Image Source: Albemarle

By Brian Nelson, CFA

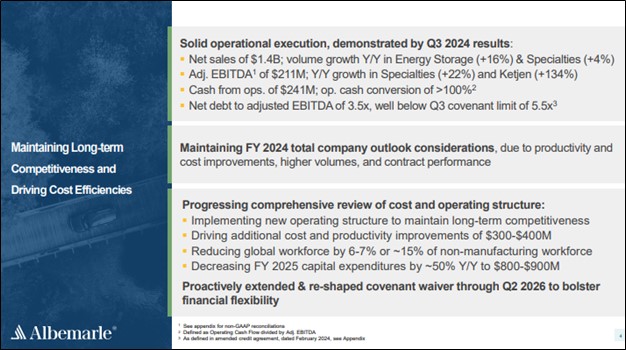

On November 6, Albemarle (ALB) reported mixed third quarter results with revenue outpacing the consensus forecast, but non-GAAP earnings per share coming up a bit short. Net sales fell to $1.36 billion from $2.3 billion in the year-ago period as a result of depressed lithium prices, while adjusted EBITDA came in at $211 million versus $653 million in the same period last year. Its adjusted EBITDA margin fell 1,200 basis points in the quarter on a year-over-year basis, while adjusted diluted loss per share was $1.55.

Management had the following to say about results:

Our steadfast focus on execution allowed us to deliver solid third-quarter results and maintain our full-year 2024 corporate outlook considerations as cost improvements, higher volumes, and the performance of our long-term contracts offset lower market pricing. Through our strategic review of Albemarle’s cost and operating structure, we have identified significant opportunities to reduce cost, improve productivity and decrease capital spending while ensuring we efficiently serve customers and our end-markets. These actions are designed to increase Albemarle’s financial flexibility, strengthen our core capabilities and position the company to maintain its leadership position long-term.

In the quarter, Albemarle’s volumes in Energy Storage and Specialties increased 16% and 4%, respectively. Specialties adjusted EBITDA advanced 22% year-over-year while Ketjen adjusted EBITDA increased 134% year-over-year. Thanks in part to favorable working capital management, cash flow from operations came in at $241 million. Year-to-date cash flow from operations was $701 million, a decline of $722 million from the same period a year ago. The company maintained its full-year outlook thanks in part to cost savings, increased volumes, and the performance of long-term contracts.

The company is maintaining its prior full-year 2024 outlook considerations, which are based on observed lithium market price scenarios. The previously published $12-15/kg range is expected to apply even when assuming recent market pricing persists for the remainder of the year, due to enterprise-wide cost improvements, strong volume growth, and Energy Storage contract performance. Total company full-year 2024 net sales are expected to be at the lower-end of that range ($5.5-$6.2 billion) due to lower recent market pricing. Full-year adjusted EBITDA is expected to be towards the middle of that range ($0.9-$1.2 billion), driven by productivity and cost benefits and higher equity income.

Albemarle is working hard in the face of weak lithium pricing, and the firm is driving cost and productivity improvements across its business. The firm noted that it is reducing its workforce by 6%-7%, which will help the company cut costs in the range of $300-$400 million, and it plans to decrease its fiscal 2025 capital spending by roughly half versus fiscal 2024 ($1.7-$1.8 billion), to an expected range of $800-$900 million. Total liquidity was $3.4 billion at the end of the quarter, including $1.7 billion in cash equivalents, while total debt was $3.6 billion. We continue to include Albemarle in the ESG Newsletter portfolio.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.