On July 27, Teva Pharmaceuticals (TEVA) reported solid preliminary results for the second quarter of 2015. The firm is growing organically, and its fundamental strengths shone throughout its report. Revenue increased 6% in the period, after excluding the impact of currency headwinds and the sale of US OTC plants in the second quarter of 2014. Non-GAAP operating income grew 16% from the year-ago quarter to $1.6 billion, and non-GAAP earnings per share increased 15% to $1.43 in the period. Cash flow from operations advanced an impressive 41% to $1.5 billion in the second quarter, and free cash flow grew 51% to $1.3 billion in the period. The solid bottom line performance caused management to raise its earnings per share guidance for the full-year 2015 to the range of $5.15-$5.40 from a range of $5.05-$5.35.

Outstanding cash flow generation is a large part of the reason Teva has been able to transform its business through non-organic means. The firm has agreed to buy the generic-drug business of Allergan (AGN), which operates under the name Actavis, for $40.5 billion in cash and stock. The deal will result in Allergan holding a stake in Teva of less than 10% and is expected to close in the first quarter of 2016. The combined entity is expected to have $26 billion in revenue and EBITDA of ~$9.5 billion in 2016, including a contribution of ~$2.7 billion from Allergan Generics. Cost synergies and tax savings of approximately $1.4 billion annually are expected, with over 20% accretion coming in years two and three following the close. Free cash flow is expected to be ~$6.5 billion in 2016 and will continue to increase thereafter. Such strong cash-flow generation will allow Teva to delever its balance sheet and continue to pursue prudent acquisitions (eventually) to further expand its portfolio.

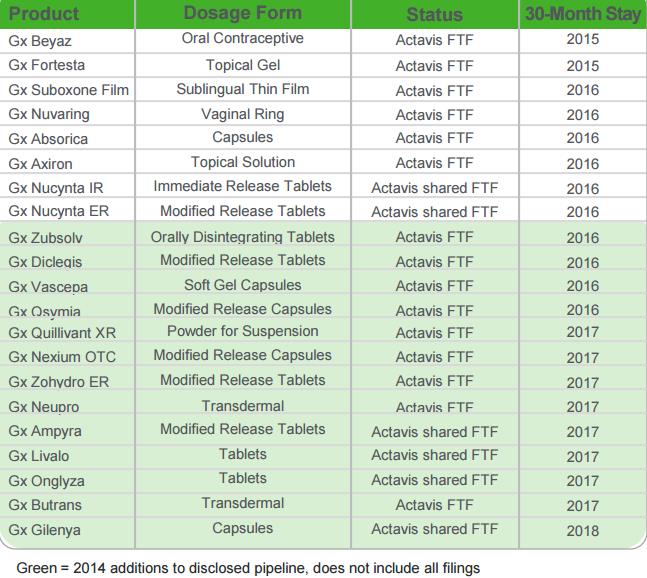

Perhaps the most attractive aspect of the deal for Teva is the strength of Allergan’s generics pipeline and the increased potential for improvement. The acquisition will give Teva the most advanced R&D capabilities in the generics industry, with ~320 combined pending Abbreviated New Drug Applications (ANDAs) in the US, 110 of which are First-to-File (FTF) ANDAs. Allergan is the industry leader in FTF opportunities in the US; the chart below shows select 2014 FTF additions to the company’s disclosed pipeline. The expansion potential is not limited to the US, however. Teva will now have a top three position in over 40 markets worldwide and will have its hand in 100 markets overall.

Image source: Actavis February investor presentation

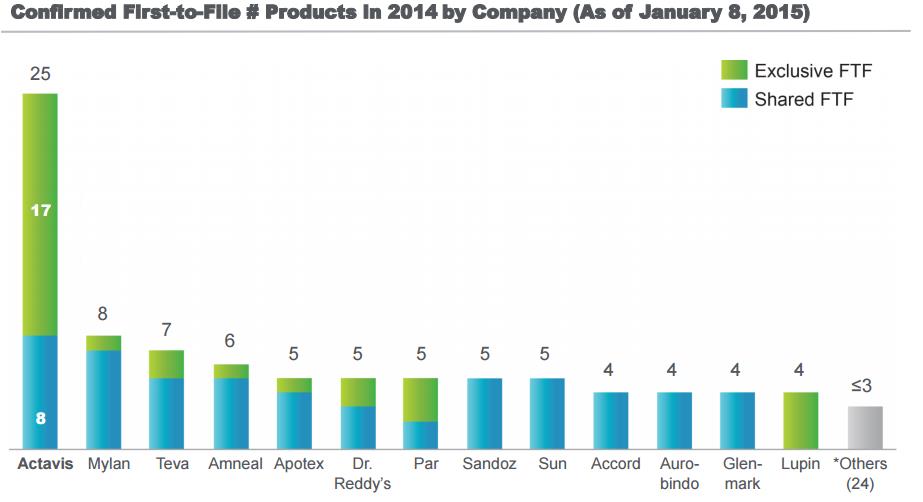

Along with its announcement to acquire Allergan Generics, Teva withdrew its unsolicited expression of interest in Mylan (MYL), which it was preparing to takeover. We were high on the potential of a deal with uncooperative Mylan, and Allegan Generics’ FTF presence in the US in much greater than Mylan’s, as is depicted in both the charts above and below. It’s safe to say we like this deal for Teva. After the dust settles, Teva will remain our favorite idea in the generics space. The company has been a tremendous performer lately, and we will continue to let this winner run as a holding in the Best Ideas Newsletter Portfolio.

Image source: Actavis February investor presentation