Image: Phillips 66’s shares continue to hover near all-time highs thanks to a favorable energy resource environment.

By Brian Nelson, CFA

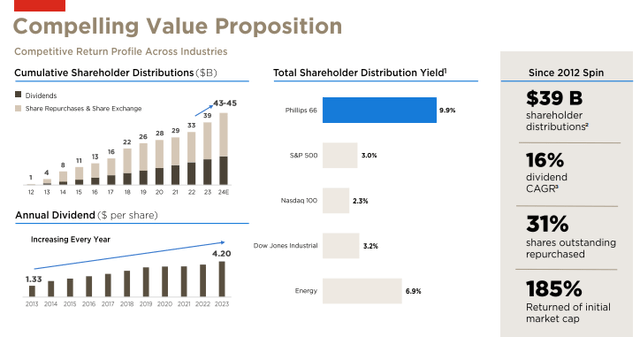

Shares of refining giant Phillips 66 (PSX) continue to hover near all-time highs as the company benefits from a favorable energy resource environment. The company’s fourth quarter non-GAAP earnings per share of $3.09 beat expectations handily, as it hauled in $2.2 billion in operating cash flow in the period. Phillips full-year 2023 performance was solid as it generated $7 billion in operating cash flow and returned $5.9 billion to shareholders in the form of dividends and share buybacks. Shares yield ~2.7% at the time of this writing.

Management remains shareholder-friendly and said much in its fourth-quarter press release:

As we look forward, we will continue to execute our strategic priorities to deliver significant shareholder value. During 2023, we distributed well over 50% of our operating cash flow to shareholders through dividends and share repurchases. We have distributed $8.3 billion to shareholders since July 2022, on pace to achieve our $13 billion to $15 billion target by year-end 2024.

According to reports from Seeking Alpha, higher gasoline prices have driven refining profit margins (i.e. crack spreads) to the highest since August and September of last year. Not only this but Phillips 66 noted that refining operations ran at 92% utilization during the fourth quarter, while for the full-year 2023, it benefited from continued run-rate cost savings. At the end of 2023, Phillips 66 had $3.3 billion of cash and cash equivalents on hand and a net debt-to-capital ratio of 34%, slightly higher than the high end of its target range of 25%-30%.

Image: Phillips 66 continues to be very shareholder friendly returning cash in the form of share repurchases and dividends.

Though crack spreads can be quite volatile at times, there’s a lot to like about Phillips 66. The company is targeting 2025 mid-cycle adjusted EBITDA of $14 billion, up from $10 billion in 2022. Cost savings should remain ongoing, with its target calling for a total of $1.4 billion in savings, implying the company has $200 million more in savings to go. We like its investment-grade (A3/BBB+) balance sheet and target for 2025 mid-cycle adjusted operating cash flow of $10+ billion, up from $7 billion in 2022, with expectations that it will return more than half of operating cash flow to shareholders. Phillips 66 is a quality income idea for investors seeking exposure to the energy space.

NOW READ: 12 Reasons to Stay Aggressive in 2024

NOW READ: 2023 Was a Fantastic Year! Are You Ready for 2024?

———-

Tickerized for PSX, MPC, DK, VLO, DINO, XLE, CRAK

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.