|

|

Recent Articles

-

High-Yielding Income Growth Idea Digital Realty Expects Business Will Continue Recovering

High-Yielding Income Growth Idea Digital Realty Expects Business Will Continue Recovering

Feb 21, 2022

-

Image Shown: We are big fans of Digital Realty Trust Inc’s global footprint. Image Source: Digital Realty Trust Inc – Fourth Quarter of 2021 IR Earnings Presentation.

On February 17, Digital Realty Trust reported fourth quarter 2021 earnings that beat both consensus top- and bottom-line estimates, though its near term guidance came in a tad softer than expected. The data center real estate investment trust (‘REIT’) is facing headwinds from vintage leases rolling off and concerns about surging power costs around the world. On the plus side, Digital Realty is experiencing decent growth at the part of its business where re-leasing terms have been more favorable, and its contracts generally include provisions that allow the REIT to pass on electricity expenses to its tenants. We include Digital Realty as an idea in both the Dividend Growth Newsletter and High Yield Dividend Newsletter portfolios.

-

Dividend Increases/Decreases for the Week February 18

Dividend Increases/Decreases for the Week February 18

Feb 18, 2022

-

Let's take a look at companies that raised/lowered their dividend this week.

-

Cisco Posts Great Earnings Update; Increases Dividend and Share Buyback Authority

Feb 17, 2022

-

Image Shown: Cisco Systems Inc is a very shareholder friendly company. Image Source: Cisco Systems Inc – Second Quarter of Fiscal 2022 IR Earnings Presentation.

On February 16, Cisco Systems reported second quarter earnings for fiscal 2022 (period ended January 29, 2022) that smashed past both consensus top- and bottom-line estimates. Shares of CSCO surged higher initially after its earnings were made public as the company offered up promising near term guidance, indicating that its positive momentum seen of late is expected to continue. We include shares of CSCO as an idea in both the Best Ideas Newsletter and Dividend Growth Newsletter portfolios. Cisco announced a 3% sequential increase in its quarterly dividend in conjunction with its latest earnings update, bringing it up to $0.38 per share or $1.52 per share on an annualized basis. The company also announced it had increased its share repurchasing capacity by $15 billion, bringing its total repurchasing capacity up to ~$18 billion. Shares of CSCO yield ~2.8% as of this writing at its new payout level, and we view its dividend strength as rock-solid due to its pristine balance sheet and stellar free cash flows. Our fair value estimate for Cisco sits at $62 per share with room for upside as the high end of our fair value estimate range sits at $74 per share. That is meaningfully above where shares of CSCO are trading at as of this writing (~$56 per share each), and we view the company’s capital appreciation upside potential quite favorably.

-

The Castle Trumps the Moat

Feb 16, 2022

-

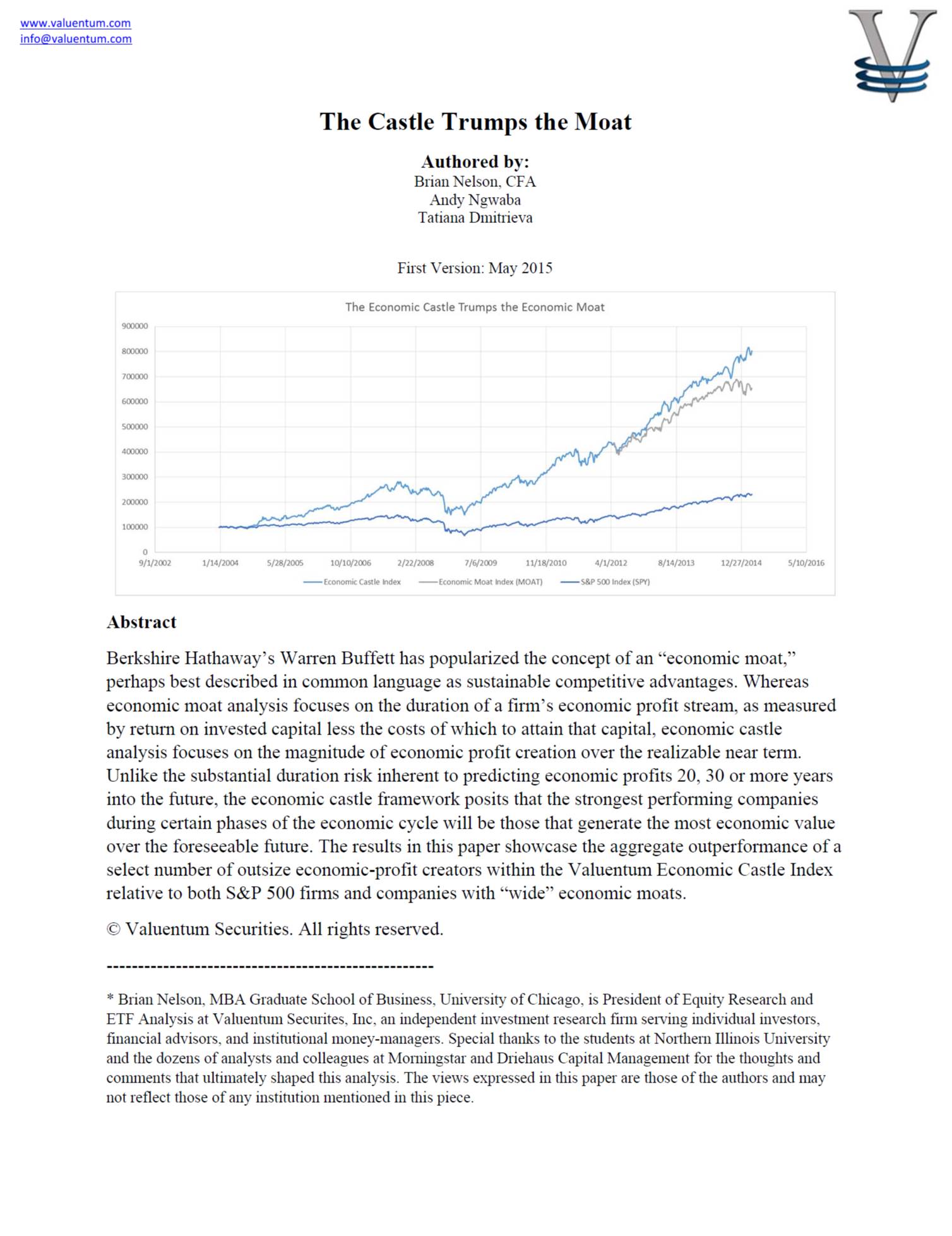

Berkshire Hathaway’s Warren Buffett has popularized the concept of an “economic moat,” perhaps best described in common language as sustainable competitive advantages. Whereas economic moat analysis focuses on the duration of a firm’s economic profit stream, as measured by return on invested capital less the costs of which to attain that capital, economic castle analysis focuses on the magnitude of economic profit creation over the realizable near term. Unlike the substantial duration risk inherent to predicting economic profits 20, 30 or more years into the future, the economic castle framework posits that the strongest performing companies during certain phases of the economic cycle will be those that generate the most economic value over the foreseeable future. The results in this paper showcase the aggregate outperformance of a select number of outsize economic-profit creators within the Valuentum Economic Castle Index relative to both S&P 500 firms and companies with “wide” economic moats.

|