Image Source: Domino’s Pizza Inc – 2022 ICR Conference IR Presentation

By Callum Turcan

Recessionary clouds are building across the globe at a time when inflationary pressures are running rampant. Only high-quality companies should be seriously considered during turbulent times such as these, and in our view, Domino’s Pizza Inc (DPZ) fits the bill. Domino’s operates of the best delivery operations out there, one supported by a top-notch digital presence and a popular customer loyalty program. We include shares of Domino’s in the simulated Best Ideas Newsletter portfolio, and our fair value estimate for DPZ sits at $374 per share, materially above where shares of DPZ are trading at as of this writing. Furthermore, shares of DPZ yield ~1.3% as of this writing, and its income growth potential offers incremental upside to its capital appreciation potential.

Earnings Update

On July 21, Domino’s reported second quarter earnings for fiscal 2022 (period ended June 19, 2022) that beat consensus top-line estimates but missed consensus bottom-line estimates. Foreign currency headwinds, a product of the strong US dollar seen of late, held down the firm’s reported performance in the fiscal second quarter. While its global retail sales grew by 1.5% year-over-year in the fiscal second quarter when removing foreign currency movements, its global retail sales fell by 3.0% when including those headwinds.

Its same store sales in the US and internationally declined 2.9% and 2.2% on a year-over-year basis, respectively, in the fiscal second quarter as these metrics are “normalizing” after Domino’s put up banner performance in fiscal 2020-2021. Domino’s noted that its same store sales in the US grew by 11.5% in fiscal 2020 and 3.5% in fiscal 2021, while its international same store sales grew by 4.4% in fiscal 2020 and 8.0% in fiscal 2021 on a year-over-year basis.

The firm’s GAAP revenues rose 4% year-over-year in the fiscal second quarter to reach $1.1 billion, as unit store count growth (which we will cover later in this article) offset headwinds from its declining same store sales and unfavorable foreign currency movements. Domino’s reported that its GAAP operating income dropped by 7% year-over-year in the fiscal second quarter, coming in at $178 million, as a sharp decline in its GAAP gross margin (down ~320 basis points) more than offset a modest reduction in its operating expenses. Food inflationary pressures, supply chain hurdles, rising wage/labor costs, and difficulties finding delivery drivers all weighed negatively on its operational and financial performance.

Domino’s generated $121 million in free cash flow during the first half of fiscal 2022 while spending $40 million covering its total dividend obligations and $98 million buying back its common stock. Share buybacks have historically been partially funded by the company’s balance sheet. Domino’s exited the fiscal second quarter with a net debt load of $4.9 billion (inclusive of short-term debt, exclusive of restricted cash and cash equivalents and noncurrent investments) along with significant operating lease liabilities.

We would prefer that Domino’s bulk up its cash position on hand and reduce its net debt load, something its strong free cash flow generating abilities could make possible. In any event, as Domino’s can generate strong free cash flows in almost any operating environment (a product of its asset-light, franchise-heavy business model), it should be able to stay on top of its net debt load and dividend obligations going forward.

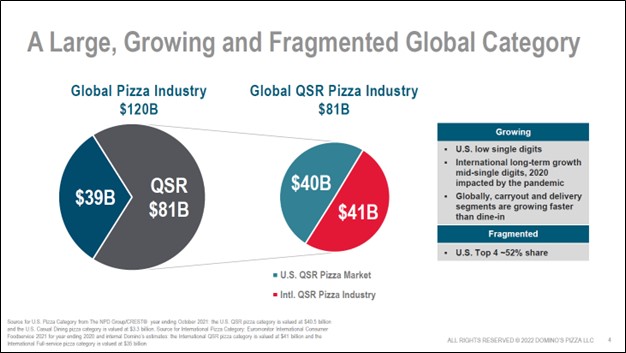

Growth Runway

One of the ways Domino’s is supporting its financials during these turbulent times is by growing its unit store count. Please note that ~98% of its more than 19,200 global locations were franchised as of June 19, 2022, as the unit economics of Domino’s store locations are quite attractive for franchisees. During the trailing twelve month period through the end of the second quarter of fiscal 2022, Domino’s saw its total net unit store count grow by ~1,240 locations with 1,040+ net new stores opened internationally along with 190+ net new locations in the US.

According to Domino’s, it sees room for 8,000+ unit store locations in the US (versus ~6,620 as of June 19, 2022) along with an additional 10,000+ unit store locations across its top international markets. While the potential for a global recession in the near term may slow down the pace of its unit store count growth, the longer term outlook for Domino’s remains bright.

Concluding Thoughts

Domino’s is contending with substantial near-term headwinds, but its longer-term growth runway remains firmly intact. There is ample room for Domino’s to grow its international unit store count and domestically, Domino’s views its unit store count growth runway favorably. Recently, its unit store count has grown at a robust pace as franchisees are drawn to the attractive unit economics of the company’s stores. We continue to like exposure to shares of Domino’s in the simulated Best Ideas Newsletter portfolio.

—–

Discretionary Spending Industry – BBY, CBRL, CMG, DIS, DG, DLTR, DPZ, EL, F, GM, HAS, HD, LOW, MCD, NFLX, NKE, SBUX, TSLA, YUM, DKS, TJX, ROST, WHR, KMX, AZO, RL, ULTA, LEG, GPC, VFC, CTAS, WSM

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares of DIS, META, GOOG, VRTX, and XLE. Chipotle Mexican Grill Inc (CMG), Dollar General Corporation (DG), Domino’s Pizza Inc (DPZ) and The Walt Disney Company (DIS) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Dick’s Sporting Goods Inc (DKS) and Home Depot Inc (HD) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.