Image: FedEx’s revenue faced significant pressure during its second quarter of fiscal 2023. Image Source: FedEx

By Brian Nelson, CFA

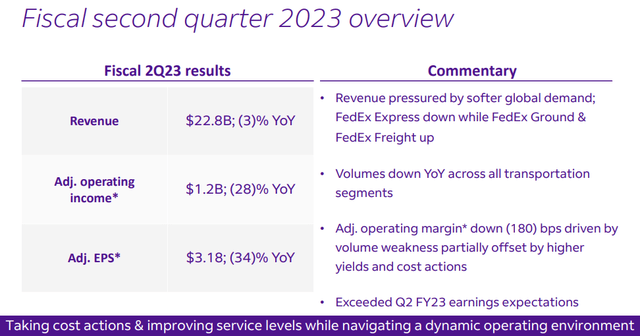

On December 20, FedEx Corp (FDX) didn’t deliver what investors wanted when it issued its fiscal second-quarter results for its fiscal 2023. Though the firm’s non-GAAP earnings per share came in slightly better than the consensus forecast, the company’s top line missed by a large margin, declining ~3% on a year-over-year basis.

We recently lowered our fair value estimate of FedEx to $214 per share from $293 per share, but even this reduced estimate may be a bit too bright given our growing concerns over its fiscal 2025 targets. We continue to be cautious on shares of FedEx in light of its weakened top-line performance and hazy outlook.

FedEx’s Fundamental Deterioration Has Been Rapid

As recently as June of this year, we had thought FedEx would be a strong consideration for the Dividend Growth Newsletter portfolio, in part because of its pricing power and lofty dividend yield, but the company’s preliminary first-quarter results led to a massive decline in its stock price as the firm withdrew its fiscal 2023 earnings forecast at the time. Here’s what the firm said back in September:

Global volumes declined as macroeconomic trends significantly worsened later in the quarter, both internationally and in the U.S. We are swiftly addressing these headwinds, but given the speed at which conditions shifted, first quarter results are below our expectations.

Though FedEx has had its share of execution issues, the company’s speed of fundamental deterioration earlier in 2022 has served — in conjunction with the weakness and inventory build across the retail sector — as one of the key reasons why we maintain our bearish tilt on the markets that continue to be locked in a technical downtrend.

That said, we continue to be fully invested across the simulated newsletter portfolios, save for a small “cash position” in the ESG Newsletter portfolio, as 1) each portfolio targets a multi-year, long-term focus via idea generation and 2) we don’t want to miss any abrupt pivot like that witnessed in 2018 when a pullback in the market was met by new highs the following year. We view support levels on the S&P 500 at 3,400, and that might mark the bottom in 2023.

Profits at FedEx Have Been Pummeled

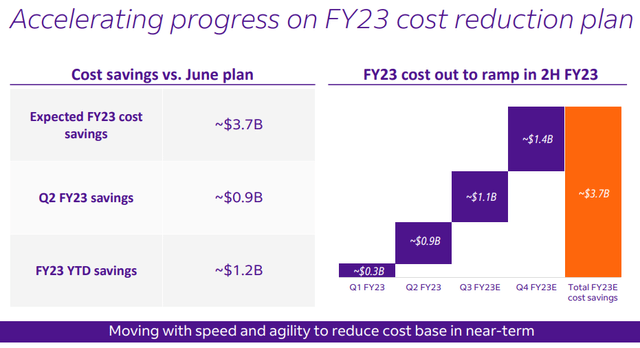

FedEx’s operating income for the second quarter of fiscal 2023 fell an incredible 64% on a year-over-year basis, as the company pointed directly to lower global volumes, despite an 8% package yield increase. The shipping giant is working hard to re-align its cost structure amid the weakening demand environment and is now targeting ~$3.7 billion in cost savings for fiscal 2023 (up an incremental $1 billion compared to its forecast released in September).

Image: FedEx continues to focus on cost savings initiatives to offset revenue weakness. Image Source: FedEx

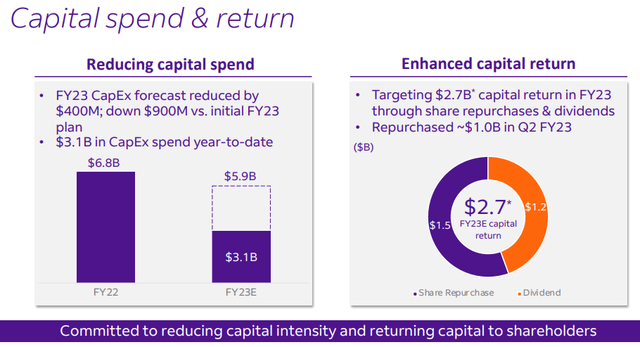

Image: FedEx has reduced its target for fiscal 2023 capital spending to $5.9 billion to shore up its cash-generating abilities amid weakness. Image Source: FedEx

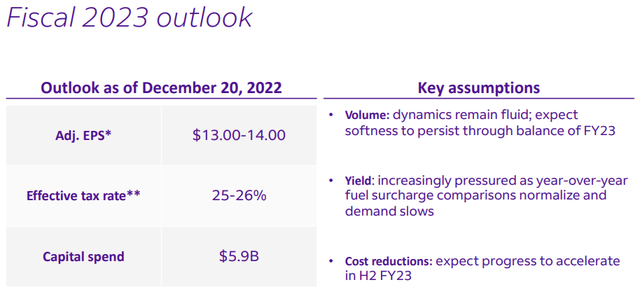

Management has also cut its forecast for capital spending in 2023 to $5.9 billion, down from $6.3 billion, and while the company hasn’t provided an official fiscal 2023 earnings per share target, excluding its mark-to-mark retirement plans accounting adjustments and costs related to business optimization/realignment initiatives, the firm is now targeting a range of $13.00-$14.00, which came in below the consensus forecast at the time.

Image: FedEx’s forecast for fiscal 2023 earnings have almost been halved since it gave guidance in June of this calendar year. Image Source: FedEx

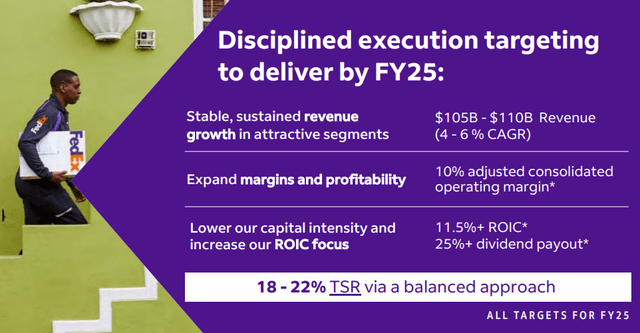

This updated range for fiscal 2023 is substantially below the $22.50-$24.50 adjusted EPS range it released in June of this year, and the magnitude of the revision leads us to believe that FedEx doesn’t have a great handle on its business trends, particularly given weakness in Europe. Still, FedEx’s financial targets for fiscal 2025 remain unchanged, but reason may suggest these goals may be a bit too ambitious, too.

Image: FedEx’s targets for fiscal 2025 were issued prior to the recent deterioration of its business. They may be too ambitious. Image Source: FedEx

Concluding Thoughts

We thought FedEx would be able to offset weakness in its business with yield and cost savings initiatives, but things have deteriorated even further than what we had been expecting. Revenue faced considerable pressure during the company’s second-quarter fiscal 2023 results, while operating income tumbled more than 60% in the period.

The firm has now cut its fiscal 2023 earnings per share forecast practically in half since it gave updated guidance in June of calendar 2022, and its financial targets for fiscal 2025 may be in jeopardy. We’re no longer evaluating FedEx for inclusion in the Dividend Growth Newsletter portfolio, despite shares yielding ~2.6% at the time of this writing.

Tickerized for FDX, UPS, FTXR, CHRW, PCAR, SUPL, IYT, XPO, JBHT, EXPD, GXO, SAIA, SNDR, TFII, ARCB, WERN, KNX

———————————————

About Our Name

But how, you will ask, does one decide what [stocks are] “attractive”? Most analysts feel they must choose between two approaches customarily thought to be in opposition: “value” and “growth,”…We view that as fuzzy thinking…Growth is always a component of value [and] the very term “value investing” is redundant.

— Warren Buffett, Berkshire Hathaway annual report, 1992

At Valuentum, we take Buffett’s thoughts one step further. We think the best opportunities arise from an understanding of a variety of investing disciplines in order to identify the most attractive stocks at any given time. Valuentum therefore analyzes each stock across a wide spectrum of philosophies, from deep value through momentum investing. And a combination of the two approaches found on each side of the spectrum (value/momentum) in a name couldn’t be more representative of what our analysts do here; hence, we’re called Valuentum.

———————————————

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, and RSP. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Be Careful With Celebrity Endorsement of Investment Products >>

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.