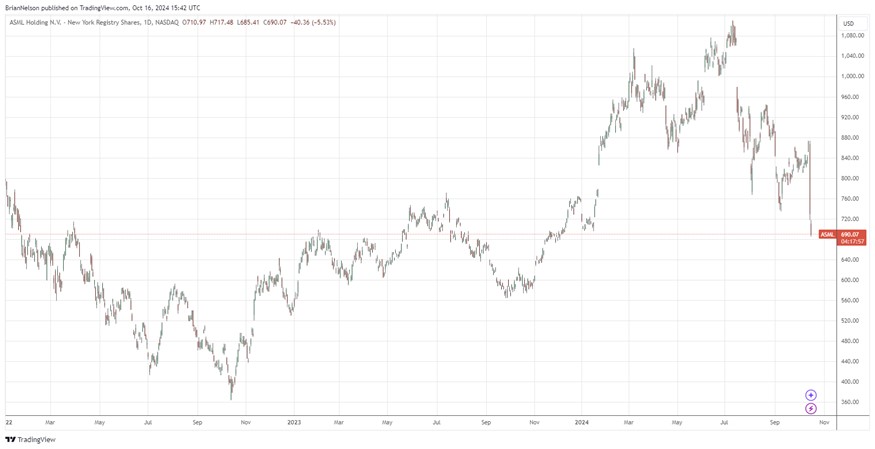

Image: ASML Holding is falling from recent highs as its third quarter report and outlook disappointed investors.

By Brian Nelson, CFA

On October 15, ASML Holding (ASML) reported disappointing results for the third quarter of 2024, as the firm’s quarterly net bookings were weaker than the market was expecting. Third quarter total net sales were €7.5 billion (better than consensus of €7.17 billion), while it put up a gross margin of 50.8%, resulting in net income of €2.1 billion in the quarter (better than consensus of €1.91 billion). The big news, however, was that net bookings in the third quarter were €2.6 billion versus consensus expectations of €5.39 billion. Management had the following to say about the quarter, adjusting its 2025 outlook:

While there continue to be strong developments and upside potential in AI, other market segments are taking longer to recover. It now appears the recovery is more gradual than previously expected. This is expected to continue in 2025, which is leading to customer cautiousness. Regarding Logic, the competitive foundry dynamics have resulted in a slower ramp of new nodes at certain customers, leading to several fab push outs and resulting changes in litho demand timing, in particular EUV. In Memory, we see limited capacity additions, with the focus still on technology transitions supporting the HBM and DDR5 AI-related demand.

We expect fourth-quarter total net sales between €8.8 billion and €9.2 billion with a gross margin between 49% and 50% which includes the recognition of the first two High NA systems upon customer acceptance, reflecting progress on imaging, overlay and contrast. ASML expects R&D costs of around €1.1 billion and SG&A costs of around €300 million. We expect full-year 2024 total net sales of around €28 billion. Based on the recent market dynamics as mentioned above, we expect our 2025 total net sales to grow to a range between €30 billion and €35 billion, which is the lower half of the range that we provided at our 2022 Investor Day. We expect a gross margin between 51% and 53%, which is below the range we then provided, mainly related to the delayed timing of EUV demand.

ASML’s guidance for 2025 came in below what consensus had been looking for. 2025 net sales are now expected in the range of €30 billion and €35 billion, which compares to guidance of €30 billion to €40 billion previously and the consensus estimate of €35.94 billion. The company’s updated gross margin outlook for 2025 in the range of 51%-53% is below the 54%-56% it had previously forecast and below the consensus estimate of 53.9%. The bookings number in the third quarter coupled with lowered 2025 guidance is weighing on the stock. Though the news isn’t great, we continue to like ASML Holding as a long-term idea in the ESG Newsletter portfolio.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.