Image Source: Taiwan Semiconductor Manufacturing Company – First Quarter of 2022 IR Earnings Presentation

By Callum Turcan

Semiconductor components, or “chips,” are the bedrock of the digital economy. Taiwan Semiconductor Manufacturing Company (TSM) operates numerous semiconductor fabrication sites all of the world, with its major manufacturing hub located in Taiwan, that produce chips utilized in all sorts of applications. Furthermore, Taiwan Semi is one of only a handful of companies capable of producing high-end chips at scale. Taiwan Semi’s business model revolves around producing chips for third-parties as the firm does not design semiconductor components itself, and the company is the largest semiconductor foundry in the world (foundries are chip fabrication sites specifically built to meet third-party needs).

We are huge fans of Taiwan Semi which offers investors a combination of capital appreciation and income growth upside. Shares of TSM yield ~2.1% as of this writing. Taiwan Semi is included as an idea in our ESG Newsletter portfolio (more on that publication here). The firm is incredibly shareholder friendly with good governance practices, focuses on sustainable manufacturing practices where feasible (placing a great emphasis on effective resource management, limiting pollution, and utilizing green energy), and has a management team that comes from diverse backgrounds (keeping in mind Taiwan Semi is headquartered in Hsinchu, Taiwan).

First, some quick housekeeping items. Taiwan Semi reports its financials in New Taiwan dollars terms, though it provides some financial items in US dollar terms at a specified exchange rate for the convenience of US-based readers. Additionally, the firm reports its financials in accordance with Republic of China (‘ROC’) generally accepted accounting practices (‘GAAP’), which differs somewhat from US GAAP rules. Taiwan Semi pays out a quarterly dividend in New Taiwan dollars, and each American Depository Receipt (‘ADR’) represents five common shares of Taiwan Semi.

Financial Overview

Over the past few years, Taiwan Semi’s business has boomed. Demand for consumer electronics and PCs surged during the initial phases of the coronavirus (‘COVID-19’) pandemic while demand for data centers and smartphones remained robust, driving up demand for semiconductor components. Additionally, automobiles are requiring substantial increases in computing power and the Internet of Things (‘IoT’) trend is adding computing power to products that previously had little to none (such as appliances), creating another source of demand growth for chips.

Due to semiconductor demand vastly outstripping supply, a situation that is slowly resolving itself but continues to this day, Taiwan Semi has been able to push through sizable pricing increases to offset inflationary pressures, supply chain hurdles, and other headwinds. In May 2022, Taiwan Semi reportedly told its customers to expect another round of pricing increases to kick in next year. This comes on the heels of its major pricing increase announcement in August 2021, and so far, demand has held up quite well due to the essential nature of its offerings and lack of serious alternatives.

From 2019-2021, Taiwan Semi’s revenues rose by 48% in New Taiwan dollar terms and its gross margin expanded by ~560 basis points to reach 51.6%. Revenue growth and gross margin expansion created a powerful combination for its operating income and net income, which grew by 74% and 67%, respectively, during this period. In US dollar terms, Taiwan Semi’s revenues stood at US$57.2 billion, its operating income stood at US$23.4 billion, and its net income stood at US$21.4 billion in 2021.

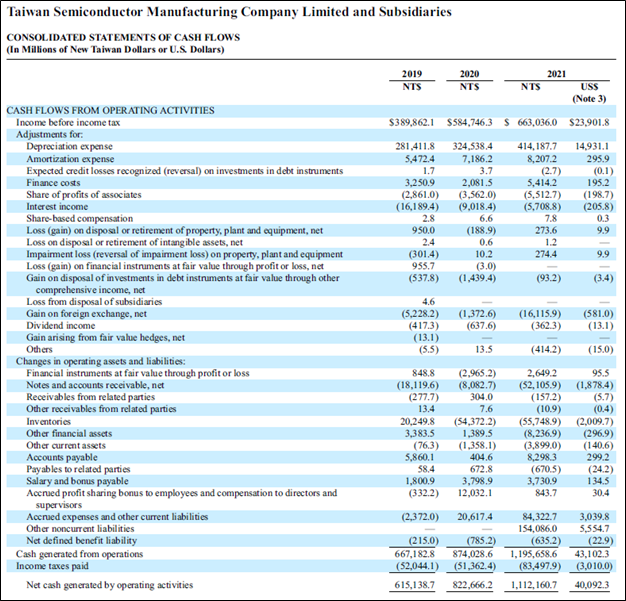

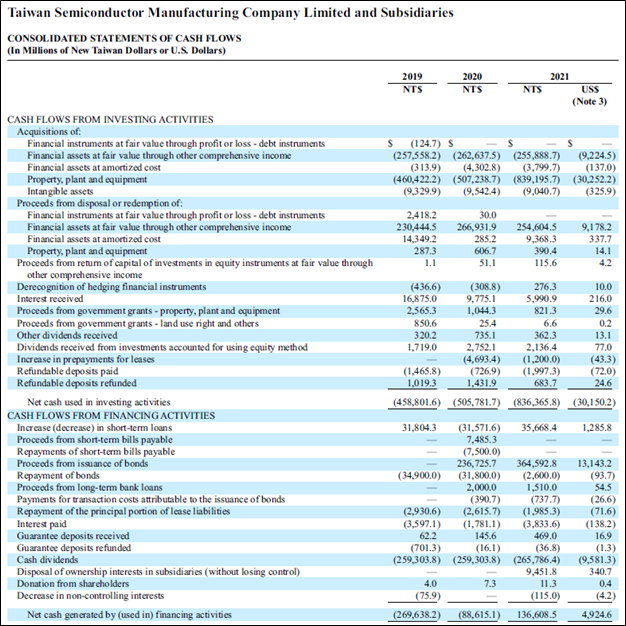

The company is a cash flow generating powerhouse, though its capital expenditures increased substantially in 2021 over 2019-2020 levels as Taiwan Semi seeks to scale up its global manufacturing capabilities. In 2021, Taiwan Semi announced it would invest ~$100 billion over the next three years towards manufacturing capacity increases and R&D activities to better meet booming global demand for chips. Last year, Taiwan Semi generated US$40.1 billion in net operating cash flow and spent US$30.3 billion on capital expenditures, allowing for US$9.8 billion in free cash flow which fully covered US$9.6 billion in dividend obligations during this period. It did not spend a significant amount repurchasing its stock last year.

Images Shown: Taiwan Semi is a tremendous cash flow generator and possesses the financial strength to organically fund major investments in its manufacturing and R&D operations to better meet surging global demand for semiconductor components. Images Source: Taiwan Semi – 2021 20-F SEC Filing

Some of Taiwan Semi’s growth ambitions involve building a chip manufacturing hub in Arizona, another manufacturing hub in Japan, and scaling up production capacity at its enormous chip manufacturing complexes in Taiwan. Given the secular tailwinds supporting demand for semiconductor components, we view its medium-term expansion plans favorably as these efforts underpin Taiwan Semi’s bright longer term cash flow growth outlook.

Latest Earnings

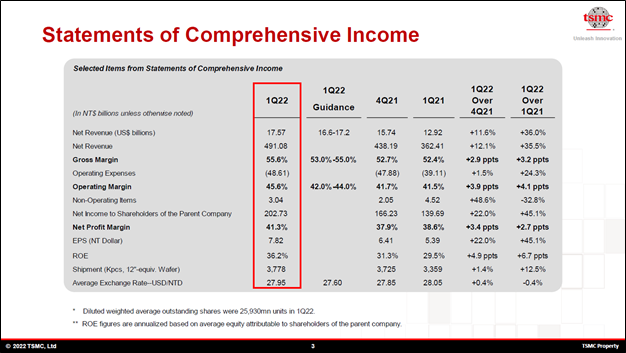

When Taiwan Semi reported first quarter 2022 earnings in mid-April, the company beat both consensus top- and bottom-line estimates. Its revenue boomed higher by 36% year-over-year and its gross margin expanded by ~320 basis points to reach 55.6% in the first quarter as the uplift from pricing increases, shipment volume growth, and greater economies of scale bolstered its financial performance. Taiwan Semi’s operating income rose by 49% year-over-year and its operating margin expanded by ~310 basis points to reach 45.6% in the first quarter.

On a standardized basis, Taiwan Semi noted its shipment volumes grew by just under 13% year-over-year and were up over 1% on a sequential basis in the first quarter as it continued to ramp up its manufacturing capabilities. Taiwan Semi’s solid operational performance of late has translated into steady improvements in its financial performance.

Image Shown: An overview of Taiwan Semi’s financial performance during the first quarter of 2022. Image Source: Taiwan Semi – First Quarter of 2022 IR Earnings Presentation

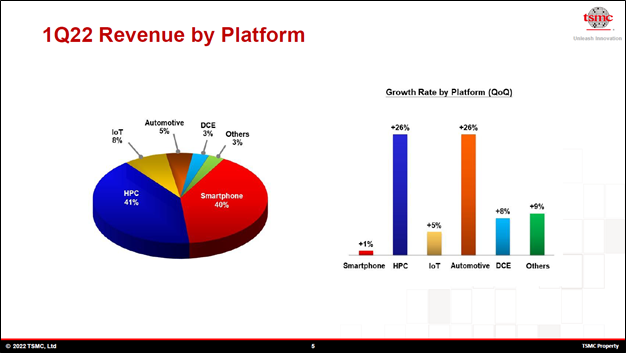

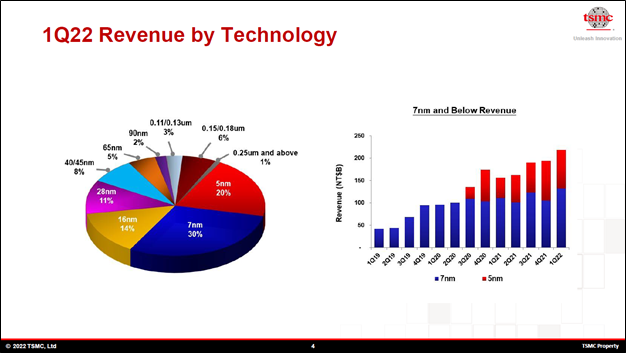

Management noted that “advanced technologies” such as 5nm and 7nm chips (with the measurement representing the space between transistors) represented about half of Taiwan Semi’s revenues in the first quarter. Chips utilizing 5nm technology are the leading edge of the semiconductor space in terms of components produced at scale, and there are efforts to develop 2nm and 3nm chips as well. A lot of Taiwan Semi’s pricing strength comes from its ability to produce cutting edge chips at scale, with its major competitor in this space being Samsung Electronics Co Ltd (SSNLF). Intel Corporation (INTC) is spending heavily to catch up but remains well behind Taiwan Semi and Samsung, and it will take years before Intel is a serious player in the semiconductor foundry space (a realm Intel decided to enter under its new CEO).

Taiwan Semi is well-positioned to meet chip demand across cutting edge and legacy technologies, and its major investments in R&D will help the firm stay ahead of the curve (the firm spent over 7% of its revenues on R&D in the first quarter). Strong automotive-related and high-performance computing (‘HPC’) demand supported Taiwan Semi’s first quarter performance according to management. Technologies utilizing artificial intelligence and autonomous driving capabilities require a lot of computing power.

Image Shown: Half of Taiwan Semi’s revenues came from manufacturing and selling leading edge chips in the first quarter. The company is well-positioned to meet demand for both legacy and cutting edge semiconductor components. Image Source: Taiwan Semi – First Quarter of 2022 IR Earnings Presentation

At the end of March 2022, Taiwan Semi had US$14.6 billion in net cash on the books (inclusive of short-term debt). That figure does not include US$4.6 billion in current ‘investments in marketable financial instruments’ and US$1.6 billion in noncurrent ‘long-term investments’ on hand at the end of this period which further bolsters its net cash-like position.

We are huge fans of Taiwan Semi’s fortress-like balance sheet. The firm has a stellar ‘A-rated’ investment grade credit rating (Aa3/AA-) with stable outlooks.

Taiwan Semi generated US$3.9 billion in free cash flow in the first quarter which fully covered US$2.6 billion in dividend obligations along with $0.1 billion in share repurchases. Even in the wake of its capital expenditure expectations shifting materially higher, Taiwan Semi continues to churn out “gobs” of free cash flow which we appreciate.

Guidance

Looking ahead, Taiwan Semi provided favorable guidance for the second quarter that calls for US$17.6-US$18.2 billion in revenue, a gross margin of 56%-58%, and an operating margin of 45%-47%. At the midpoint, this guidance represents 2% revenue growth (in US dollar terms), gross margin expansion of ~140 basis points, and operating margin expansion of ~40 basis points on a sequential basis. On a year-over-year basis at the midpoint, this guidance represents 35% revenue growth (in US dollar terms), a ~700 basis point expansion in its growth margin, and a ~690 basis point expansion in its operating margin. Management noted that continued strength from automotive-related and HPC demand was expected to support Taiwan Semi’s performance in the second quarter, offsetting expected headwinds from seasonal factors impacting smartphone-related sales.

During Taiwan Semi’s first quarter of 2022 earnings call, management had this to say on the firm’s near term guidance and profitability performance (emphasis added):

“Now let me turn to our key messages. I will start by making some comments on our first quarter and second quarter profitability. As a reminder, 6 factors determine TSMC’s profitability: leadership technology development and ramp-up, pricing, cost reduction, capacity utilization, technology mix and foreign exchange rate. As we discussed earlier, our first quarter gross margin increased by 290 basis points sequentially to 55.6%, mainly due to cost improvement and value-selling efforts and a more favorable foreign exchange rate.

Our gross margin guidance provided 3 months ago was based on exchange rate assumption of USD 1 to TWD 27.6, whereas the actual first quarter exchange rate was USD 1 to TWD 27.95. This created about 50 basis point difference in our actual first quarter gross margin versus our original guidance. We have just guided our second quarter gross margin to further increase by 140 basis points sequentially to 57% at the midpoint primarily due to a more favorable exchange rate assumption of USD 1 to TWD 28.8, which brings more than 100 basis points gross margin tailwind, and continued cost improvement and value-selling efforts.

Looking ahead on our profitability, we continue to face challenges from rising inflationary costs, increasing process complexity of leading nodes, new investments in mature nodes and overseas fab expansions. Despite the manufacturing cost challenges and excluding the impact of foreign exchange rate, of which we have no control over, taking the other 5 factors into consideration, we continue to believe a long-term gross margin of 53% and higher is achievable.” — Wendell Huang, VP and CFO of Taiwan Semi

We appreciate Taiwan Semi’s confidence in its near term performance and ability to maintain its longer term gross margin targets.

Concluding Thoughts

The selloff in equities seen this year has pushed shares of TSM lower though Taiwan Semi’s fundamental performance remains rock-solid. Its revenues are growing robustly, and its margins have expanded nicely of late. Demand for chips is supported by numerous secular tailwinds and given that only a handful of companies are capable of producing high-end semiconductor components at scale (primarily Taiwan Semi and Samsung), Taiwan Semi has a bright growth outlook backed up by its tremendous pricing power. Rising capital expenditure expectations in the medium-term will weigh negatively on its free cash flow generating abilities, though the firm has continued to churn out “gobs” of free cash flow so far. Its fortress-like balance sheet provides it with ample financial firepower.

We continue to like Taiwan Semi as an idea in our ESG Newsletter portfolio. Our fair value estimate sits at $123 per share of TSM with room for upside. Shares of TSM are trading at the low end of our fair value estimate range (which sits at $92 per share) as of this writing. Taiwan Semi’s Dividend Cushion ratio sits well above parity at 1.8 due to its strong balance sheet (i.e., net cash position) and impressive cash flow generating abilities, earning it a “GOOD” Dividend Safety rating. As we view its dividend growth outlook quite favorably, we assign Taiwan Semi an “EXCELLENT” Dividend Growth rating. Its dividend growth track-record is rock-solid. The company offers investors a nice combination of capital appreciation and income growth upside and complies with ESG investing standards.

Downloads

—–

Technology Giants Industry – FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI

Tickerized for ASML, TSM, SSNLF, INTC, and various holdings in the SMH.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares of DIS, FB, GOOG, VRTX, and XLE and is long DIS and FB call options. Apple Inc (AAPL), Cisco Systems Inc (CSCO) and Microsoft Corporation (MSFT) are all included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares, Meta Platforms Inc (FB), Korn Ferry (KFY), PayPal Holdings Inc (PYPL) and Visa Inc (V) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Oracle Corporation (ORCL) and Qualcomm Inc (QCOM) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. ASML Holding NV (ASML), Meta Platforms, Oracle, and Taiwan Semiconductor Manufacturing Company Limited (TSM) are all included in Valuentum’s simulated ESG Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.