|

|

Recent Articles

-

Public Storage’s Core FFO Comfortably Covers Its Dividend

Public Storage’s Core FFO Comfortably Covers Its Dividend

Nov 4, 2024

-

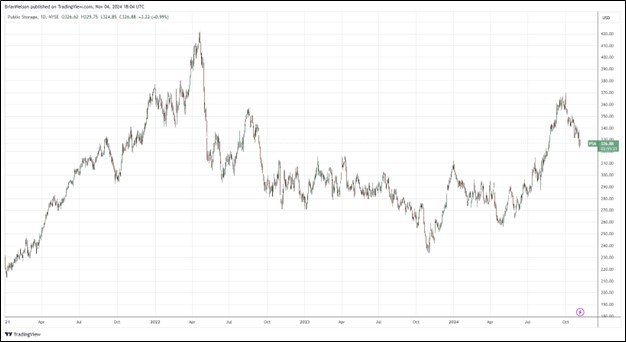

Image: Public Storage is bouncing off lows hit in late 2023.

Public Storage’s core FFO allocable to common shareholders in the quarter came in at $4.20, down 3% on a year-over-year basis, but in excess of its regular common quarterly dividend of $3.00. Looking to 2024, management is targeting revenue to fall 0.5%-1.3%, with expense growth in the range of 2%-3.5%, and net operating income to fall 1.3%-2.7%. Non-same store operating income is targeted in the range of $480-$495 million, while core FFO per share for 2024 is expected in the range of $16.50-$16.85, down 0.2%-2.3% from last year but comfortably above the $12.00 annual dividend per share run rate. Shares yield 3.7% at the time of this writing.

-

Berkshire Hathaway’s Operating Earnings, Free Cash Flow Fall in Third Quarter

Nov 4, 2024

-

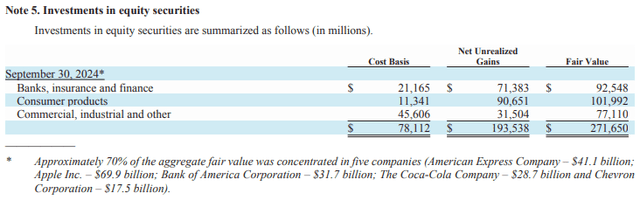

Image: Berkshire Hathaway has reduced its stake in Apple and Bank of America.

Berkshire’s third quarter operating results weren’t great, and the firm noted that it expects pre-tax incurred losses from Hurricane Milton to be between $1.3-$1.5 billion and be reflected in its fourth quarter earnings. Free cash flow has faced some pressure during the first nine months of the year, and Buffett continues to cash out of Apple and Bank of America. Berkshire’s cash balance continues to swell, perhaps indicating that Buffett views the market as overheated at the moment. Total shareholders’ equity was $631.8 billion at the end of September, translating into a price-to-book ratio of 1.54. Shares of Berkshire are not cheap, in our view, but the company remains a key holding in the Best Ideas Newsletter portfolio.

-

Amazon’s Operating Profit Surprises to the Upside

Nov 4, 2024

-

Image: Amazon’s shares have done quite well since the beginning of 2023.

Looking to the fourth quarter of 2024, Amazon's net sales are expected to be between $181.5 billion and $188.5 billion, growing 7%-11% compared with the fourth quarter of 2023 and the midpoint slightly below consensus of $186.4 billion. The top line guidance assumes an unfavorable impact of roughly 10 basis points from currency fluctuations. Operating income in the quarter is targeted in the range of $16-$20 billion, compared with $13.2 billion in the fourth quarter of 2023 and the midpoint above consensus of $17.5 billion. Amazon ended the quarter with $88 billion in cash and marketable securities and $54.9 billion in long-term debt.

-

Meta Platforms Expects Significant Capex Growth in 2025

Nov 4, 2024

-

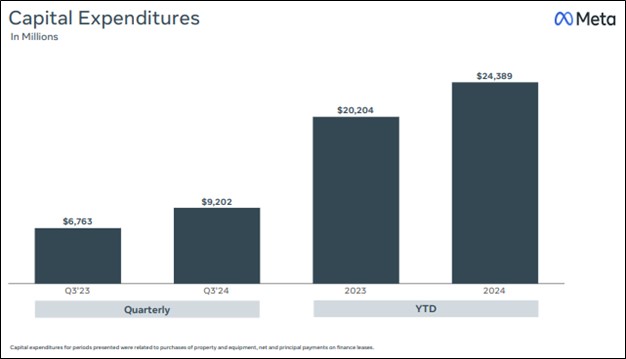

Image: Meta’s capital spending continues to be on the rise, but its free cash flow generation remains robust.

Meta Platforms put up excellent third quarter results with strong free cash flow generation. The company’s balance sheet also remains very healthy with a substantial net cash position. However, management spoke of continued capital spending growth, which will weigh on free cash flow generation in the coming periods. The company also noted cost pressures in depreciation and operating expense growth for next year, putting a damper on the excitement surrounding its third-quarter earnings beat. Though cost pressures should be expected, Meta Platforms remains a net-cash-rich, free-cash-flow generating powerhouse.

|