Key Takeaways

· Valuentum sees four major brand segments

o Ultra-Luxury

§ Richemont, Burberry, LVMH, Gucci (Kering), Chanel, Hermes

§ Rich heritage brands, economically resilient consumer

o Luxury

§ Marc Jacobs, Tory Burch, Ralph Lauren, Tiffany

§ Valuable brands, semi-strong barriers to entry

o Aspirational

§ Michael Kors, Marc by Marc Jacobs, Coach, North Face

§ Popular with younger consumers, strong brand loyalty

o Established

§ Nike, Adidas, Under Armour, lululemon, PVH, Express

§ Price competitive, exposed to fashion

· Our favorite dividend idea: Coach

· Fallen Stars: Guess, Bebe

· Valuentum’s Take: Brand value is only part of the investment equation

Branding has been a powerful force in both marketing and investing for the past century. Companies work hard to establish a story and invoke an emotional reaction from consumers. Of course, these emotional reactions can be produced by a variety of means depending on the individual consumer. These brands may cater to value seekers, those desiring luxury, or those wanting the most fashionable product. The brands enable connections that develop loyalty and repeat purchases no matter the consumer.

Let’s take a journey inside various sectors of retail and analyze the structure of what we view as the most important category segments: Ultra-Luxury, Luxury, Aspirational, and Established Brands. Our investigation will focus mainly on soft goods, including cosmetics, clothing, jewelry, and handbags.

Ultra-Luxury

Image Source: Piaget

Ultra luxury firms stand alone at the high-end of the retail space. Many of these companies sell products that may cost more than the average American makes in a year, and therefore, sales tend to hold up relatively well in spite of broader macroeconomic conditions. The traditional ultra-luxury buyer won’t “feel” a 3% decline in housing prices or even a 10% pullback in equity prices. With the exception of an economic or financial market catastrophe, this market is resilient.

Barriers to entry seem very low on the surface. Theoretically, Valuentum could hire a designer and employees, and strike up a distribution deal to sell Valuentum Handbags for $15,000. Would anyone buy them? Probably not. It can take years, if not decades, to cultivate an exclusive brand value that justifies a premium price tag. Richemont, for instance, owns luxury brands such as Cartier that have a reputation that has been established over centuries. Barriers to entry are strong, in our view.

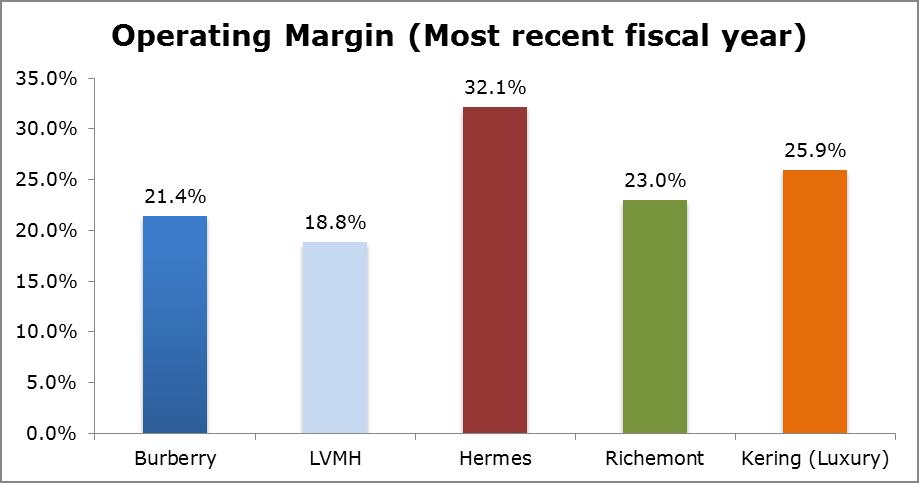

Because ultra-luxury buyers are the wealthiest consumers in the world, companies maintain good pricing power. Burberry, for instance, can raise prices on its signature scarf every year without demand waning. These companies also don’t have to worry about competitors eroding the industry price structure because lowering prices could eventually damage brand value. We can see this story in the operating margins of competitors (shown above).

Recently, some ultra-luxury brands have shifted attention away from conspicuous luxury as buyers become more conscious of displays of affluence. Brands such as Burberry, Hermes and those under the Richemont umbrella have always focused on craftsmanship and elegance rather than displaying brand names to drive sales, so these firms have performed exceptionally well.

Image Source: Hermes

On the other hand, firms like Louis Vuitton Moet Hennessey (LVMH), Dolce & Gabanna, and Kering-owned Gucci have focused on making their brands visible on their products, particularly in the leather bags space. Luckily, most ultra-luxury brand owners have multiple product lines (Gucci has shoes, bags, clothes, and jewelry) or brands (LVMH owns Louis Vuitton, Dior, Fendi, and Celine), so sales of less conspicuous products can compensate for weakness elsewhere.

Although the style may be toned down, at the end of the day, many consumers still purchase ultra-luxury goods as a display of wealth. A handbag from Hermes (shown above) still carries plenty of branding based on color, silhouette, and materials that are identifiable by other luxury consumers.

Cosmetics, unlike a bag or a purse, don’t carry wearable branding. However, firms are able to differentiate on quality and performance. LVMH-owned Sephora sells LVMH-owned Yves Saint Laurent cosmetics at a high price with competition from the privately-held Chanel in makeup as well as Hermes in fragrances.

While luxury consumption becomes more conspicuous, the chance of a blowback against luxury consumption remains a risk to industry profitability. American consumers, in our view, may be more interested in shifting consumption from material goods to experiences (think travel, restaurants, etc.). We think this could set a tone across the globe that consumers can get more value from life experiences than they can from luxury consumption. Still, we have yet to see this trend hit the growing base of Chinese and Indian luxury consumers. Plus, ultra-luxury consumers already have so much wealth that they probably do not need to choose between different purchases, making conspicuous consumption more of a risk to luxury brands than ultra-luxury brands.

With classic style, incredible brand value, and a customer base that is dominated by the richest people on earth, the ultra-luxury space can reward investors with wonderful economic profits.

Luxury

Don’t get us wrong, the luxury market isn’t necessarily a lower quality area or not as popular, but it simply caters to a wider audience. Price points at luxury brands like Tiffany and Ralph Lauren are not inexpensive, but price points are undoubtedly lower than at the highest end of the market.

The average luxury consumer does not possess the same level of wealth as ultra-luxury consumers, though this consumer is no slouch. Unlike the ultra-high-end, luxury brands depend on branding as much as superior craftsmanship. Tiffany, for instance, is known for its iconic “little blue box,” while Ralph Lauren boosts its legendary Polo player logo.

The Iconic Polo Horse

Image Source: Ralph Lauren

Though prices are lower, make no doubt about it, barriers to entry in the segment are relatively strong. Occasionally, a smaller brand like Tory Burch will rapidly gain market share and popularity, but it still takes years (3-5 in the case of Burch) to generate credibility to reach the broader marketplace.

LVMH is exposed to this market via Marc Jacobs, which also has an aspirational level brand in Marc by Marc Jacobs.

Because price points are more affordable, luxury competitors are often tempted to leverage the existing brand integrity to open distribution and move down market. Some brands can successfully accomplish this goal by differentiating between the brands, while others have cheapened themselves to the point where they are relegated to aspirational status. Tiffany recently encountered this problem and opted to focus on its high-end products to avoid diluting its brand value.

Therefore, brands have the ability to charge premium prices but must be careful to strike a balance between being too expensive and cheapening the brand. If gross margins decline over a long timeframe, then there is a good possibility management is “down marketing” the brand. Guess provides a recent cautionary tale that we will examine further in our “Fallen Stars” segment.

Ultimately, luxury companies have a larger potential footprint than ultra-luxury brands, but industry participants must continually work to justify premium price points and must avoid diluting brand value in search of revenue growth. The luxury industry can be a wonderful place for companies to earn economic profits, but we think the sector carries more fashion and brand value risk than the ultra-luxury space.

Luxury Market Size and Potential

In 2012, the total value of the global luxury market was approximately 212 billion euros ($287 billion USD), and projections peg sales to exceed 250 billion euros ($339 billion USD) by 2015. This robust growth bodes well for every participant.

The bulk of sales growth will come from China, which we believe will significantly outpace the rest of the luxury market in terms of sales growth going forward. This doesn’t necessarily require a luxury maker to have an enormous bricks-and-mortar footprint in mainland China—many shoppers will purchase luxury goods while traveling abroad. Still, luxury brands must cater particularly to high-end Chinese buyers to win a share of luxury spending growth.

When it comes to catering to Chinese consumers, we think Richemont, Tiffany, Louis Vuitton, and Hermes do it best as all have significant footprints in major tourist destinations such as New York City, London, Paris, and Dubai, while also pushing product through plenty of doors domestically. We think consumption could shift in favor of domestic growth in China as the government lowers tariffs in order to capture sales tax revenue. The country recently signed a free trade agreement with Switzerland to lower the cost of Swiss watches, and it could be the first of many initiatives to make domestic consumption more attractive relative to foreign purchases.

As far as goods are concerned, watches and jewelry remain tremendous growth opportunities flanked by growth in leather goods (think handbags) and shoes. Bain estimates each of these segments within the luxury market, as well as men’s apparel, grew at a double-digit rate in 2012. If growth can be similarly strong going forward—even a low-double-digit growth rate—industry participants will have the wind at their backs.

Aspirational

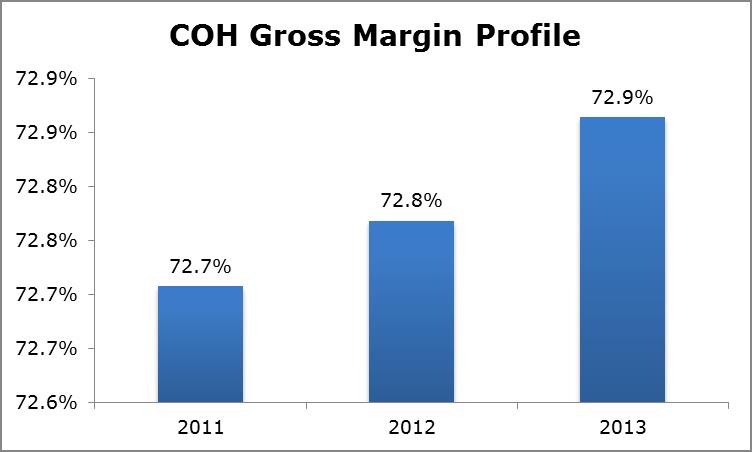

Often confused and sometimes interchangeable with luxury depending on who defines luxury, aspirational brands sit a tier below traditional luxury brands, but still inspire brand loyalty and value. A perfect example of an aspirational brand is Coach. While consumers won’t pay Louis Vuitton prices for its products, Coach still commands a nice premium that allows the firm to earn a healthy gross margin.

Image Source: Company Filings, Valuentum

In fact, because Coach is able to utilize lower-cost production standards, it is able to earn gross margins that are even stronger than those of most luxury and ultra-luxury brands. We’ve seen that sentiment echoed from aspirational peer, Michael Kors. Interestingly enough, Michael Kors has stolen share from Coach during the past few years, and the situation highlights the relatively low barriers to entry in the aspirational space. Though it may have taken the likes of Tiffany, Richemont, and Louis Vuitton years to ramp up sales, Michael Kors&