|

|

Recent Articles

-

AT&T: A High Yield Dividend Disaster, Now An ESG Nightmare

AT&T: A High Yield Dividend Disaster, Now An ESG Nightmare

Jul 24, 2023

-

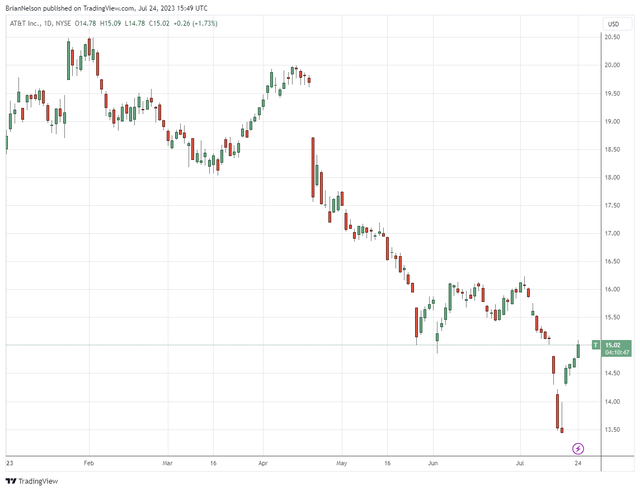

Image: AT&T’s shares continue to disappoint.

We’re not interested in AT&T at all and believe that shares may remain under significant pressure until 1) material top-line growth resumes, 2) the firm’s capital-intensity lessens, 3) free cash flow improves significantly, 4) dividend increases resume 5) its leverage improves and 6) there is more visibility related to the potential contingent liabilities associated with lead-covered cables. We doubt all six of these things will happen, and therefore we believe the best days are likely behind AT&T.

-

Philip Morris’ Cash-Flow Dividend Coverage Resilient, ZYN Performance Impressive

Jul 24, 2023

-

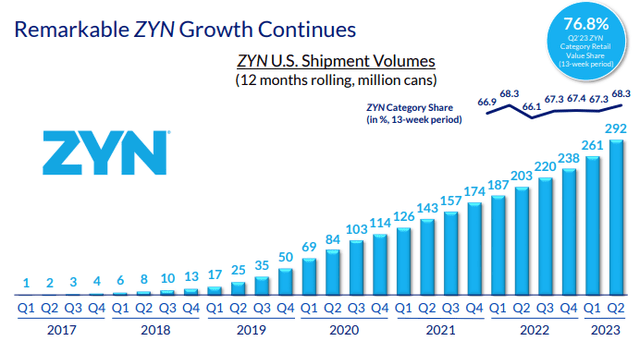

Image Source: Philip Morris.

Our fair value estimate for Philip Morris stands at $105 per share, and we don’t expect to make any material changes to our valuation of the company following the quarterly report. Philip Morris’ combustible tobacco revenue continues to be strengthened by pricing power, while its smoke-free momentum, particularly with ZYN, continues. Though adjusted financial measures continue to look good at Philip Morris, more and more we’re paying closer attention to reported diluted earnings per share, which will face material pressure in 2023 ($5.36-$5.45 per share) compared to $5.81 per share in 2022. The company’s free cash flow remains robust, but its total debt levels are not ideal, in our view. Philip Morris is trading just shy of $100 with a dividend yield of ~5.2% at the time of this writing.

-

Dividend Increases/Decreases for the Week of July 21

Dividend Increases/Decreases for the Week of July 21

Jul 21, 2023

-

Let's take a look at firms raising/lowering their dividends this week.

-

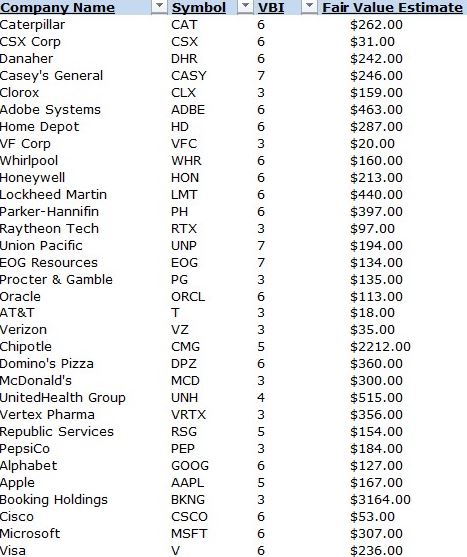

Stock Report Updates

Jul 20, 2023

-

Check out the latest report updates on the website.

|