Image Source: Altria

By Brian Nelson, CFA

Altria (MO) reported better than expected fourth quarter results on January 30, with both revenue and non-GAAP earnings per share exceeding the consensus forecasts. Revenue, net of excise taxes advanced 1.6%, while adjusted diluted earnings per share came in at $1.29, up more than 9% on a year-over-year basis.

NJOY consumables reported shipment volume advanced 15.3% in the quarter, while NJOY devices reported shipment volume increased 22.2%. In its Smokeable Products segment, net revenues fell 0.2% due to lower shipment volume, partially offset by higher pricing, while adjusted segment operating companies income (OCI) increased 5.5%. In its Oral Tobacco Products segment, net revenue increased 2.7% driven by higher pricing, while segment adjusted OCI increased 13%.

Management had the following to say in the press release:

2024 was another pivotal year for Altria, headlined by meaningful progress toward our Vision, strong financial results and significant cash returns to shareholders. Our companies’ leading brands and talented teams enabled our core tobacco businesses to deliver solid income growth and margin expansion, while we strategically invested in our future.

In the fourth quarter, the company repurchased 5.8 million shares for a total cost of $310 million. For the full year, Altria bought back 73.5 million shares for a total cost of $3.4 billion. The board authorized a new $1 billion share repurchase program, which is expected to be completed by the end of 2025. Altria paid dividends of $1.7 billion in the fourth quarter and $6.8 billion for the full year.

Altria’s 2028 Enterprise Goals are noteworthy. The company expects to deliver a mid-single digits adjusted diluted earnings per share compound annual growth rate in 2028 from a $4.84 base in 2022. Altria targets a progressive dividend goal of mid-single digits dividend per share growth annually through 2028. The company targets a debt-to-consolidated EBITDA ratio of 2.0x and to maintain its leadership position in the U.S. tobacco space with core brands Marlboro, Copenhagen and Black & Mild. Management also wants to maintain a total adjusted OCI margin of at least 60% in each year through 2028.

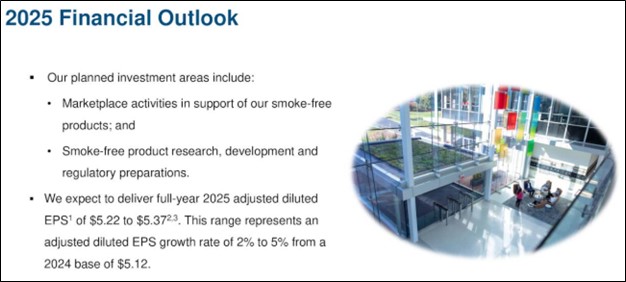

Altria ended the year with $3.1 billion in cash and cash equivalents and $24.9 billion in debt. Looking to 2025, Altria expects to deliver full-year adjusted diluted earnings per share in a range of $5.22-$5.37, which reflects a growth rate of 2%-5% from a base of $5.12 in 2024. Management expects 2025 capital expenditures to be between $175-$225 million. Though Altria’s 2025 outlook came in lower than expected, we like the firm’s pricing power and income generation potential with a forward estimated yield of 7.8%.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, QQQM, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, QQQM, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.