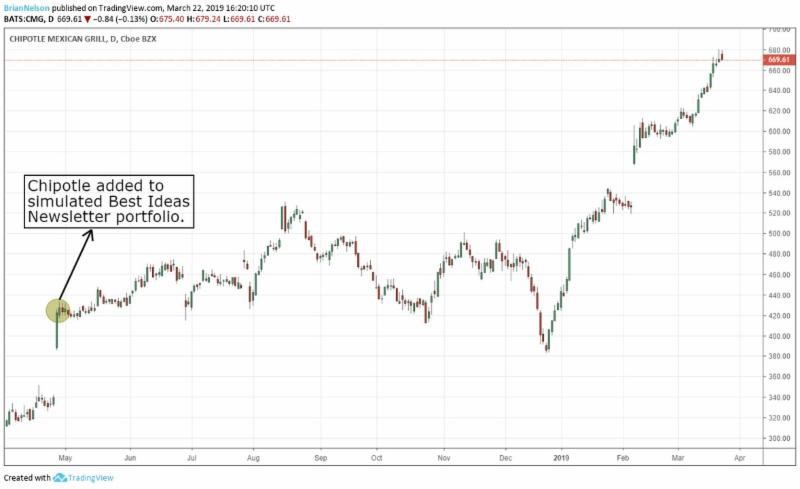

Image shown: Chipotle (CMG) has been one of our best calls so far in 2019.

No changes to simulated newsletter portfolios. Tickers mentioned: AAPL, AMZN, BRK.B, CMG, CVS, FB, GE, JPM, KMI, PYPL, V, XLNX.

Let’s talk about the newsletter portfolios, some areas where we’ve made mistakes, and how some members use our services.

By Brian Nelson, CFA

I love it when I get questions because it shows the engagement of our members. I appreciate that very much. Though there are other considerations, of course, the Valuentum methodology is really quite simple: dividend growth considerations aside, we like undervalued ideas that are going up, and we generally won’t remove ideas that are overvalued until their technical/momentum indicators turn over. Here’s more about our methodology in action.

A stock’s Valuentum Buying Index (VBI) rating is based on our view of the attractiveness of a company’s discounted cash-flow valuation, its relative valuation versus peers, and an overall technical/momentum assessment. If our views on any of these three investment pillars change, a company’s Valuentum Buying Index rating will change to reflect this new view. We use our methodologies and our experience and judgment to build and adjust the newsletter portfolios. Achieving the goals of the newsletter portfolios is our primary objective with our regular premium service. If you’re focused only on our report-update cycle, you’re missing the forest for the trees.

As it relates to the Best Ideas Newsletter portfolio, for example, if a stock registers a 9 or 10 on the Valuentum Buying Index in our coverage universe, we would consider adding it to the newsletter portfolio. When the stock then/eventually registers a 1 or 2 on the Valuentum Buying Index in time, we might then consider removing it from the newsletter portfolio. The changes in the “big middle” of the Valuentum Buying Index offer more tactical considerations, but we generally only consider the highest and lowest VBI ratings to be material. During times of market froth, however, as in arguably today’s environment, in the Best Ideas Newsletter portfolio, we may relax some of the VBI criteria and consider undervalued stocks with neutral technical/momentum indicators, or fairly valued stocks with good relative valuation metrics and strong technical/momentum indicators. We may only consider removing ideas from the simulated newsletter portfolios when both their valuation and technical/momentum indicators point in the same direction (good/good or poor/poor), or if we’re making more strategic/tactical moves.

The criteria for the Dividend Growth Newsletter is somewhat different. We’re looking for strong dividend growth stocks in the Dividend Growth Newsletter portfolio (something that is not a part of the criteria in the Best Ideas Newsletter portfolio), meaning that in addition to considering the VBI and fair value estimate range, the Dividend Cushion ratio is also very important. We still look to add highly-rated stocks on the VBI and those that are undervalued to this newsletter portfolio, but we may be more open to ideas that have strong dividend growth prospects, on the basis of the forward-looking Dividend Cushion ratio. After adding ideas to the Dividend Growth Newsletter portfolio, we may continue to include them in the portfolio even if they have modest VBI ratings that are trading within our fair value estimate range, as long as they have strong dividend growth prospects. We’d only consider removing a stock from the Dividend Growth Newsletter portfolio when we lose confidence in its intrinsic value support and its dividend growth prospects.

The way to think about our process is rather simple. In the Best Ideas Newsletter portfolio, if a company registers a high rating in our coverage universe, we consider adding it (but we won’t consider adding all companies because of portfolio constraints). If we do decide to add the idea, then we watch its fair value estimate and technical/momentum indicators as it navigates the “big middle” of VBI ratings, and only consider removing the idea from the Best Ideas Newsletter portfolio if it registers a 1 or 2 on the Valuentum Buying Index. In the Dividend Growth Newsletter portfolio, we pay attention to the price-versus-fair value estimate range and the company’s Dividend Cushion ratio, as we’re looking for resilient equities with intrinsic-value support that have strong dividend growth prospects. Only when intrinsic-value support and dividend growth strength wane will we consider removing an idea from the Dividend Growth Newsletter portfolio.

We talk a lot about our winners (thank goodness we have a lot of them!), from Apple (AAPL) to PayPal (PYPL) to Chipotle and beyond, but how about one that didn’t work out: CVS (CVS) was a rare idea in the newsletter portfolios that didn’t quite live up to our expectations a couple years ago. That’s okay. In the context of 15-20 ideas (or a total of 40 or so in both newsletter portfolios in the premium membership), we’re going to get a few wrong. But we didn’t dwell on our mistake. We removed CVS from the newsletter portfolios February 2018, more than a year ago now, and we didn’t look back (in fact, we added a couple months later what turned into a big winners in Chipotle and Xilinx). Here’s what we said more than 12 months ago about CVS, on February 8, 2018:

We think we’ve seen enough with the myriad risks that have found their way into the CVS “story.” From the Amazon (AMZN)-Whole Foods scare to Amazon teaming up with Berkshire Hathaway (BRK.B) and JP Morgan (JPM) to form a new healthcare company, the long-term outlook for CVS has become even more cloudy. Its purchase of Aetna (AET) may have been the straw that broke the camel’s back to our thesis, and we can neither see relief with respect to the structural dynamics of the industry in which it operates, nor can we see its increased leverage and competitive environment a positive for the dividend. We are removing CVS from both the simulated Dividend Growth Newsletter portfolio and the simulated Best Ideas Newsletter portfolio.

Shares of CVS have continued to plummet since we removed it from the newsletter portfolios and could now probably be added to the long list of newsletter portfolio removals from General Electric (GE) to Kinder Morgan (KMI) where we avoided even further declines, a good thing. When structural dynamics change, so should theses, and removing CVS more than a year ago from the newsletter portfolios was the right call. We can’t look back, and we even replaced the company a couple months later in the Best Ideas Newsletter portfolio with Chipotle, which is up huge since that time, and subsequently in the Dividend Growth Newsletter portfolio with Xilinx (XLNX), which we removed February 14, 2019 for a huge “gain.”

Diversification simply matters. There will be winners, and there will be losers in any portfolio. This is just a fact of investing, and it is only more obvious when we produce all of our work in full transparency (again, a good thing). However, what should be clear if you have been following our methodology effectively is how important it is to not stick with falling equities (knives) without balance-sheet net cash support, especially those that encounter structural changes to their business models that bring into question the resilience of their intrinsic value (e.g. CVS). We only retain conviction in an equity with a falling price when it has substantial net-cash support from the balance sheet, tremendous future expected free cash flow generation, and moaty business-model characteristics.

Apple and Facebook (FB), whose share prices have faced declines recently, fit this mold, but CVS just didn’t, so we let it go February 2018. There may be members that are still hoping for a turnaround in CVS, but we’re not expecting one. We have little, if any, interest in CVS at this point. We’ve moved on. We’re now laser-focused on the strength of Visa (V) and the recoveries in Apple and Facebook, and the strong performance from Chipotle and other ideas in the Best Ideas Newsletter portfolio and Dividend Growth Newsletter portfolio. We simply can’t look back. CVS just isn’t part of the picture anymore. With all of this being said, I wanted to share an example of how one of our long-time members has been using our service:

Your screener does a great job in showing the price/fair (P/FV) value ratio and it’s what I’ve used in the past to make purchase or sell decisions. What I learned (and you rightly point out) is that it is only one of the factors that should go into making a transaction decision. The other parts “forward-looking behavioral (relative) valuation multiples and then technical and momentum indicators” are really really important. In isolation. the price/fair value ratio should not be the only criteria. A stock could have a favorable ratio but have negative or neutral on momentum, for example…Also, on a complimentary note, I’ve never bought a stock based on a favorable ratio and then it has become a VBI 9 or 10. So I’ve never been ahead of you guys so to speak, lol. The point is the other parts of what make up the VBI should not be underestimated in their importance.

As you are aware, the Valuentum process is multi-faceted based on a price-to-fair value estimate (derived by enterprise valuation), a relative (behavioral) valuation concept, and technical/momentum indicators. It sounds complicated, but it really just boils down to liking stocks that are undervalued and are going up (can you imagine I wrote a 350-page book on this rather simple construct?). Importantly, we pursue a modified approach in the Dividend Growth Newsletter portfolio, using the Dividend Cushion ratio, which is a forward-looking free-cash-flow-based measure of dividend health. Dividend growth analysis is different than the Valuentum process, though there are overlapping similarities (e.g. intrinsic value analysis, free cash flow assessment, business-model evaluation, etc.).

With all this said, don’t forget to dig into my new book, Value Trap: Theory of Universal Valuation. I’m not selling books. I have thoughts and views that I want to share, and they are screaming to come out. My passion for investing and helping investors seems to be limitless. I really need you to read the text to get inside my head to understand all of this! Please keep the questions coming, too. That’s it for today. Our latest performance update for the Best Ideas Newsletter portfolio can be found here. In case you missed the latest edition of the Best Ideas Newsletter, the March edition, it can be downloaded below. Thank you for reading!

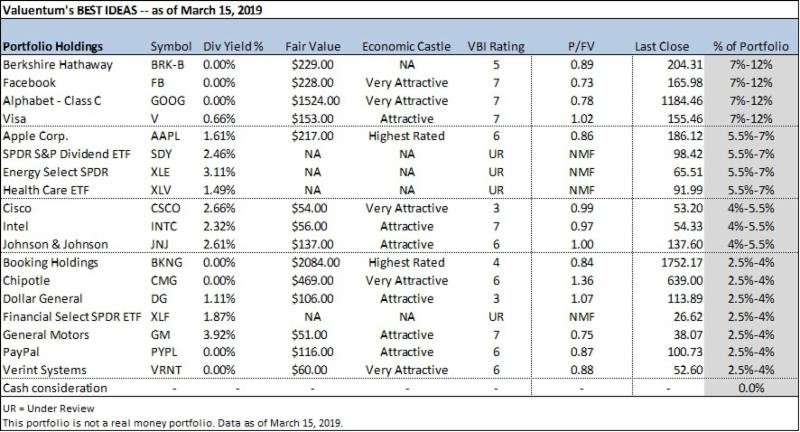

Image shown: Valuentum migrated to a weighting range format for the Best Ideas Newsletter portfolio ideas beginning in 2018.

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.