Executive Summary: Ford has been a solid performer in the portfolio of the Best Ideas Newsletter. Though 2014 may not be its best year, we think the best times at the company are still ahead of it. A sub-10 trailing earnings multiple is too harsh, even after considering operational (cyclicality) and financial (Ford Motor Credit) risks.

We couldn’t be happier with Ford’s (F) performance during 2013, results released January 28. Full-year 2013 pre-tax profit of $8.6 billion advanced more than $600 million from the mark in the same period a year ago and represented one of Ford’s best years ever. The company’s full-year earnings per share of $1.62, which jumped $0.21 from the same period last year, implies a trailing price-to-earnings ratio of less than 10 times (based on the company’s price at the time of this writing).

Worldwide, Ford’s pension plans are underfunded by only $9 billion at year-end 2013 (or just over $2 per share), and the automaker ended the year with ‘Automotive’ gross cash of $24.8 billion, exceeding debt by $9.1 billion. From an analytical standpoint, Ford could wipe clean the under-fundedness in one fell swoop of a cash injection, meaning that the balance sheet (including pension considerations) should not warrant such a large punitive effect on Ford’s earnings multiple.

Image Source: Ford

Though the inherent cyclicality of its operations and the risks related to its captive finance arm (Ford Motor Credit) may reduce the ‘appropriate’ earnings multiple to place on its earnings stream relative to a steady-eddy mature stalwart with no financial-related risk, a sub-10 times trailing earnings multiple is frankly a bit too harsh. Our fair value estimate of $21 per share (at the time of this writing) implies a 13 times trailing multiple, which we think is more appropriate while also capturing the embedded discount associated with the operational (cyclicality) and financial (finance arm) risk inherent to the company’s operations.

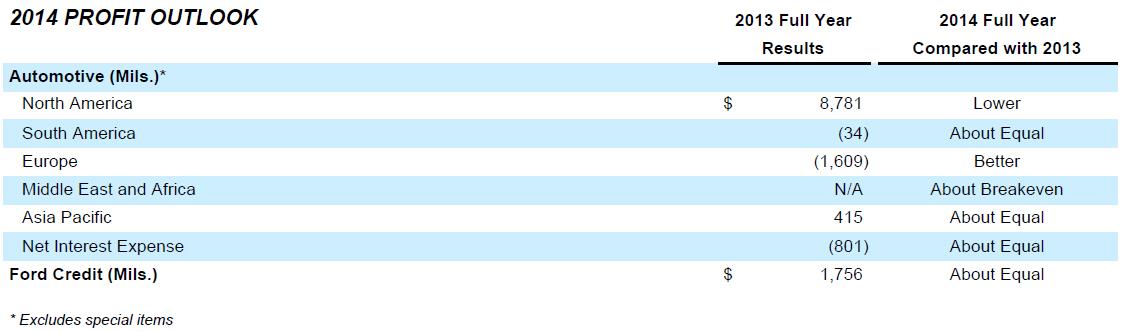

Looking ahead, Ford reiterated its outlook for 2014:

In 2014, Ford is continuing to invest to create innovative products such as the all-new F-150 to ensure Ford has the freshest and most attractive product line-up in the industry. At the same time, Ford is investing to expand its portfolio into new markets, as well as adding capacity, where appropriate, to satisfy increasing demand.

Ford expects another solid year with total company pre-tax profit to range from $7 billion to $8 billion; Automotive revenue to be about the same as last year; Automotive operating margin to be lower; and Automotive operating-related cash flow to be positive but substantially lower than 2013.

Valuentum’s Take

Though investments (which will pressure earnings) and commentary regarding ‘Automotive’ operating-related cash flow in 2014 have caused a couple hiccups in investor optimism, we think the best years at Ford are still ahead of it (even if 2014 may not one of them). We think investors should place a greater emphasis on pent-up demand than on performance in any one year, as we estimate that as many as 16+ million new car unit sales from the period of 2008-2011 were deferred (see here). Even after adjusting for a shift to used cars during this time period, we don’t think the lost unit sales during the Great Recession are anywhere near being satisfied. Other estimates for roughly 4-5 million in deferred units during the Great Repression appear too low, but even these estimates are not yet satisfied, in our view. We maintain our view that Ford’s shares have substantial upside potential, if only on the basis of its valuation. The company remains a holding in the portfolio of the Best Ideas Newsletter.