Booking Holdings, formerly Priceline, reported solid second-quarter 2019 results. We continue to believe this Best Ideas Newsletter portfolio holding is undervalued. Our fair value estimate stands at ~$2,130+.

By Brian Nelson, CFA

Booking Holdings (BKNG), formerly Priceline, was added to the Best Ideas Newsletter portfolio in February 2015, registering a 10 on the Valuentum Buying Index at the time, at ~$1,240 per share. Shares of the company are soaring during the trading session August 8 on news of a strong second-quarter report. Shares currently trade hands for ~$1,950 each.

For some of our new members that may not be familiar with Booking Holdings, the company operates the “world’s leading brand for booking online accommodation reservations,” Booking.com. It also operates KAYAK (an online travel price comparison service), priceline.com (an online travel reservation service), agoda, Rentalcars.com, and OpenTable. The firm generates revenue primarily from commissions on facilitating reservations of travel and related services (it also generates sales from advertising and ancillary means).

The online travel reservation space is a competitive one, and such rivals include Expedia (EXPE), Hotels.com, Hotwire, Orbitz, Travelocity, Wotif, Cheaptickers and others. Some of the biggest online tech giants also pose risk to the large economic returns that current reside in this asset-light business. What we think differentiates Booking Holdings are 1) its relative first mover advantage (it was formed in 1997, prior to the dot-com bust), which has facilitated customer familiarity and trust, 2) its expansive partnership network with travel service providers, and 3) its diverse brand portfolio.

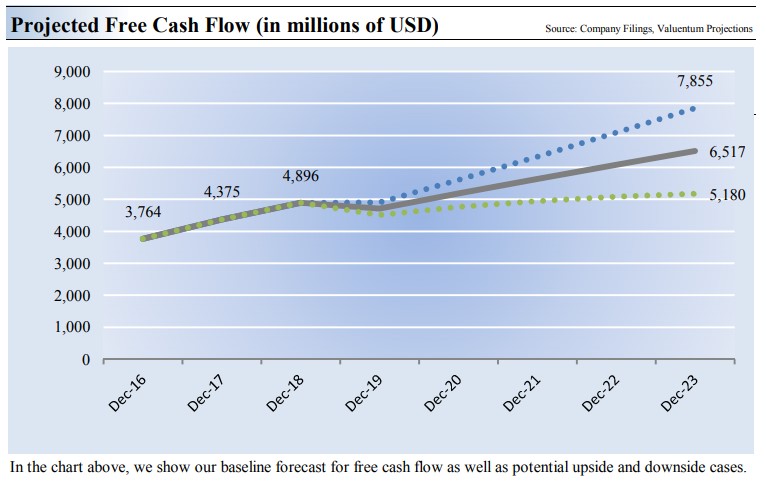

Image Source: Valuentum’s forecasts for Booking Holdings’ free cash flow.

What we absolutely love about Booking Holdings is its enormous free-cash-flow generation. Let’s put the company’s rate of free cash flow conversion in perspective. During 2018, Booking Holdings generated revenue of $14.5 billion, while it hauled in ~$4.9 billion in free cash flow, good enough for a free-cash-flow margin (free cash flow divided by sales) of ~34%. The company operates an extremely asset-light business model, with annual run-rate capital spending in the $400-$500 million range. Return on invested capital is tremendous.

During Booking Holdings’ second-quarter 2019 report, gross bookings advanced ~5%, coming in better than expected. On a constant-currency basis, bookings increased 10% during the period. The firm’s adjusted EBITDA rose to $1.37 billion, beating the consensus estimate handily. For the third quarter of this year, adjusted EBITDA is expected to fall in the range of $2.4-$2.45 billion. Free cash flow generation came in at ~$1.7 billion during the first six months of the year. Here’s what management had to say about business conditions during the second-quarter call:

We are seeing encouraging signs in our business as we extended our global leadership position and accommodations and continued to execute against our long-term strategic vision of building a connected trip for our customers to become the global leader in travel and experiences.

Today, we operate the largest online marketplace for accommodations, with the greatest global reach and scale. In the first half of the year, we produced over $50 billion in gross bookings and over 430 million booked room nights. We’re investing against a large opportunity in the global accommodations market and are developing capabilities like payments, merchandising and loyalty, and expanding our focus in important customer and geographic segments.

Booking Holdings ended the second quarter of 2019 with $11.4 billion in cash and cash equivalents, short-term investments in marketable securities, and long-term investments. Long-term and convertible debt was $8.7 billion, so Booking Holdings holds a nice net cash position, as it generates copious amounts of free cash flow. Net cash on the books and future expected free cash flow generation are two of the most important components of intrinsic value.

Concluding Thoughts

We are reiterating our opinion that shares of Best Ideas Newsletter portfolio holding Booking Holdings are undervalued, based on a price-to-fair value estimate comparison. The stock has been a huge winner in the Best Ideas Newsletter portfolio during the past four years, and we believe there is further upside to come on the basis of our fair value estimate.

Related: CTRP, RCL, NCLH, DESP, HGV, VAC, CCL, TRIP, TRVG

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.