Image Source: Ameresco Inc – First Quarter of 2022 Earnings Press Release

By Callum Turcan

The rise of ESG investing and the political shift towards encouraging developments within the realm of green energy–from renewable energy projects to efforts to reduce water consumption and much more–has created numerous opportunities for investors. Ameresco Inc (AMRC) offers energy efficiency solutions, infrastructure upgrades, and renewable energy solutions to its customers. The company also operates some of the renewable energy facilities it helps develop such as solar farms and biogas plants.

Ameresco provides its services all over the globe though the US remains its most important market (and the source of over 90% of its revenues). In the US, Ameresco will often help its clients secure the financing needed to fund relevant projects, particularly for its federal government customers.

We include Ameresco as an idea in the ESG Newsletter portfolio (more on that publication here) and view its capital appreciation upside favorably. Due to Ameresco utilizing energy savings performance contracts (‘ESPC’), its financials can be a messy read. ESPCs enable its governmental customers in the US to finance infrastructure upgrades without needing to tap their capital budgets by taking advantage of the expected future energy cost savings. The company generally experiences large working capital builds on an annual basis due to growth in its federal ESPC receivables asset, a product of Ameresco’s overall business growing, making gauging its free cash flows a more difficult task.

Earnings Update

On May 2, Ameresco reported first quarter 2022 earnings that smashed past consensus top- and bottom-line estimates. Its GAAP revenues rose 88% year-over-year to reach $474 million as its project revenue surged higher 118% year-over-year, with Ameresco benefiting from a major contract with Southern California Edison (‘SCE’), a unit of Edison International (EIX). Ameresco is designing and developing three battery energy storage systems (‘BESS’) for Edison International that are “grid scale” and intended to support California’s push to develop renewable energy sources, which for wind and solar farms are intermittent sources of power supply. These batteries can provide power to the grid when the sun is not shining and the wind is not blowing.

Something that has been hanging over Ameresco’s head is delays concerning the BESS contract due to coronavirus (‘COVID-19’) lockdowns in China. Though Ameresco has made substantial progress on the project, the firm is “expecting delays in the delivery of certain batteries due to the COVID-19 lockdowns in several regions around China and newly implemented Chinese transportation safety policies,” according to its earnings press release.

Additionally, “under the SCE contract, Force Majeure events, including COVID-related delays, result in extensions of required completion deadlines without liquidated damages and the contract price may be increased to account for the impact of the Force Majeure event.” By August 2022, Ameresco intends to have 300 MW of battery storage capacity up and running out of 537.5 MW of total expected capacity, with the remainder expected to come online this year.

Last quarter, Ameresco’s GAAP operating income rose 57% year-over-year to reach $29 million as it benefited from its revenues swelling higher, which was offset to a degree by sharp increases in its operating expenses. Ameresco generated $0.36 in non-GAAP adjusted EPS last quarter, up 44% year-over-year. The company’s non-GAAP adjusted EBITDA, one of its preferred metrics when it comes to citing its cash flow performance (though this non-GAAP metric that has plenty of flaws), rose 52% year-over-year to hit $45 million in the first quarter.

Promising Growth Outlook

Ameresco exited March 2022 with $3.1 billion in total project backlogs consisting of $1.8 billion in awarded projects (that have not been signed yet) and $1.3 billion of contracted projects. The company’s development pipeline is robust. It also had 353 MWe of operational energy assets and 464 MWe of energy assets in development along with $1.2 billion in O&M revenue backlog at the end of March 2022. Some of Ameresco’s recent wins include a $102 million energy conversation project and a 25-year $95 million O&M service agreement at the Joint Base Pearl Harbor-Hickam Air Force Base in Hawaii and the 20-year LEAP project aimed at decarbonizing the city of Bristol in the UK.

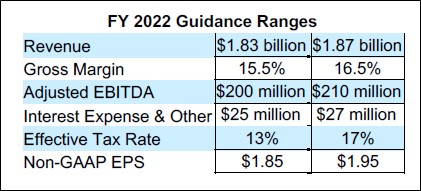

These wins combined with Ameresco’s stellar operational execution of late enabled it to reaffirm its guidance for 2022 during its latest earnings update. Ameresco aims to generate 52% annual revenue growth, 34% annual adjusted EBITDA growth, and 26% adjusted EPS growth at the midpoint of its guidance this year. For all of 2022, Ameresco aims to place 60 MWe to 80 MWe of energy assets into service.

Image Shown: A snapshot of Ameresco’s full-year guidance for 2022 which calls for nice double-digit annual revenue and adjusted EBITDA growth. Image Source: Ameresco – First Quarter of 2022 Earnings Press Release

Ameresco expects its gross margin performance will steadily improve throughout 2022. In the first quarter of 2022, Ameresco’s GAAP gross margin stood at 14.4%, down from 18.6% in the first quarter of 2021. Inflationary pressures are taking a toll, and the company is adapting accordingly. This quarter, Ameresco expects its gross margin will come in around 14% before rising to roughly 18% in the third and fourth quarters of this year. Ameresco’s ability to utilize its pricing power to improve its margins going forward highlights one of the reasons why we are big fans of the company.

We caution that Ameresco had a net debt load of ~$672 million (inclusive of short-term debt and finance lease liabilities, exclusive of restricted cash) at the end of March 2022. The firm has been able to tap capital markets at attractive rates in the recent past, and we expect that will continue to be the case going forward.

In March 2022, Ameresco amended its senior secured credit facility covering its revolving credit facility and term loans. Among other things, these changes included increasing the aggregate total commitments to $495 million (versus $245 million previously) and extending the maturity date of Term Loan A and the revolving credit facility to March 2025 (versus June 2024 previously). Ameresco has ample access to liquidity when considering its revolving credit facility and its $68 million cash and cash equivalents position at the end of the first quarter of 2022.

We will also caution here that Ameresco generated negative net operating cash flows in the first quarter, though again that is not indicative of its underlying financial performance and is primarily a function of the nature of ESPCs (which interested members can read more about here).

Concluding Thoughts

Supply chain hurdles and inflationary pressures remain a concern, though Ameresco has done a solid job navigating those headwinds as best as the company reasonably can. Ameresco is a rock-solid enterprise with a promising growth outlook and ample pricing power backed up by a large project backlog. Looking ahead, Ameresco should continue to benefit immensely from the “green energy revolution” and we appreciate its global footprint as it puts the firm in a better position to capitalize on government-led efforts to decarbonize regional and national economies. We continue to like Ameresco as an idea in the ESG Newsletter portfolio.

—–

Disruptive Innovation Industry – W, ZM, SPCE, ROKU, WORK, MNST, SAM, SPLK, PENN, VRSK, ICE, LULU, DOCU, ESTY, UBER, BYND, SFIX, CVNA, TER, GPN, PANW, VRSN, MELI, PRLB, FSLR, JD, CRSP, PINS, NDAQ, FVRR, SNAP, GME, CROX, NOW

Utilities (Large) Industry – AEP, D, DUK, ED, EIX, ETR, EXC, FE, NEE, NGG, PCG, PPL, SO, XEL

Utilities (Mid/Small) Industry – AEE, ALE, CNP, CMS, DTE, ES, LNT, MGEE, NI, PEG, PNW, SCG, SJI, SR, SRE, WEC

Tickerized for AMRC, RSG, STEM, EIX, DUK, ENGIY, XLU

Callum Turcan owns shares of DIS, FB, GOOG, VRTX, and XLE and is long call options on DIS and FB. Utilities Select Sector SPDR Fund (XLU) is included in Valuentum’s simulated High Yield Dividend Newsletter portfolio. Ameresco Inc (AMRC) and NextEra Energy Inc (NEE) are both included in Valuentum’s simulated ESG Newsletter portfolio. Republic Services Inc (RSG) is included in both Valuentum’s simulated Dividend Growth Newsletter portfolio and simulated ESG Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.