|

|

Recent Articles

-

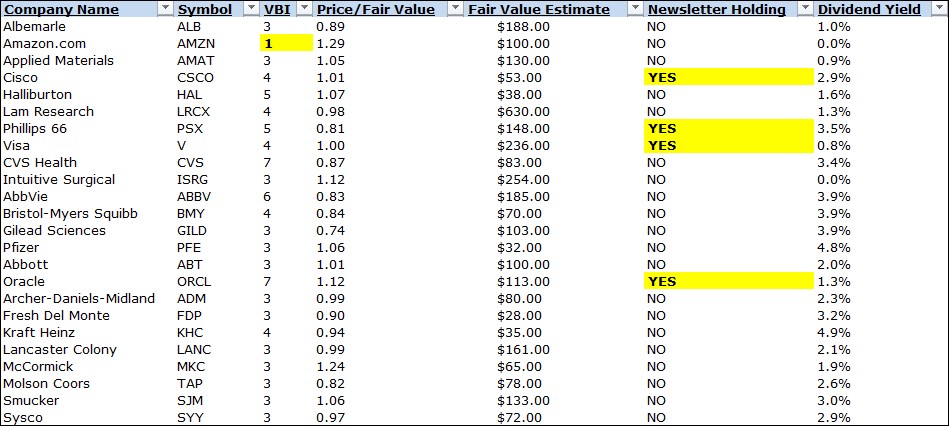

Report Updates: Amazon Registers the Lowest Rating on Our Scale

Report Updates: Amazon Registers the Lowest Rating on Our Scale

Sep 24, 2023

-

Check out the latest report updates on the website. The biggest takeaway of this refresh is that Amazon is poised to generate significantly negative free cash flow in 2023, and while we think the firm will turn this measure around materially in the long haul, shares are coming out as overvalued on our discounted cash-flow process, while technically its stock price is breaking down. An overvalued stock on both an absolute and relative value basis with negative technical/momentum indicators registers the worst rating on our methodology, the Valuentum Buying Index (1=worst, 10-best).

-

Dividend Increases/Decreases for the Week of September 22

Sep 22, 2023

-

Let's take a look at firms raising/lowering their dividends this week.

-

Cisco Buys Splunk

Sep 21, 2023

-

Image Source: Brandon Leon.

Dividend Growth Newsletter portfolio holding Cisco is all about growing its recurring revenue base these days, and its announcement that it will buy Splunk on September 21 will not only help in a big way towards that goal, but the deal will also position Cisco for tremendous opportunities in the booming market that has become artificial intelligence [AI]. That said, some investors were not fans of the purchase price – some $28 billion in cash – but we think the price is fair and strategically, there’s nothing wrong with adding to the fold an asset-light, recurring-revenue business that has the foundation to be a key long-term player in AI. We’ll be taking a close look at our valuation model on Cisco as we further digest this proposed transaction, but for now, we’re comfortable with our $53 per-share fair value estimate of the networking giant.

-

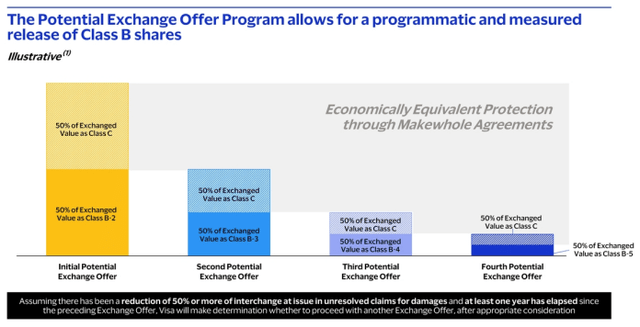

Details Regarding Visa’s Exchange Offer

Sep 21, 2023

-

Image: Visa's 8-K.

Visa remains a free-cash-flow generating powerhouse, and the firm’s operating and free cash flow margins are about as good as it gets. Future potential exchange offers from Visa corresponding to its various share classes should be viewed as a minor intermediate-term inconvenience that will only provide but a modest potential headwind to the advancement of the company’s intrinsic value over time, and only in the scenario where diluted shares outstanding increase relative to expectations based on then-conversion rates for non-A class shares when converted. We continue to like Visa as a holding in the simulated Best Ideas Newsletter portfolio, and we like it and Mastercard more than their rivals such as American Express and Discover Financial that take on credit risk.

|