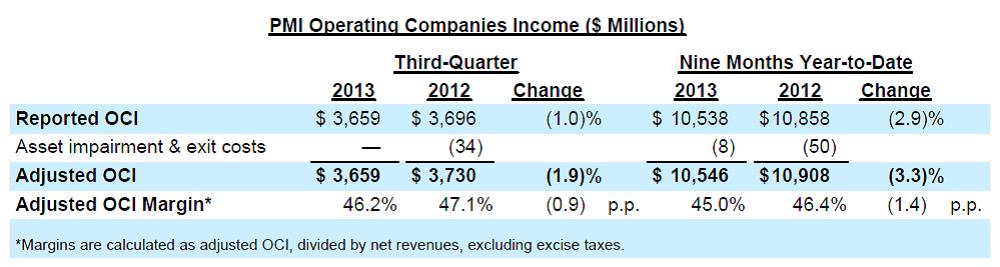

On Thursday, Philip Morris International (PM) reported third-quarter results that showed the continuation of a very challenging cigarette volume environment. Reported net revenues held the line thanks to significant pricing strength, but adjusted ‘operating companies income’ (OCI) still fell 1.9% (shown below). We’re growing skeptical of the firm’s ability to control costs, as there should have been better performance on the operating line given that pricing completely replaced volume losses in the period (price falls straight to the bottom line). Profit margin improvement was surprisingly absent, with the company’s adjusted OCI margin falling 0.9 percentage points from the year-ago period.

Image Source: Philip Morris

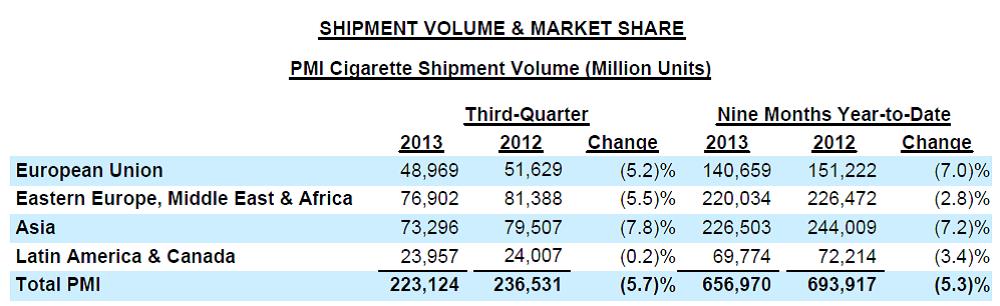

Adjusted diluted earnings per share of $1.44 was 4.3% higher than the same period a year ago, but it was bolstered by the firm’s share repurchase program (a low-quality improvement). We don’t expect to make any changes to our fair value estimate, but we’d like to see better ‘operating companies income’ performance given pricing strength, as volume declines show no signs of letting up. The pace of the decline in total cigarette shipment volume actually accelerated in the third quarter relative to the year-to-date pace. The performance is not pretty (shown below).

Image Source: Philip Morris

Valuentum’s Take

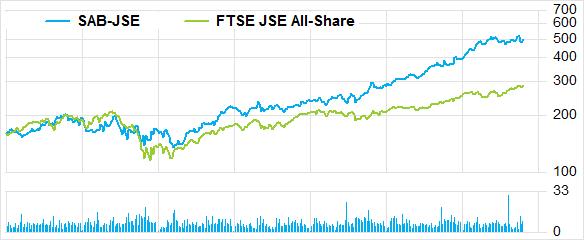

Philip Morris’ third-quarter results left much to be desired. We continue to prefer domestic peer Altria (MO), as its annual dividend yield of 5.4% is not only better than Philip Morris International’s 4.3% mark (at the time of this writing), but the former continues to raise it at a nice clip and holds a prized 27% ownership stake in SABMiller, which continues to perform well. SABMiller currently sports an R800 billion market capitalization (or about $80 billion USD at current exchange rates), which means Altria is effectively sitting on $21.6 billion in potential cash (about 30% of its market capitalization)* at current price levels. We think this hidden asset within Altria’s portfolio is the primary difference between our fair value of Altria and its market price. Altria remains a core holding in the portfolio of our Dividend Growth Newsletter.

SABMiller Recent Equity Performance (SAB-JSE) – in South African Rand

Image Source: FactSet

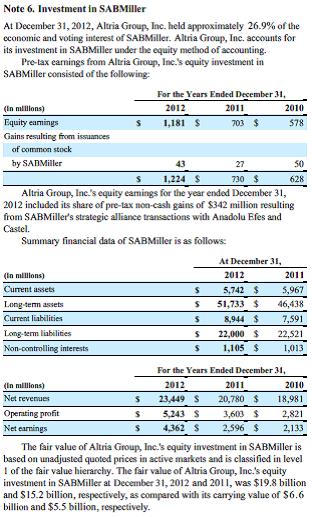

(*) Altria’s Investment in SABMiller, excerpt from page 53 of annual report.

{kind=link}

Image Source: Altria