By Brian Nelson, CFA

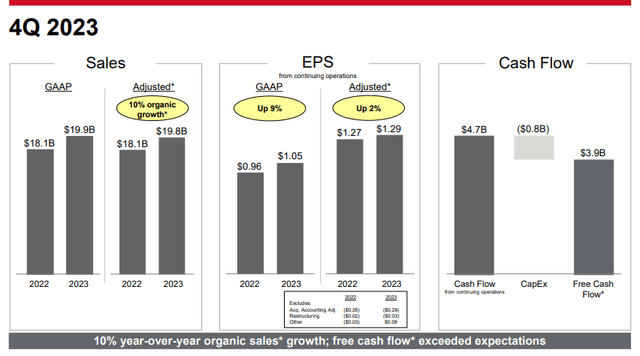

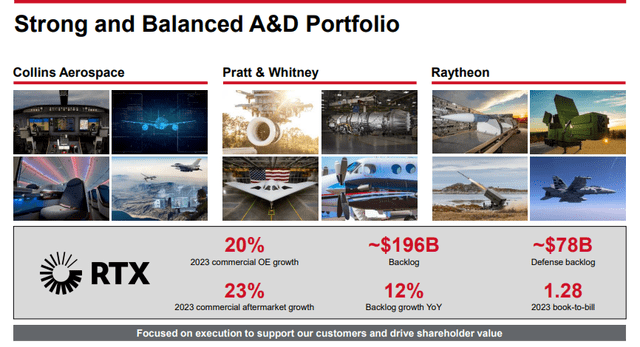

Back in late January, RTX (RTX), formerly Raytheon Technologies, reported solid fourth-quarter results, beating on both the top and bottom lines. Adjusted sales advanced 10% from the prior year, while adjusted earnings per share edged 2% higher, to $1.29. For the fourth quarter, the company hauled in $4.7 billion in operating cash flow and generated $3.9 billion in free cash flow. RTX ended the year with record company backlog of $196 billion, with $118 billion attributable to commercial and the balance to defense.

Image Source: RTX

Management noted the firm is off to a good start in 2024 in the press release:

RTX reported solid full-year results, delivering 11 percent organic sales growth and $5.5 billion in free cash flow for the year, exceeding our expectations. Across our portfolio, we supported the continued recovery in commercial aerospace and provided critical platforms and advanced technologies to our customers, achieving $95 billion in new awards and ending the year with a record backlog of $196 billion.

RTX is beginning 2024 with strong momentum and we are projecting another year of strong sales growth and continued segment margin expansion. The financial and operational outlook of our GTF fleet management plans remain consistent from October and continues to be a top priority as we focus on driving performance across all three businesses to support our customers and deliver shareowner value. With the execution of our $10 billion accelerated share repurchase program, we’ve delivered over $29 billion to shareowners since the merger, achieving significant progress toward our capital return commitment of between $36 – $37 billion through 2025.

Image Source: RTX

Image Source: RTX

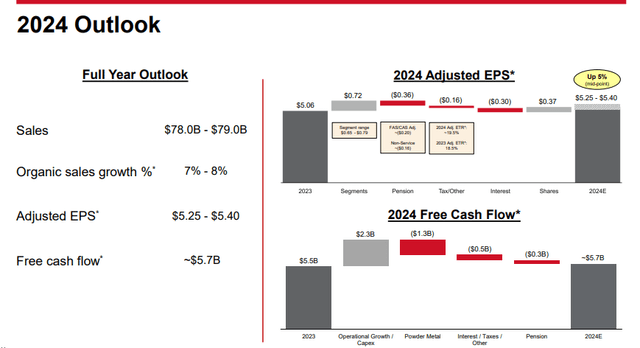

Looking ahead to its full year outlook for 2024, RTX expects sales in the range of $78-$79 billion, slightly lower than the consensus forecast at the time, and adjusted earnings per share in the range of $5.25-$5.40, the midpoint of which was higher than the consensus forecast, with free cash flow generation of ~$5.7 billion. Management also reaffirmed its 2025 free cash flow commitment of ~$7.5 billion, revealing considerable free cash flow growth potential.

Image Source: RTX

With the Russia-Ukraine war and the Israel-Hamas wars still raging, geopolitical tensions continue to be elevated, playing into the hands of defense contracts such as RTX. With an attractive commercial portfolio to boot, RTX is poised to continue to capitalize on both original equipment and higher-margin after-market commercial aerospace sales, too. We’re fans of RTX, and the firm looks to be moving past a costly recall associated with its Pratt & Whitney geared turbofan engines. Shares yield ~2.4% at this time.

———-

Tickerized for RTX, GD, BA, NOC, GE, HON, ITA, PPA

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.