|

|

Recent Articles

-

Johnson & Johnson’s Pending Split-Up, Talc Liabilities, New CEO Add Complexity to a Once-Clean Dividend Growth Story

Johnson & Johnson’s Pending Split-Up, Talc Liabilities, New CEO Add Complexity to a Once-Clean Dividend Growth Story

Jan 25, 2022

-

Image Shown: J&J continues to face legal liabilities due to talcum powder lawsuits. Image Source: Mike Mozart.

We prefer simple dividend growth stories. Unfortunately, J&J is no longer one of them. A split of Johnson & Johnson’s consumer products division from its medical device and pharma divisions in the next 18-24 months means that dividend growth investors will have added complexity as a new CEO takes the helm, all the while the board manages its growing talc liabilities during a global pandemic. Shares of J&J haven’t been as strong a performer as other stocks on the market the past five years, but we still like its firm foundation and nice combination of dividend yield and potential dividend growth for now. That may change in the coming months to years, however.

-

Netflix’s Subscriber Growth Is Slowing Down, Competition Heating Up

Jan 23, 2022

-

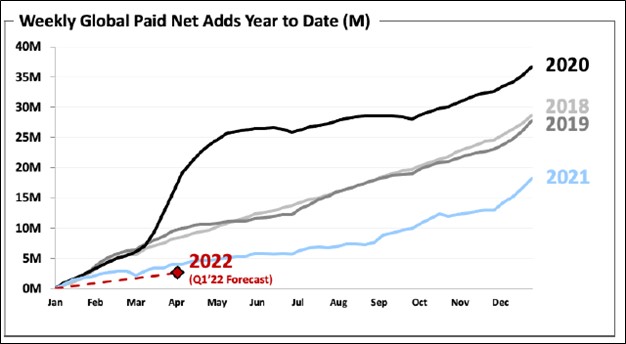

Image Shown: Netflix Inc’s paid subscriber base is expected to grow at a slower pace in the near term compared to the performance seen in recent years. Image Source: Netflix Inc – Shareholder letter covering the fourth quarter of 2021.

On January 20, Netflix reported fourth-quarter 2021 earnings after the bell. The video streaming giant met consensus top-line estimates and beat consensus bottom-line estimates last quarter as original content such as the South Korean TV show Squid Game (released September 2021) proved to be quite popular in markets around the globe and helped Netflix retain interest in its service. During Netflix’s latest earnings call, management noted that the violent Squid Game TV show had been renewed for a second season when asked by an analyst about the issue. However, the near-term guidance Netflix provided in conjunction with its latest earnings update signaled that growth in its paid subscriber base was expected to slow down in the first quarter of 2022 on both a year-over-year and sequential basis. During regular trading hours on January 21, shares of NFLX were pummeled.

-

RH’s Financials, Long-Term Potential Great But Housing Market and Deteriorating Wealth Effect Pose Risks

Jan 23, 2022

-

Image Shown: Shares of RH have exploded higher since the news broke that Berkshire Hathaway Inc had taken a stake in the firm’s equity back in 2019, though shares of RH have shifted lower in recent months.

RH is an innovative home furnishing company that pairs its products with interior/exterior design services to offer a comprehensive package. The company primarily targets affluent households in the U.S., Canada, and the U.K. RH has tremendous pricing power and its margins have increased significantly in recent fiscal years, even during the COVID-19 pandemic, and its net revenues are trending higher as well. The firm is expanding into the high-end hospitality industry and has several projects that are set to come online in 2022 and beyond. RH is a stellar free cash flow generator with a manageable net debt load. Though the company has been executing nicely of late, as witnessed by its stellar financial performance and recent guidance increases, shares of RH have sold off in recent months. In our view, the recent selloff is a function of broad based market weakness, but it also may be due to investors growing more concerned about the impact higher interest rates and a deteriorating wealth effect may have on housing and home furnishing demand and on its push into the hospitality space, respectively. We continue to view RH’s long-term capital appreciation upside potential favorably, however.

-

Don’t Throw the Baby Out with the Bathwater

Don’t Throw the Baby Out with the Bathwater

Jan 22, 2022

-

Image: Erica Nicol.

Junk tech should continue to collapse, but the stylistic area of large cap growth and big cap tech should remain resilient. Moderately elevated levels of inflation coupled with interest rates hovering at all-time lows isn’t a terrible combination. In fact, it’s not bad at all. The markets are digesting the huge gains of the past few years so far in 2022, and the excesses in ARKK funds, crypto, SPACs, and meme stocks are being rid from the system. Our best ideas are “outperforming” the very benchmarks that are outperforming everyone else. The BIN portfolio is down 6.4% and the DGN portfolio is down 3.2% year to date. The SPY is down 7.8%, while the average investor may be doing much worse. Our timing to exit some very speculative ideas in the Exclusive publication has been impeccable. Beware of “best-fitted” backtest data regarding sequence of return risks. Research is to help you navigate the future, not the past. We remain bullish on stocks for the long haul and grow more and more excited as our simulated newsletter portfolios continue to hold up very well. Don’t throw the baby out with the bath water. Stick with the largest, strongest growth names. We still like large cap growth and big cap tech, though we are tactical overweight in the largest energy stocks (e.g. XOM, CVX, XLE). The latest short idea in the Exclusive publication has collapsed aggressively since highlight January 9, and we remain encouraged by the resilience of ideas in the High Yield Dividend Newsletter portfolio and ESG Newsletter portfolio. Our options idea generation remains ongoing.

|