Image Source: kennijima

By Alexander J. Poulos and Brian Nelson, CFA

The pharmaceutical industry remains an area of innovation with numerous life-altering therapies brought forth to treat the many afflictions that plague us. The industry lifeblood remains the tenuous path of research and study. There is not a foolproof way to predict how a compound will respond until full clinical trials are completed and analyzed, and even successful commercialization cannot be guaranteed should a drug be approved, regardless of the time and costs invested. A later stage clinical failure, for example, could devastate a smaller company, with its equity never to recover.

That’s in part why we tend to prefer larger, more diversified, entities within the pharma/biotech arena as the hit-or-miss riskiness of a one-trick biotech may be too great for prudent and reasonable capital to bear. The Health Care Select SPDR (XLV) is one of our favorites for this very reason. However, whereas a larger, more diversified entity may be better able to absorb the hit of lost opportunity, even their shares can face challenges when things don’t go as planned. Bristol-Myers Squibb (BMY), for example, has come under enormous strain as the clinical outcomes of its crucial product Opdivo (Nivolumab) continue to come under fire. Let’s talk more about this.

Opdivo

Opdivo remains Bristol’s key clinical backbone in its hope of dominating the burgeoning field of immune-oncology (I-O). The concept is very straightforward; the goal is to develop targeted therapies that activate the bodies own immune responses to fight off cancerous cells. The theory is by utilizing the host’s immune response, the side-effect profile will diminish, and a more robust response will be generated to fight off cancer.

Opdivo jumped out of the gate as the first to hit the market. The product produced an impressive string of various approvals, which allows for a broadening of the compounds label. The additional indications are key, as the broader label allows the product to be used to treat various forms of cancer, thereby substantially increasing the total addressable patient population. Shares of Bristol exploded higher, more than doubling since the introduction of Opdivo as the compound seemed poised to dominate the field. Opdivo’s upward trend of adoption seemed assured, with the largest prize–first line therapy for non-small cell lung cancer–well in its sight.

However, Bristol recently shocked the market with a clinical failure of Opdivo used in monotherapy, and when further results showed that Opdivo was inferior to chemotherapy, the company’s share price dropped to $50. Making matters worse, chief rival Merck (MRK) with its I-O therapy dubbed Keytruda was able to garner a win in first-line monotherapy for Non-Small Cell Lung Cancer (NSCLC) utilizing a narrower patient population than Bristol. In our view, by designing the study to incorporate all patients instead of those who are considered high expressors of PD-1, Bristol made a tactical blunder. To add to the disappointment, Opdivo is approved for second-line monotherapy for NSCLC based on the impressive results of the Checkmate-057 trial.

To say the least, the clinical failure shocked a lot of investors.

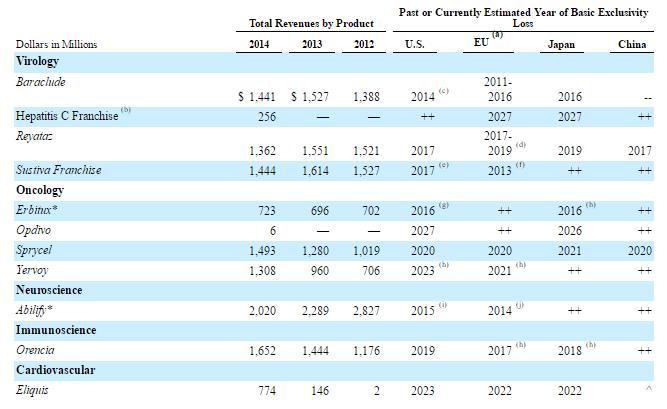

For the Bristol bulls, the hope shifted to combination therapy to tackle NSCLC. We generally believe the optimal treatment may require some form of combination therapy, and that may mean Bristol could utilize its in-house treatments by combining Opdivo with Yervoy. Optimism was running high as Bristol looked for an accelerated filing based on the results of the recently-concluded interim trial results combining Opdivo and Yervoy. However, Bristol recently posted a regulatory update saying it would not seek an accelerated approval for the combination therapy. Though disappointing, we don’t think this is the last we’ve heard from Bristol-Myers on the topic, and we’ll be monitoring future developments closely.

In light of the considerable selling pressure in shares, however, we think the sell-off in Bristol-Myers’ equity is likely an overreaction to the string of recent bad news (shares trade below the lower bound of our fair value esitmate range). The remainder of this piece will focus on the key compounds that Bristol controls outside of news-making Opdivo, all of which drive our fair value estimate of shares.

Eliquis

Eliquis is a crucial member of the next generation of anti-coagulant therapies. Eliquis is co-marketed by Pfizer (PFE), and the partnership is an excellent way to utilize Pfizer’s extensive sales force and reduce overall costs, which remain elevated as Bristol continues to fund numerous oncology clinical trials.

The power of the combined sales force is evident by the market share gains made by the compound. Eliquis was the third product to hit the market with Boehringer Ingelheim the first to market with Pradaxa. Similar with Pradaxa, Eliquis requires twice-a-day dosing, which often impedes overall compliance versus its chief rival Xarelto with its once-a-day dosage requirement. Eliquis is on pace to exceed Xarelto sales based on its lead in new Rx’s written. Sales of Eliquis continue to ramp higher with 9-month sales for 2016 eclipsing $2.3 billion. At the current run rate, sales should exceed $3 billion in 2016, cementing Eliquis as a blockbuster therapy and enviable cash cow.

We feel there is ample room to expand the overall anti-coagulant market. Outside of price, the chief impediment remains the unavailability of a reversal agent. Warfarin the standard for many decades has a reversal agent which is utilized to stop bleeding in case of an overdose or adverse event. Warfarin does have a host of drawbacks, most notably significant food-drug interactions in addition to a multitude of drug-drug interactions. A few promising reversal agents are working their way through the various stages of clinical trials.

Bristol and Pfizer, for example, have provided a $50 million dollar loan to Portola Pharmaceuticals (PTLA) for its key product AndexXa. AndexXa is a promising antidote for Factor Xa inhibitors class which includes Eliquis. The AndexXa application was recently accepted for priority review by the FDA. By funding the process, Bristol/Pfizer will be paid back through royalties from AndexXa sales, but the bigger payoff, in our view, remains market share expansion.

The Eliquis franchise looks secure until 2023 when the primary patent coverage will lapse. We do expect Bristol to make an attempt to extend the patent, but for now, we are using 2023 as the base case in our assumptions.