Member LoginDividend CushionValue Trap

|

Value Is Not Static and the Qualitative Overlay Is Vital to Our Process

publication date: Nov 16, 2020

|

author/source: Brian Nelson, CFA

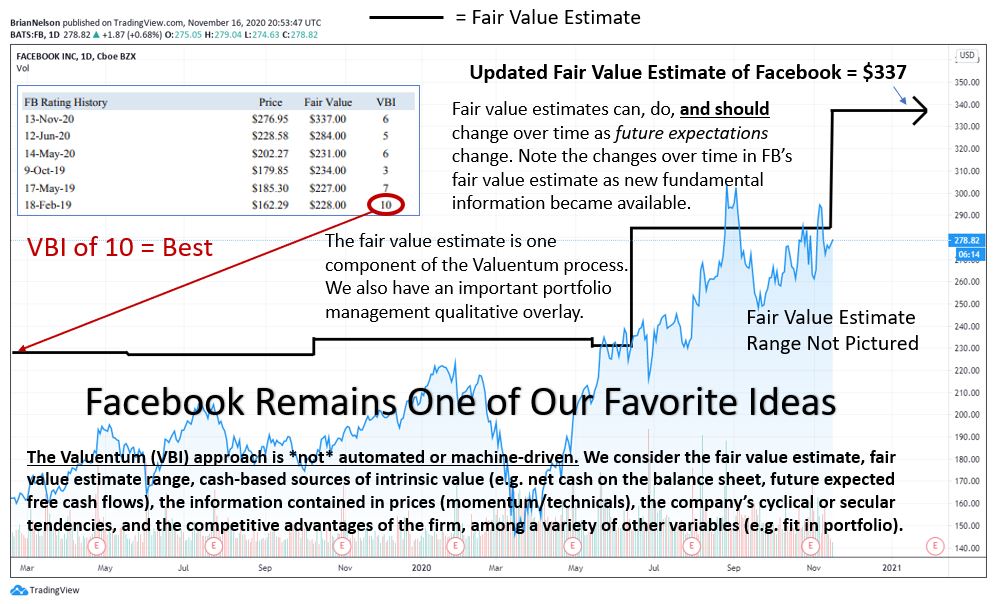

Note: We recently raised our fair value estimate of Facebook to $413 per share December 2, 2020. Its stock page can be accessed here. The following article is for informational purposes only and was published November 16, 2020. With prudence and care, the Valuentum Buying Index process and its components are carried out. Our analyst team spends most of its time thinking about the intrinsic value of companies within the context of a discounted cash-flow model and evaluating the risk profile of a company's revenue model. We have checks and balances, too. First, we use a fair value range in our valuation approach as we embrace the very important concept that value is a range and not a point estimate. A relative value overlay as the second pillar helps to add conviction in the discounted cash-flow process, while a technical and momentum overlay seeks to provide confirmation in all of the valuation work. There's a lot happening behind the scenes even before a VBI rating is published, but it will always be just one factor to consider. Within any process, of course, we value the human, qualitative overlay, which captures a wealth of experience and common sense. We strive to surface our best ideas for members. By Brian Nelson, CFA Sometimes our members notice a fair value estimate change on one of their stocks, and we wanted to explain the key drivers behind why fair value estimates can, should and do change. The image above shows how the fair value estimate for Facebook (FB) has changed over time, and the following is a slightly modified excerpt from our book Value Trap that covers the topic. Share prices, which are driven by the buying and selling of stock, are not static, and neither are fair value estimates. When important drivers within the enterprise cash flow model change or when new information comes to light, fair value estimates can and should change, much like the prices themselves. Though there are perhaps an infinite number of reasons why a fair value estimate can change, there are generally two primary reasons that account for most fair value estimate revisions: 1) “rolling the model forward,” and 2) significant changes in expectations or transformative acquisitions. Modest tweaks in fair value estimates within the enterprise valuation process may occur when an analyst rolls a company’s model forward one year. This occurs when Year 1 of the model changes from, say, 2019 to 2020. The timing of this revision generally occurs after a company issues its fiscal annual report (form 10-K or form 20-F). For most companies, this would occur late in the first quarter, as audited new information for the last fiscal year (which is released in the form 10-K or form 20-F) is entered into the model. Generally speaking, if forecasts have been relatively accurate in setting the original fair value estimate, the fair value estimate should theoretically increase by its discount rate less the dividend yield each year, all else equal, through the course of the year. This phenomenon is caused by what is called the time value of money (as companies collect cash through the year, their value increases, net of cash going out the door, the dividend payment), and because of the steady advancement in value through the course of the year, there may actually only be modest tweaks to an estimate of intrinsic value when rolling the model forward, in most cases. It’s important to note, however, that as future expectations are always changing, so is the iterative value estimate of the company through the year, with the passing of time providing an upward bias (e.g. larger cash flows are brought closer to the present with the passing of time, assuming the company is growing). The time value of money nonetheless forms the backbone of why equity values generally advance over time, consistent with stock prices having drifted upward through the course of history (or the market factor). If you recall, Fama and French’s three-factor model included the B/M ratio for value, size, and a market factor to try to explain the cross-section of stock returns, but both the B/M ratio and the size factor have since become less important considerations. It’s possible at times that the trajectory of the company’s future free cash flow stream and its capital structure can experience more material changes as they are refined with the new information in the 10-K or 20-F. For example, if a company has engaged in value-destructive activities during the previous year (e.g. it has overpaid for acquisitions or bought back its own stock at egregious prices), this may show up more vividly in the new fair value estimate. On the other hand, if a company is a wise capital allocator, the company’s balance sheet and future cash flow trajectory may have been enhanced from the previous year. This may cause an upward revision in the fair value estimate (sometimes by 10% or more), all else equal, once these value-creating buybacks are incorporated. When rolling the model forward, there are a near-infinite number of drivers (factors) that could influence a fair value estimate of a stock, though changes in the balance sheet (specifically the net cash or net debt position) and revisions in the future enterprise free cash flow stream (revenue, earnings before interest, capital spending, working capital and other components) are among the greatest causes of change. However, most of the drivers behind a change in a fair value estimate resulting from rolling the model, should be operational (e.g. updating the cash flow trajectory and accounting for cash generated during the previous year as reflected in the updated balance sheet and/or lower share count). It may not be wise to adjust a firm’s cost of equity often or to adjust the risk-free rate frequently, even if such adjustments may happen in some cases, as these more subjective considerations could muddy a cleaner operating assessment of value. Though the fundamental-adjusted CAPM still has shortcomings, the very idea of a pure application of quantitative beta, which may be ever-changing with prices, almost precludes its use under any reasonable valuation framework. Fair value estimates and, by relation, the enterprise valuation process is forward looking, meaning that when expectations of a company’s future free cash flow stream are revised because of forward guidance revisions, or when a company pursues a transformative acquisition that will materially change its capital structure in the future, the fair value estimate should change accordingly. [Changes in future expectations within the discounted cash-flow construct are what has driven most of the fair value estimate revisions in Facebook, as shown in the illustration above.] The variables that may cause the biggest changes in the fair value estimate on an operating level are generally forecasts of a company’s mid-cycle operating margin (year 5) expectations, mid-cycle revenue growth rate (year 5), and capital spending over the 5-year discrete forecast period (or what can be described as the first phase of the model). That is not to say that, if a company comes out with substantially lower revenue and earnings guidance for the current year than what the analyst had been modeling, there shouldn’t be a downward revision in the company’s fair value estimate. The early years of the forecasts within an enterprise valuation model, however, generally do not impact the fair value estimate materially in most cases, but the information behind the revised guidance could influence the intermediate-term and even the long-term forecasts of the model (think “ripple” or “cascade” effect), and this would cause an even larger fair value estimate revision (in some cases). Whenever the trajectory of the future enterprise free cash flow stream changes, the fair value estimate, which is based on the future enterprise free cash flows, changes, and generally so should the price of the equity. --- Tickerized for the Russell 2000 ETF (IWM). Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free. Brian Nelson owns shares in SPY, SCHG, DIA, VOT, and QQQ. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies. |

0 Comments Posted Leave a comment