Image Source: NodStrum Tech

Streaming giant Netflix continues to grow its subscriber base at an impressive rate as it works to achieve sufficient levels of operating leverage, but its free cash flow burn is as significant as ever as financial obligations mount.

By Kris Rosemann

Shares of market darling Netflix (NFLX) were boosted in the October 17 trading session by strong subscriber growth guidance and better-than-expected profit generation in its third quarter report, released October 16, though management noted a portion of that profit generation was due to marketing costs being pushed in the fourth quarter. Paid net additions came in at 6.07 million in the third quarter, and total paid memberships sat at 130.42 million at the end of the quarter, compared to 124.35 million a quarter earlier and 104.02 million a year earlier. Management’s guidance for subscriber growth in the fourth quarter of 2018 came in at 9.40 million and 7.60 million for net and paid net additions, respectively, which were well above consensus expectations.

Netflix’s revenue jumped 34% on a year-over-year basis, and operating income more than doubled as operating margin expanded to 12% from 7% in the year-ago period. However, free cash flow generation continues to be significantly negative, and management noted that it expects its free cash flow burn to be closer to the lower end of its $3-$4 billion guidance for the full-year 2018. The company expects its 2019 free cash flow burn to be roughly in line with that of 2018.

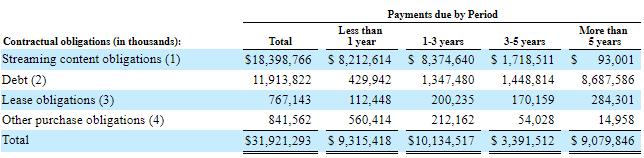

Though we love the operating leverage potential of Netflix’s business as it continues to achieve increasingly attractive economies of scale, the combination of significantly negative free cash flow generation combined with massive financial obligations–both in the form of traditional debt and off-balance sheet obligations such as streaming content obligations–are not an attractive feature of its business. As of the end of the third quarter of 2018, Netflix had $18.6 billion in streaming content obligations, up from $18.4 billion and $17.0 billion a quarter and a year earlier, respectively. Long-term debt on the balance sheet was just over $8.3 billion at the end of the third quarter of 2018, but the image below, taken from Netflix’s second quarter 2018 10-Q, shows the company’s contractual obligations for the years ahead.

Image Source: Netflix second quarter 10-Q

We think these are the kinds of figures investors should be more interested in, as opposed to the massive chart the company included in its third quarter earnings release detailing the number of Instagram (FB) followers stars of its content had and have before and after launches on its platform. Social relevance may very well be a vital portion of any media business, but actor and actress Instagram followings are not going to drive Netflix to positive free cash flow generation.

Management believes it is nearing an inflection point at which growth in operating profit is going to grow faster than growth in content cash spend, which is what will actually drive free cash flow improvement, and the expectation for flat free cash flow burn in 2019 is actually an improvement over the company’s prior internal projections. Material improvements are expected in 2020, but it will still be “a few years towards breakeven because we’re optimizing again for long-term cash flow and long-term profitability,” according to CFO David Wells on the company’s third quarter conference call.

Shares are trading just below the upper bound of our fair value range as of this, and we see no reason to change our fair value estimate at this point in time. Near-term free cash flow generation for the firm may be even worse than the projections in our discounted cash flow model, but the longer-term trajectory of operating margins and free cash flow generation will ultimately tell how the share-price story of Netflix unfolds over the coming years, in our opinion.

Recent significant improvements in operating margin and EBITDA growth are very encouraging signs for those long Netflix, but we continue to believe the company has a lot to prove. Netflix expects to be free-cash-flow negative for a few more years, and its substantial indebtedness earns it a junk-territory credit rating, both of which could spell trouble for equity holders in the event a cyclical downturn pressures consumer spending in a material way. From the fickle nature of consumer preferences to rivals that are only growing stronger, the uncertainty surrounding our fair value estimate remains considerable. In any case, attention grabbing volatility and headlines surrounding Netflix are not going away any time soon.

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Kris Rosemann does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.