Image Source: Cisco Systems Inc – 2021 Investor Day Event Presentation

By Callum Turcan

Things at Cisco Systems Inc (CSCO) are beginning to turn around and management made sure to highlight the company’s improving outlook during its big Investor Day event held on September 15. We include Cisco Systems as an idea in both the Best Ideas Newsletter and Dividend Growth Newsletter portfolios as the firm has a fortress-like balance sheet (i.e., large net cash position), tremendous free cash flow generating abilities, and its growth outlook has improved immensely since contending with serious headwinds from the worst of the coronavirus (‘COVID-19’) pandemic. Shares of CSCO yield ~2.6% as of this writing.

On the hardware front, Cisco Systems sells products in the realm of switching, routing, wireless, data centers and more that are primarily geared towards supporting network operations (including cloud-computing, 5G, and Wi-Fi 6 operations). On the software front, Cisco Systems sells offerings in the realm of cybersecurity, collaboration, applications monitoring, Internet of Things (‘IoT’), customer experience-as-a-service (‘CXaaS’), analytics solutions, and more.

Overview

Cisco Systems is a tremendous generator of free cash flow. From fiscal 2019 to fiscal 2021, keeping in mind its fiscal year ends in late July, the firm generated on average $14.8 billion in free cash flow per fiscal year while exiting fiscal 2021 with $6.1 billion in run-rate dividend obligations. At the end of fiscal 2021, Cisco Systems had a net cash position of $13.0 billion (inclusive of short-term debt). We are enormous fans of Cisco Systems’ stellar free cash flow generating abilities and fortress-like balance sheet.

However, we will caution that the company’s GAAP revenues dropped by 4% from fiscal 2019 to fiscal 2021, even after a series of acquisitions were completed during this period. Declining sales combined with a weakening of its GAAP gross margin and modest operating expense growth saw the company’s GAAP operating income drop 10% from fiscal 2019 to fiscal 2021. Though headwinds from the COVID-19 pandemic are partially responsible, part of this dynamic comes down to the hurdles Cisco Systems has faced in transitioning its business model towards software, cloud-based services, and recurring revenue streams. More recently, the company has started to gain some real traction on this front while demand for its hardware offerings has held up rather well (keeping headwinds from the ongoing semiconductor shortage in mind).

Growth Outlook Improving

What management communicated during Cisco Systems’ Investor Day event held on September 15 was that the company had finally turned a corner. Looking ahead, Cisco Systems expects that its revenue and earnings will steadily improve over the coming fiscal years, aided by forecasted growth in its subscription revenues. For example, expected growth at offerings such as its video conferencing and workforce collaboration service Webex in the wake of the proliferation of the hybrid work dynamic represents part of this strategy.

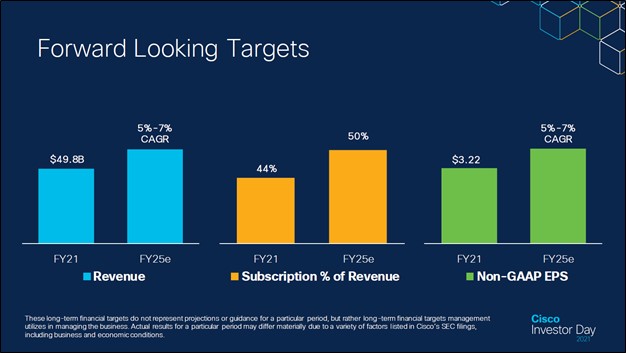

The company’s annual revenue and EPS growth rates are expected to come in at 5%-7% through fiscal 2025, indicating that while Cisco Systems’ growth trajectory is improving, its margins are expected to stay broadly flat during this period. Rising prices for semiconductor components and the need to invest heavily in R&D are part of the reason why, given Cisco Systems retains a large hardware business and operates across several incredibly competitive industries.

Image Shown: Cisco Systems expects its revenues and EPS will steadily grow in lockstep over the coming fiscal years which we appreciate as that speaks favorably towards its future free cash flow growth prospects. Image Source: Cisco Systems – 2021 Investor Day Event Presentation

To generate consistent and sustainable revenue growth, Cisco Systems is targeting several market opportunities supported by secular growth tailwinds while maintaining its position in its core markets. Hybrid work is one market the firm expects to grow at a brisk pace in the coming years, as is cybersecurity, which Cisco Systems can cater to via offerings such as Cisco Duo, Cisco Tetration, and Cisco Umbrella. Optimized application experiences represent another market expected to post strong growth going forward, along with the need to manage vast troves of data and increasingly complicated networking operations.

Image Shown: A look at the various markets Cisco Systems is capitalizing on to support its growth trajectory over the long haul. Image Source: Cisco Systems – 2021 Investor Day Event Presentation

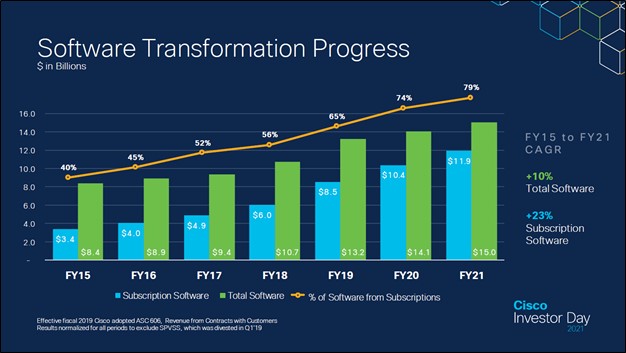

Software sales represent a major way Cisco Systems intends to reboot its growth trajectory. Recurring revenue streams provide for stronger cash flow profiles given the greater visibility of those sales, which is why Cisco Systems is laser-focused on growing its subscription-based software revenues. Over the past several fiscal years, Cisco Systems has had a lot of success on these fronts, though headwinds elsewhere have stymied its ability to improve its company-wide financial performance. The company was still able to generate gobs of free cash flow during this period.

Image Shown: Cisco Systems’ software sales have grown significantly in recent fiscal years which in turn has grown its recurring revenue streams and improved its cash flow profile. Image Source: Cisco Systems – 2021 Investor Day Event Presentation

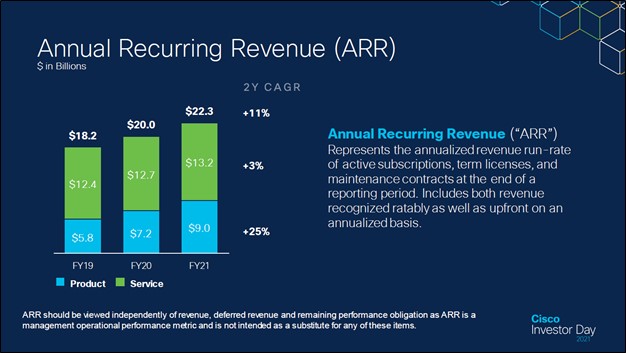

Going forward, Cisco Systems intends to start providing greater clarity on its pivot towards providing software and cloud-based services by highlighting its annual recurring revenue (‘ARR’) performance. Its ARR figure includes maintenance contracts as well, keeping in mind Cisco Systems has a large hardware business.

Image Shown: Cisco Systems intends to highlight its ARR performance going forward. Image Source: Cisco Systems – 2021 Investor Day Event Presentation

Numerous Market Opportunities

Cisco Systems expect its core business opportunities will post a ~5% CAGR through 2025, creating a ~$260 billion total addressable market opportunity (‘TAM’) for the firm to capitalize on. The company expects its revenue will grow at a premium to that due to the upside from what Cisco Systems views as expansion market opportunities, with ‘Expansion Markets’ expected to post ~18% CAGR through 2025 creating a ~$140 billion TAM for the company to capitalize on. Combined, those opportunities underpin Cisco Systems’ medium-term revenue and EPS growth outlook, and in our view, that growth trajectory looks reasonable and achievable. If anything, Cisco Systems is being rather cautious and conservative with its medium-term guidance.

Image Shown: Cisco Systems’ growth trajectory is underpinned by expected growth in the TAM from its core and expansion market opportunities. Image Source: Cisco Systems – 2021 Investor Day Event Presentation

Additional Upside

Beyond its well-identified growth opportunities, Cisco Systems has ample upside in the realm of automation and what the firm views as the future of work. Let’s provide some examples of this upside.

Self-Driving Services

We are now living in a world where self-driving taxi services are no longer a thing of science fiction but could become a readily available transportation option in the not-so-distant future. Over time, the emergence of a widespread self-driving taxi services would create a massive need to manage and optimize that additional data consumption, opportunities that Cisco Systems is well-positioned to capitalize on via its sizable Infrastructure-as-a-Platform (‘IaaS’) business and its hardware offerings that cater to data centers.

We covered how Alphabet Inc’s (GOOG) (GOOGL) Waymo unit is expanding its self-driving pilot program to San Francisco, California, after having success in Arizona in our September 2021 article Update on Best Idea Alphabet’s Self-Driving Taxi Upside (link here) that provides more info on this intriguing topic.

Fully Automated Restaurants

Another source of automation involves restaurants, particularly fast food and quick-service operations. Some examples would be the rollout of in-store kiosks and mobile apps where customers can place orders that show up on a screen inside the relevant restaurant, prompting employees to fulfill those orders. However, we are increasingly moving towards a future where robots may eventually fulfill fast-food and quick-service orders, too. Unlike in an upscale establishment where service may be more appreciated, in fast-food or quick-service operations, whether it is a human or an automated system providing the customer the order, it may not matter much.

Based in Toronto, Canada, the company SJW Robotics aims to showcase a pre-commercial example of its fully autonomous restaurant this fall with the commercial rollout of its offerings beginning in the first quarter of 2022. In Boston, Massachusetts, the Spyce restaurant is largely automated (particularly on the kitchen side of things) though it still has some in-store human employees to assist its customers. There are also plenty of examples of restaurants utilizing some level of in-store automation beyond self-ordering operations, such as White Castle’s partnership with Miso Robotics that involves the former using the latter’s Flippy kitchen automation offerings. As the business world contends with headwinds from labor shortages, having some level of kitchen automation makes meeting customer demand a more manageable endeavor.

Though we are still in the early stages, it is not unreasonable to assume that sometime in the future fully autonomous fast-food and quick-service restaurants will become a larger part of this side of the restaurant business. Neighborhood and fancy restaurants will still exist, of course, but when the goal is getting cheap food quickly, robots will increasingly play a role here. For Cisco Systems, this matters because growth in data consumption and utilizing from the rise of automation creates a massive growth opportunity for its business.

Call Centers and Customer Service Operations

There is room for many other tasks to get automated. One final example we will highlight here is call centers and customer service operations, with an eye towards Nvidia Corporation’s (NVDA) newer Jarvis offering. This offering is billed as “an application framework for multimodal conversational AI services that delivers real-time performance on GPUs. The Jarvis framework includes pre-trained conversational AI models, tools in the NVIDIA AI Toolkit, and optimized end-to-end services for speech and natural language understanding (‘NLU’) tasks” and we are intrigued by the potential here.

Beyond automation and collaboration services, the future of work is creating all sorts of growth opportunities for Cisco Systems. For instance, there is a growing need for end-to-end cybersecurity operations to prevent malevolent cyber actors from accessing private data and potentially shutting down key operations. Managing workloads, applications, and data flows across hybrid and cloud computing networks as an increasing number of employees work from home is another major growth opportunity. Cisco Systems has ample avenues for upside beyond the markets that management had identified as being core or expansion opportunities, which is why we view the firm’s medium-term revenue and EPS guidance as being rather conservative.

Concluding Thoughts

We are big fans of Cisco Systems and view its capital appreciation and dividend growth upside quite favorably, which is why we include shares of CSCO as an idea in both the Best Ideas Newsletter and Dividend Growth Newsletter portfolios. One of the biggest things holding Cisco Systems back over the past few years has been its inability to consistently grow its revenues, which again is partially due to headwinds created by the COVID-19 pandemic. Should the firm regain the ability to post steady revenue and earnings growth, that would favorably impact Cisco Systems’ free cash flow growth outlook in a very meaningful way.

For fiscal 2022, Cisco Systems aims to grow both its revenues and non-GAAP adjusted EPS by 5%-7%, in-line with its medium-term growth targets. Shares of CSCO are up ~27% year-to-date as of this writing, before taking dividend considerations into account, outpacing the ~17% increase seen in the S&P 500 (SPY) during this period.

The company is facing headwinds from inflationary pressures and component shortages (particularly for semiconductors), as we covered in our August 2021 article Cisco Systems Continues to Recover; Growth Outlook Quite Promising (link here). Recently enacted pricing increases should help Cisco Systems navigate these headwinds in the near term, and eventually, these hurdles should dissipate as the global economy slowly returns to normal in the wake of widespread COVID-19 vaccine distribution efforts (vaccination rates remain relatively low in emerging and developing economies, though that will steadily change).

As things eventually return to normal worldwide while Cisco Systems continues to push deeper into markets supported by secular tailwinds, we expect investors will continue warming up to the name and its improving growth outlook.

Downloads

Cisco’s 16-page Stock Report (pdf) >>

Cisco’s Dividend Report (pdf) >>

—–

Technology Giants Industry – FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI

Tickerized for CSCO, INFN, CIEN, FSLY, ANET, FFIV, COMM, LITE, AVYA, IIVI, JNPR, PLT, ZBRA, GLW, TRMB, ZM, PANW, PLTR, CRWD, OKTA, ZS, FEYE, FTNT, PFPT, SPLK, GOOG, GOOGL, NVDA, SPY

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Apple Inc (AAPL), Cisco Systems Inc (CSCO), and Microsoft Corporation (MSFT) are all included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares, Facebook Inc (FB), Korn Ferry (KFY), PayPal Holdings Inc (PYPL) and Visa Inc (V) are all included in Valuentum&rsqu