Image: Meta’s free cash flow remains robust despite higher capital spending.

By Brian Nelson, CFA

On July 30, Meta Platforms (META) reported blockbuster second quarter results with revenue and GAAP earnings per share exceeding the consensus forecast. Revenue grew 22% on a year-over-year basis, to $47.5 billion (consensus was $44.8 billion) while costs and expenses rose at a more modest 12% rate in the quarter, driving a 38% increase in income from operations. Meta’s operating margin rose roughly 5 percentage points, to 43%. Net income increased 36% in the quarter, while diluted earnings per share rose 38%, to $7.14 (consensus was $5.90).

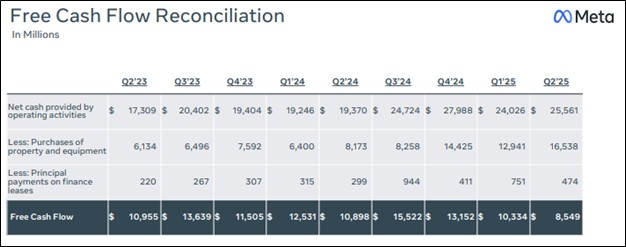

Meta’s family daily active people (DAP) on average for June 2025 increased 6%. Ad impressions delivered across its Family of Apps increased 11%, while average price per ad increased 9% year-over-year. During the quarter, share repurchases totaled $9.76 billion, while total dividend payments were $1.33 billion. Cash flow from operating activities was $25.56 billion, while capital expenditures, including principal payments on finance leases, were $17.01 billion, resulting in free cash flow of $8.55 billion in the quarter. As of June 30, cash and marketable securities were $47.07 billion. Long-term debt totaled $28.83 billion.

Looking to the third quarter of 2025, Meta Platforms expects revenue to be in the range of $47.5-$50.5 billion (consensus was $44.8 billion), revealing sequential growth at the midpoint relative to second quarter numbers. The company’s guidance assumes a 1% tailwind to revenue growth from foreign currency, based on current exchange rates. Meta fell short of providing an outlook for fourth quarter revenue, but it noted that its year-over-year growth rate for the quarter will be slower than the third quarter as it laps a period of stronger growth in the fourth quarter of last year.

Meta expects full year 2025 total expenses to be in the range of $114-$118 billion, narrowed from its prior outlook of $113-$118 billion and reflecting a growth rate of 20%-24% year-over-year. The social media giant expects 2025 capital expenditures, including principal payments on finance leases, to be in the range of $66-$72 billion, narrowed from its prior outlook of $64-$72 billion and up roughly $30 billion year-over-year at the mid-point.

Meta’s year-over-year expense growth rate for 2026 is expected to be higher than that of 2025 due to infrastructure costs and employee compensation. Management expects similarly significant capital expenditure dollar growth in 2026 as it continues to aggressively pursue opportunities in artificial intelligence and general business operations. We liked the quarterly results at Meta, and the company’s core business is significantly more profitable than reported income numbers due to losses at Reality Labs. The big beat in terms of revenue growth guidance for the third quarter was also reassuring. Though Meta is not a large dividend payer, we think its dividend growth prospects are fantastic.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, QQQM, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, QQQM, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.