Image Shown: Exxon Mobil Corporation put up stellar results when reporting its second quarter earnings in late July 2022. Image Source: Exxon Mobil Corporation – Second Quarter of 2022 IR Earnings Presentation

By Callum Turcan

Exxon Mobil Corporation (XOM) posted second quarter 2022 earnings that flew past consensus top- and bottom-line estimates. The tailwind provided by elevated raw energy resources prices, rising oil & gas production volumes, ongoing cost structure improvement initiatives, and strong “crack spreads” (refining margins) more than offset headwinds arising from its decision to exit Russia in March 2022 and foreign currency headwinds due to a strong U.S. dollar.

Exxon Mobil is one of our favorite energy ideas, and we include shares of XOM in several of the newsletter portfolios as it offers investors a nice combination of dividend growth and capital appreciation upside potential. Shares of XOM yield ~3.6% as of this writing, and our fair value estimate sits at $105 per share of Exxon Mobil.

Earnings Update

In the second quarter of 2022, Exxon Mobil posted $115.7 billion in ‘total revenues and other income’ which was up 71% year-over-year. The firm’s oil & gas production, part of its ‘Upstream’ division, rose 2% year-over-year to climb over 3.6 million net barrels of oil equivalent per day (and was up 4% when removing special items). Its operations in Guyana and the Permian Basin were key to driving this production growth and should remain two of Exxon Mobil’s top oil & gas production growth drivers over the next decade. Exxon Mobil noted that “crude realizations improved 15% and gas realizations increased 23% compared to the first quarter driven by tight supply,” which helped drive its adjusted Upstream earnings up to $11.1 billion in the second quarter of 2022 versus $3.2 billion in the same period in 2021.

Looking ahead, Exxon Mobil and its partners are getting close to commencing commercial operations at the Coral South Floating LNG project in Mozambique during the second half of this year. The Italian energy firm Eni SpA (E), owned in part by the Italian government, and state-run PetroChina Company Limited (PTR) are Exxon Mobil’s key partners in this project and BP plc (BP) is set to acquire 100% of the liquified natural gas (‘LNG’) produced from the endeavor under a 20-year contract with extensions. Eni, as the lead operator, began introducing hydrocarbons to the floating LNG plant in June 2022. Natural gas is sourced from upstream operations in the Area 4 offshore concession in Mozambique.

Other partners in the Coral South FLNG project include the Portuguese energy firm Galp Energia SA (GLPEF), which is partially owned by the Portuguese government, Korea Gas Corporation (partially owned by the Korean government), and the national oil firm of Mozambique which is owned by the Mozambican government, Empresa Nacional de Hidrocarbonetos (‘ENH’). There are a lot of actors involved here. Eni is a solid operator, especially when backed up by Exxon Mobil’s expertise.

Within its second quarter earnings presentation, Exxon Mobil noted that it had secured $6.0 billion in structural cost savings versus 2019 levels and was on track to exceed $9.0 billion in annual structural cost savings by 2023. Headcount reductions are a big part of this strategy, as are various digital and automation initiatives along with corporate reorganization efforts. The firm noted in its latest earnings press release that:

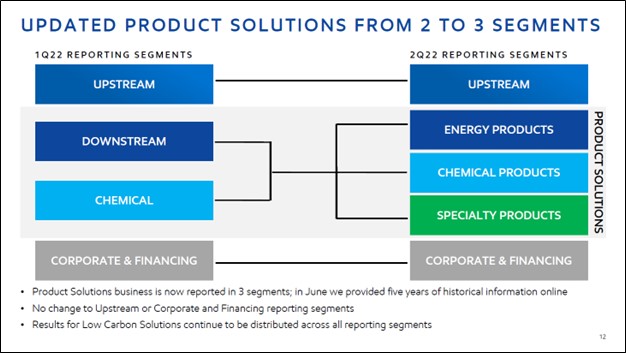

Effective April 1, to improve the effectiveness of operations and to better serve customers, [Exxon Mobil] formed ExxonMobil Product Solutions, combining world-scale Downstream and Chemical businesses. The company also centralized Technology & Engineering and Operations & Sustainability groups to further capture the benefits of technology, scale, and integration. The company has changed its segment reporting to reflect the new structure.

The upcoming graphic down below provides a visual overview of recent changes to its corporate umbrella which should help drive greater operational focus going forward.

Image Shown: Exxon Mobil’s recent corporate restructuring efforts should help drive greater operational focus at its oil refining, petrochemical, and alternative energy divisions. Image Source: Exxon Mobil – Second Quarter of 2022 IR Earnings Presentation

Looking at Exxon Mobil’s ‘Energy Products’ unit, adjusted earnings in this segment came in at $5.3 billion last quarter versus a loss of $0.9 billion in the same period in 2021. Higher oil refinery utilization rates and sales volumes combined with strong crack spreads seen of late were key. Exxon Mobil’s ‘Chemical Products’ unit posted $1.1 billion in adjusted earnings last quarter, down from $2.2 billion in the same period last year. Foreign currency headwinds and reduced margins for petrochemical product sales weighed negatively on this unit’s financial performance.

Overall, strength at its upstream and refining operations more than offset weakness at its petrochemical operations. Exxon Mobil’s performance in the second quarter of 2022 was impressive. The firm generated $17.9 billion in GAAP net income in the second quarter of this year, up almost four-fold from last year’s levels. Its adjusted non-GAAP net income came in at $17.6 billion last year, also up almost four-fold from last year’s levels. Exxon Mobil’s GAAP and non-GAAP adjusted diluted EPS stood at $4.21 and $4.14, respectively, last quarter. Looking ahead, as the outlook for raw energy resources pricing remains robust and crack spreads have been quite strong of late, Exxon Mobil’s financial performance should continue to impress in the current environment.

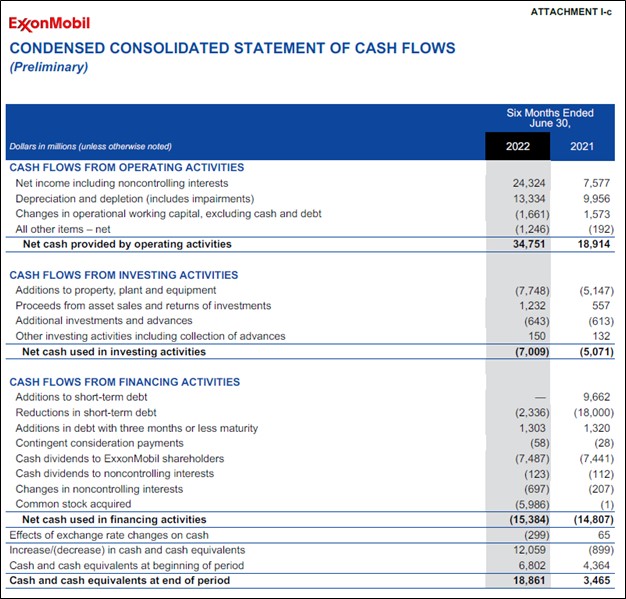

Exxon Mobil generated $27.0 billion in free cash flow during the first half of 2022, up from $13.8 billion in the same period in 2021. The firm spent $7.6 billion covering its total payout obligations and another $6.0 billion buying back its stock in the first half of this year, with the remainder used to further improve Exxon Mobil’s balance sheet health. Exxon Mobil is keeping a lid on its capital expenditures, when compared to its large net operating cash flow generating abilities, to better enable it to churn out “gobs” of free cash flow in the current environment. During the company’s second quarter earnings call, management reiterated Exxon Mobil’s plan to spend $21.0-$24.0 billion on capital expenditures this year.

Image Shown: Exxon Mobil generated “gobs” of free cash flow during the first half of 2022. Image Source: Exxon Mobil – Second Quarter of 2022 Earnings Press Release

At the end of June 2022, Exxon Mobil had a net debt load of $28.0 billion (inclusive of short-term debt), with its $18.9 billion in cash and cash equivalents on hand at the end of this period providing it with ample liquidity to meet its near term funding needs. For reference, Exxon Mobil had $63.8 billion in net debt on the books at the end of December 2020 (inclusive of short term debt). One of the reasons why we are huge fans of Exxon Mobil is its past deleveraging efforts.

During Exxon Mobil’s latest earnings call, management noted that the firm’s gross debt to capital ratio of ~20% at the end of the second quarter was at the low end of its targeted range. That figure sat at ~13% on a net debt basis at the end of June 2022. Management also noted that Exxon Mobil was “on track with our program to repurchase up to $30 billion of shares through 2023,” and its past deleveraging efforts should help enable the firm to return cash to shareholders in a sustainable manner when also taking its immense cash flow generating abilities into account.

Divestiture Updates

The company sold its Barnett shale gas assets through a $0.75 billion deal that closed in June 2022, adding $0.3 billion to its earnings last quarter. Exxon Mobil divested a mature legacy asset with limited production growth opportunities by parting ways with its upstream Barnett position, which has a higher cost of supply than its nearby Permian Basin position. Over the next decade or so, natural gas production from this asset will likely continue to fade given the lack of attractive investment opportunities.

In June 2022, Exxon Mobil and Imperial Oil Ltd (IMO), which is majority-owned by Exxon Mobil, announced the sale of XTO Energy Canada, which jointly owned by Imperial Oil and Exxon Mobil Canada. The asset sale is expected to close in the third quarter of this year and will raise ~$1.5 billion for the group. Within this package includes upstream operations in the Duvernay and Montney shale plays with ample production growth upside. However, these assets are currently producing a relatively modest amount of oil & gas and it would require sizable capital expenditures to further develop these resources.

Exxon Mobil is also working towards selling its Romanian upstream operations through a deal announced in May 2022 that is expected to close this year. The company noted the asset sale was “for more than $1 billion” and originally was expected to close last quarter, though Exxon Mobil pushed the timetable back modestly during its latest earnings update. Exxon Mobil Exploration and Production Romania and the firm’s interest in the XIX Neptun Block, a deepwater exploration block in the Black Sea, are being sold off as part of this deal. As Exxon Mobil already has a vast resource base to develop, especially in the wake of its successes in Guyana (in this year alone, Exxon Mobil has already achieved an additional seven discoveries as of July 2022), the firm is fine-tuning its global exploration footprint.

Concluding Thoughts

We liked what we saw in Exxon Mobil’s latest earnings update. The company is remaining disciplined as it concerns its capital allocation priorities and Exxon Mobil should continue to churn out gobs of free cash flow in the current environment. Share buybacks, in moderation, are a good use of capital as we view shares of Exxon Mobil as trading well below our estimate of their intrinsic value as of this writing. The top end of our fair value estimate range sits at $136 per share of Exxon Mobil. Additionally, we see ample room for Exxon Mobil to further grow its per-share dividend going forward in a sustainable manner, aided by the significant reduction in its net debt load since the end of December 2020 and ongoing cost structure improvement initiatives.

Exxon Mobil is a stellar enterprise that has been doing great of late. We continue to like Exxon Mobil in the simulated portfolios of the Best Ideas Newsletter, Dividend Growth Newsletter, and High Yield Dividend Newsletter.

—–

Oil and Gas Complex Industry – BKR, HAL, SLB, BP, CVX, COP, XOM, SHEL, TOT, COG, EOG, OXY, PXD, ENB, ET, EPD, MMP, KMI, PSX

Related: E, GLPEF, PTR, IMO, XLE

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares in DIS, META, GOOG, VRTX, and XLE and is long call options on DIS, GOOG, META, MSFT, V, and VRTX and is long put options on RDFN and RKT. Energy Select Sector SPDR Fund ETF (XLE) is included in Valuentum’s simulated Best Ideas Newsletter portfolio. Chevron Corporation (CVX) and ExxonMobil Corporation (XOM) are both included in Valuentum’s simulated Best Ideas Newsletter portfolio, simulated Dividend Growth Newsletter portfolio, and simulated High Yield Dividend Newsletter portfolio. Enterprise Products Partners L.P. (EPD) and Magellan Midstream Partners L.P. (MMP) are both included in Valuentum’s simulated High Yield Dividend Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.