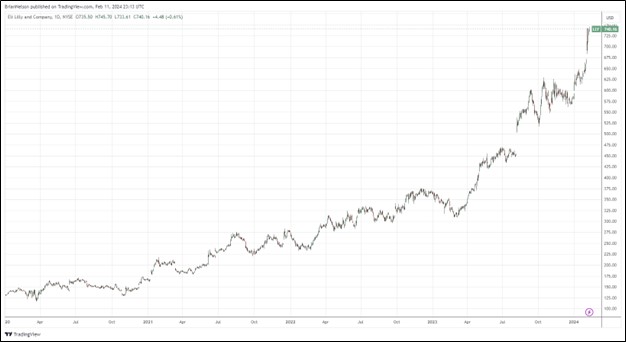

Image: Eli Lilly’s shares have been on a tear these past few years.

By Brian Nelson, CFA

On February 6, Eli Lilly (LLY) reported excellent fourth-quarter results that showed revenue and non-GAAP earnings per share coming in better than expectations. The company’s fourth-quarter results were bolstered by sales of diabetes and weight-loss drug Mounjaro, which saw sales in the quarter leap to ~$2.2 billion from ~$279 million in the year ago period. We continue to be in awe of the sales momentum behind GLP-1 receptor agonists, and the opportunity continues to be robust, despite already rapid sales acceleration. Though Eli Lilly trades at a premium to the high end of our fair value estimate range, we may be low in our expectations of the company’s ability to tap this lucrative market in the longer run, and shares may still be attractive to the risk-seeking aggressive growth investor.

In the quarter, Eli Lilly’s ‘New Products’ revenue grew by ~$2.19 billion, to ~$2.49 billion, thanks to strength in the aforementioned Mounjaro, but also injectable weight loss GLP-1 drug Zepbound, which was only commercialized recently, but experienced ~$176 million in sales in the quarter. The company witnessed a 9% increase in its ‘Growth Products’ revenue in the quarter thanks to strength in metastatic breast cancer medication Verzenio and antidiabetic medication Jardiance, where sales increased 42% and 30% in the quarter, respectively. Taltz, which is used for the treatment of autoimmune diseases, and Olumiant, which is used for rheumatoid arthritis and alopecia areata, also experienced nice year-over-year sales increases in the quarter.

Overall, revenue increased 28% in the quarter, despite 14% lower revenue from Trulicity, and management was upbeat about the progression of its pipeline in the press release:

Pipeline progress included FDA approval of Zepbound for adults with obesity or overweight with weight-related comorbidities and Jaypirca for chronic lymphocytic leukemia or small lymphocytic lymphoma under the Accelerated Approval Program. Additional progress included positive results from SYNERGY-NASH, a Phase 2 study of tirzepatide in adults with nonalcoholic steatohepatitis (NASH), also known as metabolic dysfunction-associated steatohepatitis (MASH).

Eli Lilly is also benefiting from higher prices, as its non-GAAP gross margin expanded 1.8 percentage points in the quarter, to 82.3%. Roughly 16 percentage points of the 28% increase in revenue in the quarter was driven through higher realized prices, with 11 percentage points coming from volume, with a one percentage point increase coming from a favorable impact of foreign exchange rates. Revenue in the U.S. advanced 39% in the quarter, while revenue outside the U.S. advanced 10%. With such a strong growth runway ahead of it and a nice pipeline to boot, Eli Lilly is not backing down with respect to R&D spending, which advanced 28% in the quarter. On a non-GAAP basis, both net income and earnings per share advanced 19% in the period.

We’re also liking what Eli Lilly is doing with respect to ESG initiatives. The firm’s ESG highlights are many, but a few that we really liked include making Lilly insulin available for $35 or less per month, providing as much as $95 million in disaster relief and humanitarian assistance in 2022, reducing its greenhouse gas emissions across its business by more than 20% between 2000 and 2022, having 49% women in management globally (25% of U.S. management positions held by minority group members), and spending $358 million with black-owned businesses in the U.S, an increase of 150% over 2020 levels (Source: the firm’s website, retrieved February 11, 2024). The company is also committed to sourcing all of its purchased electricity from renewable sources by 2030, while becoming carbon neutral in its own operations by the same year.

Looking to all of 2024, Eli Lilly expects revenue to grow ~20% to the range of $40.4-$41.6 billion (was $34.1 billion in 2023 and $28.5 billion in 2022) thanks to strength in sales of Mounjaro, offset by continued weakness in Trulicity. Non-GAAP earnings per share is expected in the range of $12.20-$12.70 for 2024, up significantly from the $6.32 mark and $7.94 mark it achieved in 2023 and 2022, respectively. Through 2023, Eli Lilly has increased its dividend by ~15% for the past few years and has more than doubled its payout since 2018. Given its strong Dividend Cushion ratio, we expect continued strong dividend increases at Eli Lilly for years to come. When it comes to a firm with tremendous business momentum, a solid dividend, and strong ESG initiatives to boot, Eli Lilly is a worthy consideration.

—–

Tickerized for holdings in the XLV.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.