By Brian Nelson, CFA

On July 20, Philip Morris (PM) reported strong second-quarter 2023 results that showed 14.5% reported revenue growth and a non-GAAP earnings per share beat of $0.12. Adjusted operating income faced headwinds from global inflationary pressures, but still advanced 6.9% in the quarter. Adjusted diluted (currency-neutral) earnings per share growth came in at 16.9% in the period. For the full year, Philip Morris is targeting organic sales expansion of 7.5%-8.5% and adjusted diluted earnings per share in the range of $6.13-$6.22 per share on the year, reflecting a high-single-digit pace of expansion and a modest increase from prior expectations.

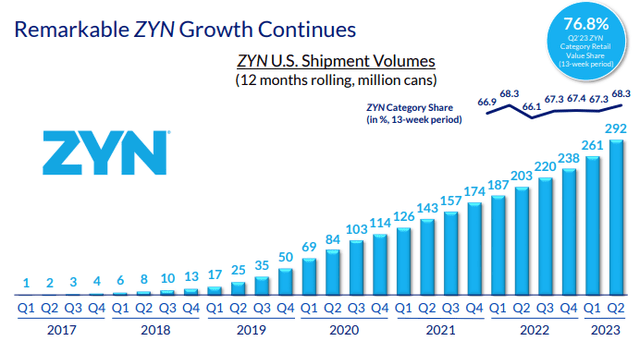

Cigarette makers continue to transition to a smoke-free world, and Philip Morris is walking the line between combustible tobacco and healthier, smoke-free alternatives. The company’s smoke-free product net revenues advanced 34.1% on a year-over-year basis in the quarter, and we like the momentum in this area, not only as it relates to supporting a healthier consumer but also as it relates to the longevity of Philip Morris and the tobacco industry, more generally. The executive team pointed to “outstanding performance of Swedish Match – fueled by growth of ZYN nicotine pouch) in the U.S” as one of the key catalysts of its smoke-free transformation. Shipment volume growth of ZYN was 53%+ in the U.S.

Image Source: Philip Morris

For 2023, Philip Morris is targeting operating cash flow in the range of $10-$11 billion and capital expenditures of $1.3 billion, meaning Philip Morris expects to haul in $8.7-$9.7 billion in free cash flow on the year. The expected performance in operating cash flow is about in line with what Philip Morris put up last year, while capital spending continues to expand, with its target for this year more than double that of 2020. The strength in free cash flow, however, will still handily cover expected cash dividends paid of ~$7.5-$8 billion on the year, but we do note that the cash-flow coverage isn’t as strong as it was just a couple years ago in 2021. Total debt of $45.2 billion at the end of March is not ideal.

Our fair value estimate for Philip Morris stands at $105 per share, and we don’t expect to make any material changes to our valuation of the company following the quarterly report. Philip Morris’ combustible tobacco revenue continues to be strengthened by pricing power, while its smoke-free momentum, particularly with ZYN, continues. Though adjusted financial measures continue to look good at Philip Morris, more and more we’re paying closer attention to reported diluted earnings per share, which will face material pressure in 2023 ($5.36-$5.45 per share) compared to $5.81 per share in 2022. The company’s free cash flow remains robust, but its total debt levels are not ideal, in our view. Philip Morris is trading just shy of $100 with a dividend yield of ~5.2% at the time of this writing.

———-

NOW READ: Philip Morris’ First-Quarter 2023 Results Just Okay

NOW READ — ALERT: Big Yield Additions to Dividend Growth Newsletter Portfolio and High Yield Dividend Newsletter Portfolio

NOW READ — ALERT: Going to “Fully Invested” in the Best Ideas Newsletter Portfolio

NOW READ — Expect Huge Equity Returns This Decade, Much More Volatility However

NOW READ — There Are No Free ‘Income’ Lunches

———-

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, and RSP. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.