharing our concerns over the likelihood of an effective deal getting done. Shares of Praxair were down more than 4% on the news of the agreement in intraday trading December 20, and shares of Linde were down more than 3% in trading in Frankfurt as of this writing. We’re not ruling out the possibility of the nonbinding agreement eventually resulting in a merger by any means, but investors must be aware of the regulatory risk surrounding the deal, and what a failed deal could mean for both firms as company resources are absorbed while working toward completion.

Chemicals – Broad: APD, ASH, CE, DD, DOW, ECL, EMN, FUL, HUN, LYB, PPG, PX

Chemicals – Mid/Small: ALB, FMC, GTLS, IPHS, IFF, NEU, OLN, ROL