By Brian Nelson, CFA

AbbVie (ABBV) Facing Pressure on Humira Sales But Companywide Revenue Outlook Remains Robust

On February 2, pharma giant AbbVie reported mixed fourth-quarter results with revenue coming in ahead of expectations, but non-GAAP earnings per share coming in slightly lower than the consensus forecast. In the quarter, worldwide net revenue fell 5.4% as the firm continues to work through biosimilar competition against its blockbuster Humira, where net revenues fell more than 40% in the quarter on an operational basis. Global sales of Skyrizi and Rinvoq, however, still powered ahead, advancing nearly 52% and 63% in the quarter on an operational basis, respectively. Its oncology portfolio faced pressure from declining sales of Imbruvica, while it experienced particular strength in its neuroscience portfolio and a solid revenue increase in its aesthetics portfolio in the quarter. Fourth-quarter adjusted diluted earnings per share dropped 22.5% in the quarter on a year over year basis, however. Looking forward, management expects revenue growth to compound at a high-single-digit rate through 2029 thanks to strength in Skyrizi and Rinvoq and with increased contributions from Ubrelvy and Quilpta. For 2024, adjusted diluted earnings per share is targeted in the range of $11.05-$11.25. AbbVie is handling pressures on Humira quite well, in our view, and the company yields 3.7% at the time of this writing.

Chevron’s (CVX) Free Cash Flow of the Dividend Remains Strong, Ups Payout

Chevron reported fourth-quarter results February 2 that showed weakness on the top line, but slightly better-than-expected performance on the bottom line. Fourth-quarter results were messy with U.S. upstream impairment charges and decommissioning obligations, but Chevron is doing a great job returning cash to shareholders, and the firm registered the best year on record for oil and natural gas production. For 2023, net cash from operating activities totaled $12.4 billion, a slight decline from last year, while capital spending came in at $4.4 billion, resulting in ~$8.1 billion in free cash flow, a level that is much higher than what it paid out in cash dividends on common stock for the year ($2.8 billion), indicating that its dividend is very healthy. Management must be thinking the same thing as it increased its quarterly payout 8%, to $1.63 per share. Though we’re generally not fans of acquisitive activity, Chevron remains active on this front, recently bringing PDC Energy and a majority stake in ACES Delta, LLC into the fold, and signing a deal to buy Hess Corp (HES). We like Chevron, but we have grown cautious on shares given its recent acquisitive activity. Still, its dividend yield of ~4.1% isn’t shabby by any stretch.

New York Community Bancorp (NYCB) Cuts Dividend By 70%+

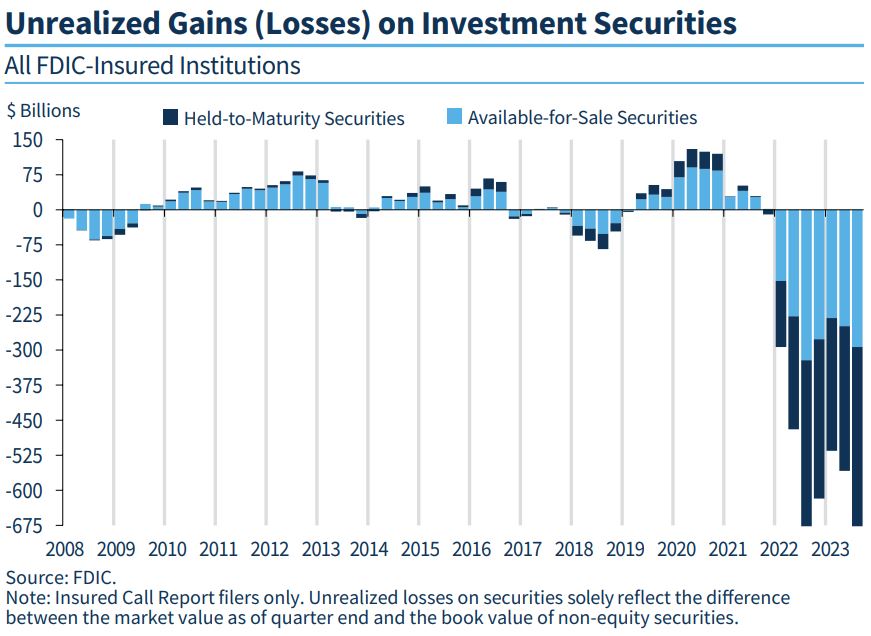

Image Source: FDIC. “Unrealized losses on securities totaled $683.9 billion in third quarter, up $125.5 billion (22.5 percent) from the prior quarter, primarily due to an increase in mortgage rates that reduced the value of mortgagebacked securities. Unrealized losses on held-to-maturity securities totaled $390.5 billion in the third quarter, while unrealized losses on available-for-sale securities totaled $293.5 billion.” — FDIC Quarterly

We continue to pound the table on the “4 Very Good Reasons Why We Don’t Like Dividends of Banking Stocks:” Reason #1: A Bank Run Is Always Possible. Reason #2: Others Have Tried to Invest in Bank Dividends and Have Failed. Reason #3: Cash Flow Is Not Meaningful at Banks. Reason #4: There Are Plenty of Other Options. When the bank reported fourth-quarter results for 2023 on January 31, the company put up a fourth-quarter net loss of $260 million due to a reserve build (it recorded a $552 million provision for credit losses in the fourth quarter), while its fourth-quarter net interest margin contracted by 45 basis points due in part to a higher cost of deposits. New York Community Bancorp also slashed its payout by more than 70%, to a quarterly rate of $0.05 per share. The Fed’s aggressive rate-hiking cycle has put the backs of many regional banks (KRE) against the wall, as unrealized losses on investment securities for the group mount (as shown in the image above). We’re not interested in any banking entity at the moment, and we continue to prefer ideas in the newsletter portfolios.

Exxon Mobil (XOM) Ends Strong 2023; Dividend Coverage Remains Solid

On February 2, Exxon Mobil reported mixed fourth-quarter results that revealed a miss on the top line, but a nice beat with respect to non-GAAP earnings per share. Fourth-quarter results were messy with an impairment charge and tax and divestment-related items, but the headline for Exxon Mobil’s full year performance was impressive: “Delivered industry-leading 2023 earnings of $36.0 billion, generated $55.4 billion of cash flow from operating activities and distributed $32.4 billion to shareholders.” Exxon Mobil also drove Guyana and Permian production 18% higher on the year, while it delivered record refinery throughput. The energy giant noted that it had achieved $9.7 billion in cumulative structural cost savings in 2023 versus 2019 and that it will look to deliver cumulative savings totaling $15 billion through the end of 2027. Exxon Mobil remains a free cash flow generating giant and hauled in ~$33.45 billion in free cash flow during 2023, lower than 2022 levels due to operating cash flow declines, but still in excess of the cash dividends paid to shareholders. As with Chevron, the newsletter portfolios benefited greatly from the strength in energy-sector equities, including Exxon Mobil, during 2022, but we’ve since moved beyond that tactical play. Shares of Exxon Mobil yield ~3.7% at the time of this writing.

—–

NOW READ: 12 Reasons to Stay Aggressive in 2024

NOW READ: 2023 Was a Fantastic Year! Are You Ready for 2024?

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.