Image Source: Valuentum

By Brian Nelson, CFA

We’re huge fans of the environmental services industry. Solid waste simply must be disposed of somewhere in good times or bad times, and garbage haulers operate within an attractive oligopoly when it comes to disposal capacity (i.e. transfer stations, disposal facilities). Many players offer attractive dividend yields to boot. We include Republic Services (RSG) as an idea in our simulated newsletter portfolios, but Waste Management (WM) is yet another consideration.

On December 8, Waste Management announced that its board gave the thumbs up for a 7.7% increase in its quarterly payout for 2023, to $0.70 per share. The hike to $2.80 per share on an annual basis implies a forward estimated dividend yield of ~1.6% at the time of this writing and amounts to the 20th consecutive year of dividend increases at the environmental services giant. Waste Management runs a largely predictable business due to its collection operations, and the company has authorized another $1.5 billion to buy back stock.

Image Source: Waste Management

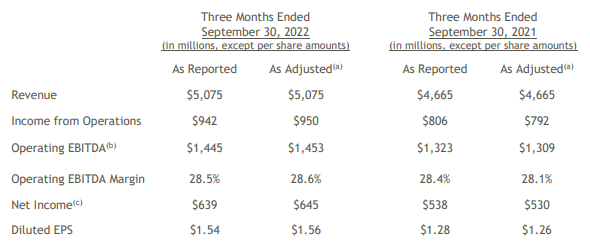

When Waste Management reported third-quarter results for the period ending September 30 in late October, the company showed robust top-line growth thanks to strong collection and disposal yield expansion of 7.1%. During the period, collection and disposal volumes advanced 1.4%, and better cost controls and a focus on automation helped to drive an 11% advance in adjusted operating EBITDA. Management noted in the press release that “pricing and operating efficiencies worked to overcome inflationary cost pressures,” as the firm continues to reduce overhead costs amid volatile market prices for recycled commodities. Operating EBITDA across its recycling operations fell by $36 million on a year-over-year basis.

Many market observers were concerned by Waste Management’s free cash flow performance in its third quarter as core capital spending (which excludes sustainability investments) swelled to $547 million compared to $448 million in the year-ago period. Though cash flow from operations was about in-line with last year’s quarter, the higher investment drove traditional free cash flow, which includes all capital spending, to $432 million compared to $773 million during the same period in 2021. Expenditures for sustainability growth investments were $210 million in the quarter, and the executive team has a sustainability program where it will shell out $1.625 billion to expand renewable energy and its recycling operations from 2022-2025.

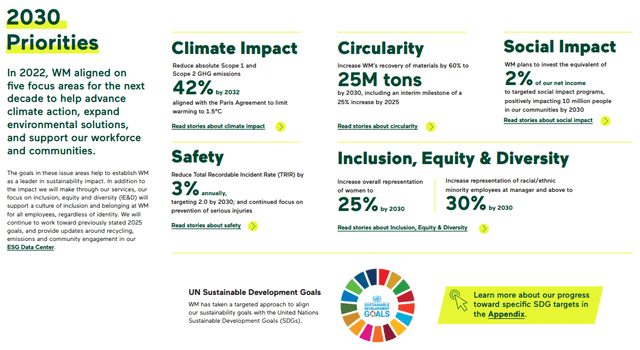

Image Source: Waste Management’s 2022 Sustainability Report

Waste Management is in an important position to make a positive impact on the environment because of the nature of its operations (i.e. renewable energy, recycling, and the like). According to Chief Sustainability Officer Tara Hemmer, “by 2026, (it) expect(s) to see six-fold growth in the amount of renewal natural gas (RNG) produced at WM-operated landfills, along with 25% growth in the tons of materials that (it) divert(s) for reuse.” CEO Jim Fish’s CEO message noted that the firm is working hard “to minimize (its) environmental impact by reducing carbon emissions across the value chain, investing in technology and automation,” and that Waste Management has launched “three new Impact Groups to connect and uplift multicultural, female, and LGBTQ+ employees.”

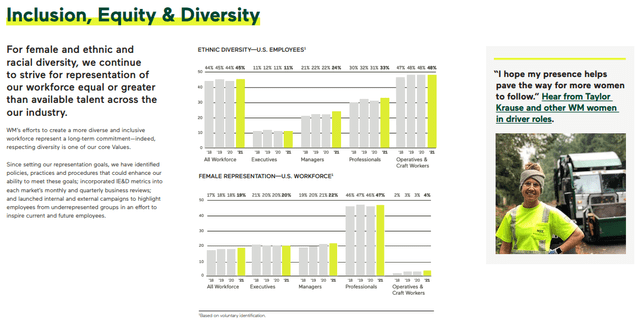

Image Source: Waste Management

Concluding Thoughts

2023 will mark the 20th consecutive year that Waste Management has increased its dividend payout. Though free cash flow is facing pressure due to its sustainability growth initiatives that are driving total capital expenditures higher, the company’s valuable disposal capacity and pricing power across its municipal solid waste operations are a couple qualities that we like. Shares are trading about in line with our fair value estimate at the moment, as they boast a ~1.6% forward estimated annual dividend yield.

Tickerized for RSG, WM, WCN, CWST, SRCL, EVX, USMV, CLH, CVA, DAR, VEOEY, SZEVY, ENGIY

———————————————

About Our Name

But how, you will ask, does one decide what [stocks are] “attractive”? Most analysts feel they must choose between two approaches customarily thought to be in opposition: “value” and “growth,”…We view that as fuzzy thinking…Growth is always a component of value [and] the very term “value investing” is redundant.

— Warren Buffett, Berkshire Hathaway annual report, 1992

At Valuentum, we take Buffett’s thoughts one step further. We think the best opportunities arise from an understanding of a variety of investing disciplines in order to identify the most attractive stocks at any given time. Valuentum therefore analyzes each stock across a wide spectrum of philosophies, from deep value through momentum investing. And a combination of the two approaches found on each side of the spectrum (value/momentum) in a name couldn’t be more representative of what our analysts do here; hence, we’re called Valuentum.

———————————————

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, RSP. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.