Image Source: Microsoft

Microsoft completed its acquisition of social media platform LinkedIn during the course of the second quarter of its fiscal 2017. Otherwise, it was business as usual for the software giant.

By Kris Rosemann

Microsoft (MSFT) reported another solid quarter January 26, “Podcast: Microsoft — Still One of Our Favorites”. Though we prudently took some profits in the software giant more recently, the company’s stock remains firmly entrenched as a core holding in the Dividend Growth Newsletter portfolio, as it has been since portfolio inception. Shares are pushing up against the high end of our fair value estimate range, though we continue to emphasize Microsoft’s fantastic Dividend Cushion ratio, which helps reinforce our dividend thesis on the company. Shares yield ~2.4% at the time of this writing.

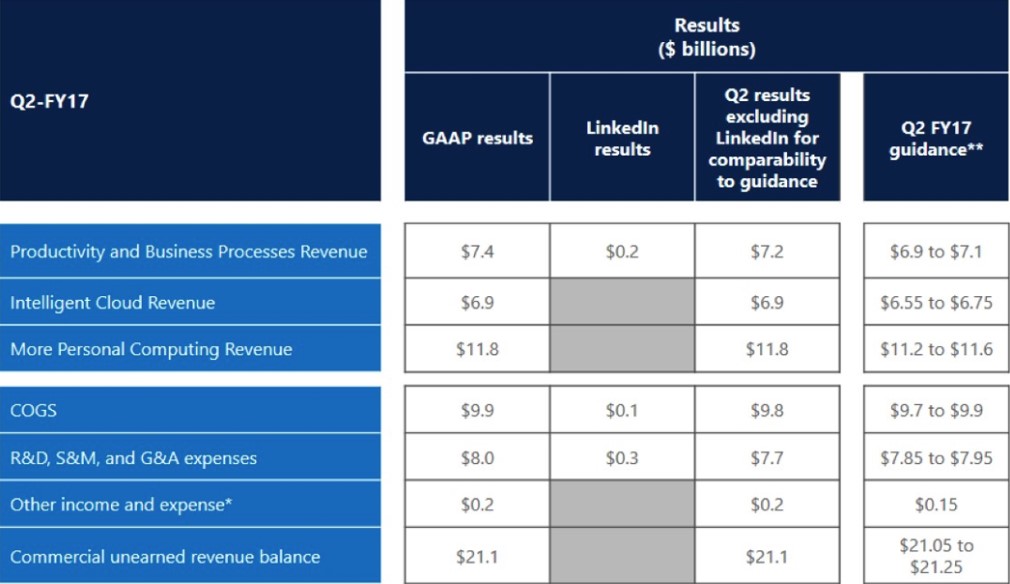

In the second quarter of its fiscal 2017, the software giant completed the acquisition of LinkedIn and kept the momentum rolling in its cloud-based product suite. Microsoft reported improvements pretty much across the board in terms of consolidated financial performance and beat its own expectations for the quarter as non-GAAP revenue, operating income, and net income advanced 4%, 8%, and 10%, respectively, on a constant currency basis from the year-ago period. Importantly, free cash flow leapt nearly 20% in the period, to $4.3 billion, well in excess of cash dividends paid in the quarter of ~$3 billion. The company expects to return a meaningful amount of its copious free cash flow to shareholders in the form of dividends and share buybacks in coming periods. Microsoft is in the midst of another $40 billion share repurchase program, which follows the $40 billion authorization that was completed in 2016.

From our perspective, the impact of the LinkedIn acquisition was lightly felt in terms of Microsoft’s quarterly financial performance (the deal was completed December 8). However, the firm’s balance sheet now reflects the impact of the acquisition, reducing its net cash position to ~$38 billion from more than $62 billion three months earlier. We’re still wary of the long-term implications of the decision to allocate billions of dollars in shareholder capital to a business with less-than-ideal profitability levels and free cash flow generating capacity, and the near-term outlook for the LinkedIn division does very little to inspire confidence the decision will be value-creating over the long haul after considering the massive capital outlay that was required to acquire the assets.

Management expects revenue contributions from LinkedIn in the third quarter of fiscal 2017 (the current quarter) to be approximately $950 million when adjusted for purchase accounting, which compares unfavorably with expectations for the division’s cost of goods sold and operating expenses to be $400 million and $970 million, respectively. Even after adjusting for the amortization of intangible assets acquired, the division is projected to report an operating loss of ~$40 million in the quarter. Though still robust, synergies related to the LinkedIn deal may not be as great as the market believes, especially after considering the autonomy Microsoft plans to give LinkedIn, which will do more to limit potential upside than foster benefits, in our opinion. In some ways, the LinkedIn deal could be considered a distraction.

More directly to the point, Microsoft remains near the top of our list of companies with fantastic dividend growth potential. We’re expecting more of the same impressive free cash flow generating prowess at the software giant that we witnessed in its most recent quarter thanks to its cloud-based product suite. Azure and Office 365 commercial and consumer products and cloud services continue to gain popularity among enterprises and consumers alike. In the third quarter of its fiscal 2017 (the current quarter), Microsoft is projecting meaningful growth in its ‘Productivity and Business Processes’ and ‘Intelligent Cloud’ segments, offering guidance of $7.65-$7.85 billion and $6.45-$6.65 billion, respectively, compared to $6.5 billion and $6.1 billion reported in the third quarter of fiscal 2016. The top-line gains in these areas should more than offset the revenue declines in the ‘More Personal Computing’ segment, which continues to wind down even though the segment is expected to outpace the overall weak PC market in terms of stemming declines.

All in, we continue to hold onto shares of Microsoft in the Dividend Growth Newsletter portfolio, as we closely monitor the integration of LinkedIn, its potential synergies, and how any further investment in the initiative may impact Microsoft’s cash-rich business. The momentum in its various cloud-based products remains fantastic, and we love the annuity-like nature of the subscription-based business model to which Microsoft continues to migrate. Shares are starting to get a little pricey, but in the current overheated market, we expect the software giant’s dividend yield and net cash position to provide substantial support to the stock. We like Microsoft.