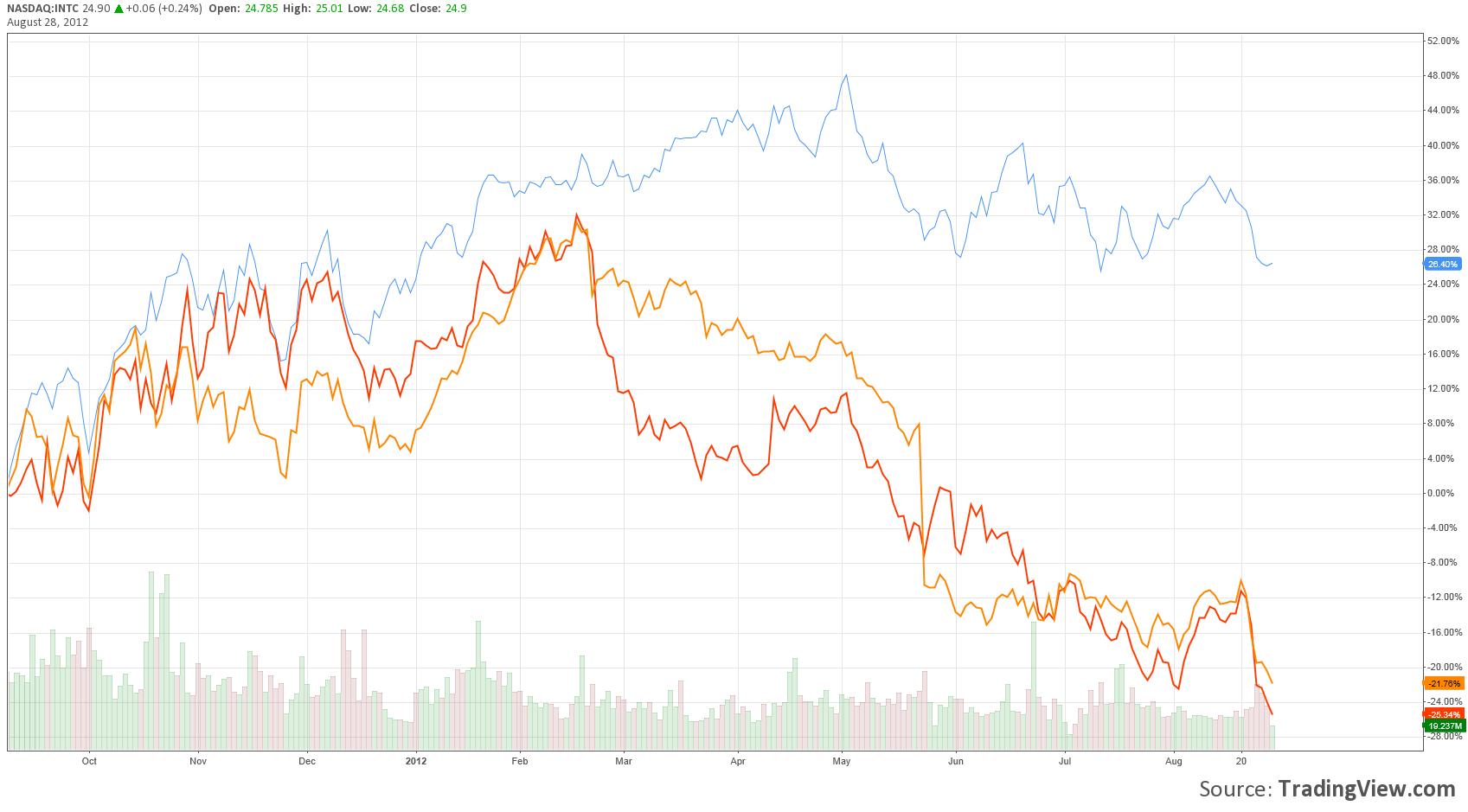

Though advancing more than 25% since we added it to the portfolio of our Best Ideas Newsletter, Intel (click ticker for report: ) has retreated from highs achieved a number of weeks ago. Given the recent fundamental issues at its two biggest clients, Hewlett Packard (click ticker for report: ) and Dell (click ticker for report: ), we wanted to offer our current line of thinking on Intel and reveal its relative outperformance (the blue line in the chart below). Hewlett Packard’s and Dell’s performance during the same time period is displayed in the red and orange lines, respectively.

Though clearly not as drastic as the significant declines its peers have experienced, Intel’s 25%+ positive performance has understandably not been as robust as some of our other tech picks in our Best Ideas portfolio – namely eBay (click ticker for report: ), which has advanced 50%, and Apple (click ticker for report: ), which has roughly doubled. With PC shipments slowing, expected now to grow just 0.9% year-over-year for 2012, Intel will continue to face some headwinds, in our view, unless Windows 8 (click ticker for report: ) becomes an immediate blockbuster hit. Though it’s hard to think the operating system will completely reverse slowing expansion in PC shipments, we’re not ready to give up on Windows 8 (and view the new platform as a legitimate catalyst for shares). In fact, we think a Windows 8 bust appears to be priced fully into Intel’s shares (presenting opportunity for investors).

Though clearly not as drastic as the significant declines its peers have experienced, Intel’s 25%+ positive performance has understandably not been as robust as some of our other tech picks in our Best Ideas portfolio – namely eBay (click ticker for report: ), which has advanced 50%, and Apple (click ticker for report: ), which has roughly doubled. With PC shipments slowing, expected now to grow just 0.9% year-over-year for 2012, Intel will continue to face some headwinds, in our view, unless Windows 8 (click ticker for report: ) becomes an immediate blockbuster hit. Though it’s hard to think the operating system will completely reverse slowing expansion in PC shipments, we’re not ready to give up on Windows 8 (and view the new platform as a legitimate catalyst for shares). In fact, we think a Windows 8 bust appears to be priced fully into Intel’s shares (presenting opportunity for investors).

In addition to pricing in poor Windows 8 performance, the market has also grown worried about Intel’s position in the mobile market. The results of Dell and HP both confirm that tablets are becoming a substitute product, especially for notebooks, so Intel’s entrance into the market will be integral to its long-term success. Though the firm doesn’t have the same presence as ARM Holdings (ARMH), tech magazine Wired offers a detailed profile of Intel’s current position in mobile chips. Essentially, the market is more competitive, offers lower margins, and consumers seem to care less about these chips than they do about PC chips. Still, we wouldn’t be shocked to see Intel make a splash, especially given the legal battle between Apple (click ticker for report: ) and Samsung, as well as the firm’s absolutely massive research and development budget.

Investors should be aware of the market’s outlook on the company given PC industry weakness and expect the next quarter to be difficult (in fact, we would not be surprised if Intel misses consensus expectations on the top line). Still, the company registers a 9 on the Valuentum Buying Index (our stock-selection methodology) and looks incredibly cheap based on our discounted cash-flow process. And it’s important to note that not all of the firm’s business lines are under pressure. The firm’s Data Center Group grew revenue 15% during the most recent quarter, and Intel continues to grow its Software and Services Group at a similar clip. With an annual dividend yield of 3.6% and downside largely priced in, we continue to hold the firm in our actively-managed portfolios. The firm has raised its dividend payout three times in the past 18 months, and we reiterate our view that Intel has significant room for further dividend increases (at a low-double-digit annual pace in coming years) based on our Valuentum Dividend Cushion measure. At this point, we think most of the tail risk (Windows 8 success, Apple iPhone/iPad deal) at Intel is to the upside.