Intermodal freight lessor TAL International () posted modest third quarter results, as the market for global shipping remains weak. Revenue increased 6.4% year-over-year to $143.9 million, short of consensus expectations, while adjusted net income per share fell short of consensus estimates at $1.03 (up 8.4% year-over-year). Adjusted EBITDA grew only 1.3% year-over-year to $142.8 million. Still, TAL increased its quarterly dividend to $0.70 per share, an increase of 2.9%.

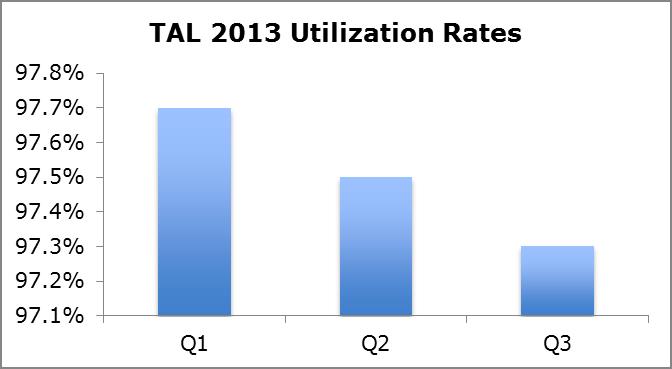

Utilization: Strong But Declining

Image Source: Company Filings, Valuentum

In spite of what TAL identified as a relatively weak market, utilization rates were above 97% compared to the industry average of the low-to mid-90% range. However, management noted that current utilization rates are hovering at 96.9%, which means that rates are on track to decline in every quarter of 2013 (on a sequential basis). This trend certainly doesn’t bode well for a highly-leveraged company that cites high utilization rates as a competitive advantage.

Top-line expansion of just 6.4% is obviously a tad disappointing for some shareholders, but we like management’s decision to remain disciplined during an environment deemed unattractive for investment. We admire what CEO Brian Sondey said on the conference call, noting:

“…no doubt, there is a tension between growth ambitions and returns. And I think in general we’ve said for many years that, and I’m just throwing these numbers out for examples, we’d rather be a company that grows at 10% and has a return on equity of 20% than be the opposite, a company that grows a 20% and has returns of 10%. And I think that remains our philosophy.”

The strategy of growth for growth’s sake can often come at a great expense for shareholders. Although it may cause frustration in the near term, we think TAL is much better off in the long run with its prevailing policy.

Outlook

TAL provided some insight into the fourth quarter of 2013 and 2014. The company believes pre-tax income will decline slightly sequentially. Yet, after three straight years of disappointing trade growth, management appears confident trade activity will accelerate in 2014; if it does, the firm is well positioned to benefit.

Valuentum’s Take

Overall, we thought TAL’s third quarter results were just okay. The firm boasts a hefty dividend yield, but shares of the company look fairly valued. We aren’t interested in adding them to either of our actively managed portfolios.