Image Source: Caterpillar Inc – May 2022 Caterpillar Investor Day Presentation

By Callum Turcan

In this article, we cover the industrial landscape by digging into the recent financial and operational performance of General Electric Company (GE), Boeing Co (BA), Caterpillar Inc (CAT), Deere & Company (DE), and Union Pacific Corporation (UNP). Common themes include robust demand for their offerings, healthy order backlogs, and meaningful pricing power, though headwinds include substantial inflationary pressures, supply chain hurdles, and in certain instances, geopolitical tensions.

General Electric will soon separate into three different publicly traded companies, and on a consolidated basis the firm is doing much better than years past. In 2022 and on a non-GAAP basis, General Electric is guiding for a 150+ basis point expansion in its adjusted organic operating margin and high-single-digit organic revenue growth, along with $2.80-$3.50 in adjusted EPS and $5.5-$6.5 billion in free cash flow (as defined by the company).

Boeing’s financials continue to be in bad shape, and its operations continue to be plagued by missteps. The aerospace giant exited March 2022 with a massive net debt load of ~$45.5 billion (inclusive of short-term debt) after generating negative free cash flows in each year from 2019-2021. The company also generated negative free cash flows during the first quarter of 2022. Large working capital builds due to its inability to deliver certain aircraft, a product of its lackluster operational execution and regulatory intervention, is largely why Boeing has had difficulties generating positive free cash flows in recent years.

Caterpillar’s first-quarter 2022 results were plagued by margin issues. In the period, the earth moving equipment maker’s GAAP revenues grew 14% year-over-year, but its manufacturing segment only posted a 3% year-over-year increase in operating income as higher costs weighed negatively on its profitability, offsetting pricing increases and increasing economies of scale. Caterpillar’s GAAP operating margin fell by ~140 basis points year-over-year in the first quarter, declining to 13.9%.

During the first half of fiscal 2022, Deere’s GAAP revenues grew by 8% though its GAAP operating profit declined by 4% year-over-year, but the company’s performance in the fiscal second quarter indicates recent pricing actions have started to have a positive impact on its bottom-line performance. Deere raised its full-year earnings guidance in conjunction with its fiscal second quarter earnings update and now expects it will post $7.0-$7.4 billion in earnings this fiscal year.

Union Pacific noted that its business volumes are measured by total revenue carloads increased by 4% year-over-year in the first quarter with strong growth seen at its agricultural and industrial freight volumes. The railroad company’s ‘operating income’ rose 19% year-over-year as its business continued to benefit from ongoing optimization efforts in the first quarter of 2022. The railroad operator remains very shareholder friendly and intends to payout roughly 45% of its earnings to investors as dividends.

General Electric to Separate Into Three Publicly-Traded Companies

During the past several years, General Electric has fundamentally transformed itself, primarily through a series of divestitures aimed at bringing down its leverage. General Electric, in its current form, is built around its ‘Aviation,’ ‘Healthcare,’ ‘Renewable Energy,’ and ‘Power’ business operating segments. The company builds jet engines for commercial and military purposes, diagnostic systems such as ultrasound machines, onshore and offshore wind turbines, and natural gas-fired turbines, among many other things. General Electric also has a financing wing, albeit one that has shrunk considerably during the past decade and a half, and sizable digital-oriented operations as well.

Please note that General Electric is in the process of separating into three publicly traded entities, a development announced back in November 2021. The three new entities are going to be represented by GE Aviation, GE Healthcare, and a combination of GE Renewable Energy, GE Power, and GE Digital. By early 2023, GE Healthcare is expected to be spun off followed by its combined renewable and power unit in early 2024. This move will fundamentally transform General Electric and is the culmination of a major transformation process embarked on over the past decade and a half since its previous business model was upended by the Great Financial Crisis (‘GFC’).

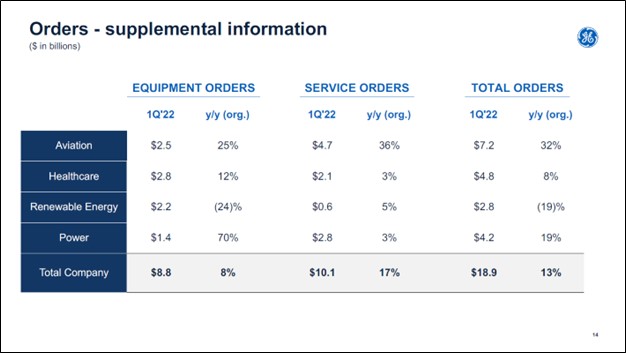

With that in mind, trends in General Electric’s order backlog and margin performance can still provide investors with a useful snapshot of the broader industrial sector. In the first quarter of 2022, General Electric posted a nice bounce in its order backlog for its aviation, healthcare, and power offerings (both equipment and related services), though orders for its renewable energy equipment offerings took a big hit (on a positive note, orders for services concerning renewable energy offerings still grew nicely).

Aerospace activity was devastated during the worst of the pandemic as households hunkered down, though more recently, passenger air travel has staged an impressive recovery and air cargo traffic remains robust. The outlook for Western national defense spending is also robust due to rising geopolitical tensions. Due to General Electric’s sizable aerospace operations, the firm has meaningful exposure to these tailwinds.

Image Shown: Overall, General Electric experienced nice growth in its equipment and services backlog on a company-wide basis during the first quarter of 2022. Image Source: General Electric – First Quarter of 2022 IR Earnings Presentation

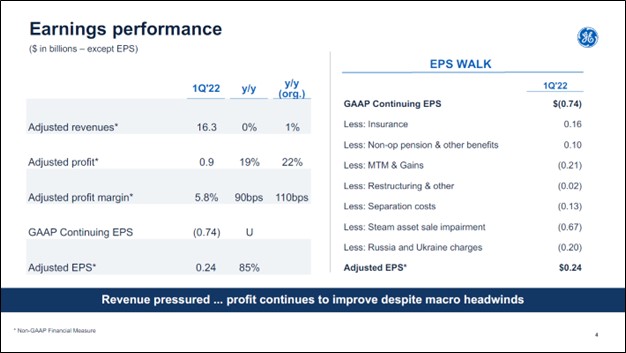

In the first quarter of 2022, General Electric’s GAAP revenues declined marginally year-over-year as strength at its aviation and healthcare segments were weighed down by weakness at its power and renewable energy segments. The firm’s GAAP gross margin stood at 26.9% in the first quarter, up ~35 basis points on a year-over-year basis, with strength seen at its aviation, healthcare, and power segments which was moderately offset by weakness at its renewable energy segment. Strong growth in its higher margin services sales supported its performance here, though inflationary pressures and supply chain hurdles represented major headwinds, especially for its healthcare and renewable energy operations according to recent management commentary.

Due primarily to various special items, General Electric’s GAAP operating income and net income from continuing operations were both negative in the first quarter. On a non-GAAP basis, General Electric’s adjusted revenues were flat year-over-year in the first quarter while its adjusted profit rose by 19% and its adjusted profit margin increased by ~90 basis points. Restructuring costs, separation expenses, costs relating to its suspension of most operations in the Russian market, and various other charges weighed negatively on General Electric’s GAAP performance in the first quarter.

Image Shown: General Electric sees its underlying financial performance trending in the right direction, though we caution that non-GAAP financial metrics always need to be taken with a large pinch of salt. Image Source: General Electric – First Quarter of 2022 IR Earnings Presentation

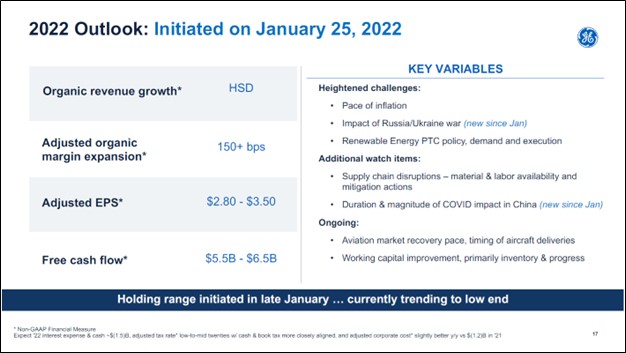

In 2022 and on a non-GAAP basis, General Electric is guiding for a 150+ basis point expansion in its adjusted organic operating margin and high-single-digit organic revenue growth, along with $2.80-$3.50 in adjusted EPS and $5.5-$6.5 billion in free cash flow (as defined by the company). For reference, General Electric generated -$0.07 (negative $0.07) and $1.71 in adjusted EPS in 2020 and 2021, respectively, highlighting the powerful rebound its business is currently experiencing. The pandemic hurt the company’s financials, though demand for its offerings has rebounded at a robust pace in recent quarters as the global economy recovered.

We caution that exogenous shocks–with an eye towards inflationary pressures, supply chain hurdles, and geopolitical tensions–could hinder General Electric’s ability to achieve its guidance. Management noted during General Electric’s first quarter earnings update in late April 2022 that the firm was trending towards the lower end of its guidance ranges, though the firm felt confident in maintaining its full-year guidance laid out in late January 2022.

Image Shown: General Electric is contending with various headwinds that may make achieving its full-year guidance, as laid out in late January 2022, difficult to achieve. Image Source: General Electric – First Quarter of 2022 IR Earnings Presentation

General Electric has its work cut out for it, though ongoing efforts to improve its cost structure along with apparent strong demand for its offerings (seen through solid order growth across most of its portfolios) indicates the firm has a chance to right the ship. At the end of March 2022, General Electric had $33.5 billion in total debt on the books (inclusive of short-term debt), with $12.8 billion in cash and cash equivalents on hand (along with substantial current and noncurrent investment securities on hand) providing the firm with ample liquidity to meet its near term funding needs.

The company generated negative free cash flow during the first quarter of 2022, though management expects that to improve going forward as General Electric benefits from aircraft delivery activities from its customers resuming in earnest. In 2021, General Electric generated $2.0 billion in free cash flow and spent $0.6 billion covering its modest dividend obligations (in November 2017, General Electric announced it would reduce its dividend to a token penny per share where it has stayed to this day after adjusting for its 8:1 reverse stock split completed in 2021). It did not spend a meaningful amount (or any) buying back its stock in 2021 or during the first quarter of this year.

General Electric’s outlook has improved materially during the past two years, albeit off of an incredibly low base, and we are keeping an eye on its planned separation. Shares of GE yield a modest ~0.5% as of this writing.

Boeing’s Financials, Operational Hiccups Leave the Stock “Uninvestable,” In Our View

As is the case with General Electric, Boeing is benefiting immensely from recovering passenger air travel demand while the outlook for defense spending in Western countries is quite robust due to rising geopolitical tensions. Boeing’s order backlog is steadily recovering though its financial strength remains lackluster as the firm has been dealing with several crises in recent years, such as the 737 MAX getting grounded in March 2019, and it does not look like the negative headlines will disappear anytime soon as its 787 aircraft is now dealing with immense regulatory scrutiny. Boeing has not delivered any of its 787 aircraft since May 2021, creating major headwinds for its financial performance.

Image Shown: Passenger air travel activity is steadily recovering from the pandemic and air cargo traffic remains robust, supporting Boeing’s longer term outlook. Image Source: Boeing – First Quarter of 2022 IR Earnings Presentation

Boeing exited March 2022 with a massive net debt load of ~$45.5 billion (inclusive of short-term debt) after generating negative free cash flows in each year from 2019-2021. The company also generated negative free cash flows during the first quarter of 2022. Large working capital builds due to its inability to deliver certain aircraft, a product of its lackluster operational execution and regulatory intervention, is largely why Boeing has had difficulties generating positive free cash flows in recent years.

In March 2020, Boeing suspended its dividend as it contended with a rapidly deteriorating outlook for aircraft demand in the wake of the early days of the pandemic and large working capital builds due to the grounding of its 737 MAX aircraft (which wasn’t cleared to fly again in the US by the Federal Aviation Administration until late 2020). Back in April 2019, Boeing suspended its share buyback program. As an aside, Boeing suspended its operations in Russia (it is no longer offering services, parts, and support to Russian airlines) and also is no longer buying titanium from Russia.

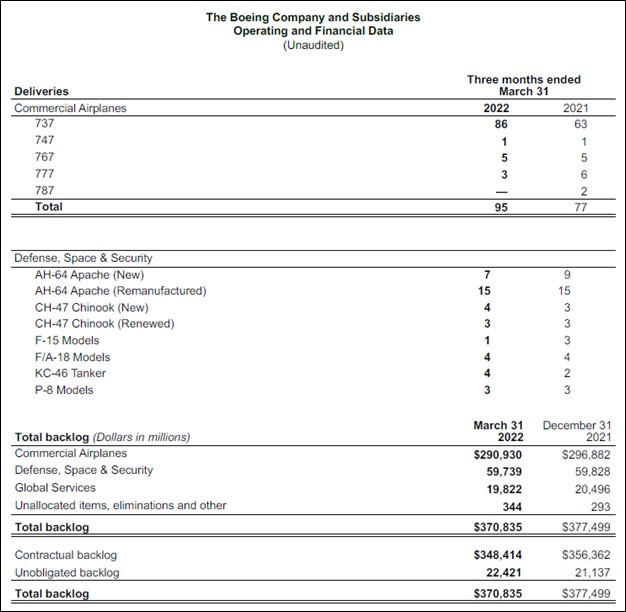

One of the few things working in Boeing’s favor is its strong order backlog, which stood at $370.8 billion at the end of March 2022. That covered ~4,200 commercial aircraft with a backlog worth $290.3 billion, followed by a $57.7 billion backlog relating to national defense needs (defense, space, and security) along with a sizable services backlog. Boeing delivered 95 aircraft in the first quarter of 2022, up from 77 aircraft in the same period in 2021. Deliveries of Boeing’s national security offerings remained robust in the first quarter of 2022 and was broadly flat, in unit terms, versus the same period last year.

The company’s backlog declined modestly (down $6.6 billion) from the end of December 2021 to the end of March 2022, primarily due to Boeing picking up the pace of its deliveries, though its backlog still remained enormous. At the end of December 2020, Boeing’s backlog stood at $363.4 billion (covering ~4,000 commercial aircraft along with sizable defense, services, and other offerings), indicating its order book has more or less resumed its growth trajectory over the past several quarters.

Image Shown: Boeing’s total backlog remains enormous and its commercial aircraft deliveries are steadily picking up the pace. Image Source: Boeing – First Quarter of 2022 Earnings Press Release

Boeing will need to step up its aircraft production activities and ultimately its deliveries to realize meaningful economies of scale while improving its cash flow generating abilities going forward. Manufacturing hiccups remain, and management will need to improve Boeing’s operational execution in order to improve the firm’s cost structure and financial performance. Resuming deliveries of its 787 aircraft while scaling up the pace of its 737 MAX production activities would go a long way in supporting Boeing’s future financial performance.

Caterpillar Feeling a Pinch on Its Margins

When Caterpillar posted first quarter 2022 earnings in late April 2022, the industrial equipment manufacturer beat both top- and bottom-line estimates. Its GAAP revenues grew 14% year-over-year to hit $13.6 billion due primarily to its ‘Machinery, Energy & Transportation’ revenues (Caterpillar’s manufacturing segment) growing by 15% to reach $12.9 billion.