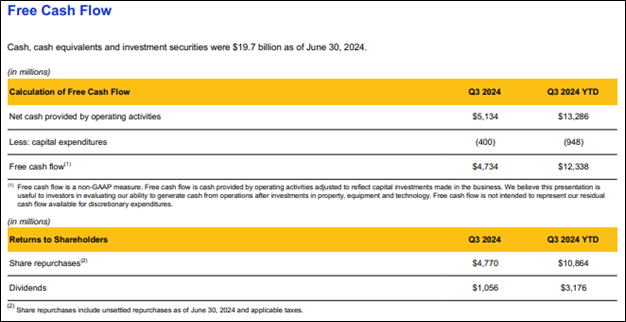

Image: Visa’s asset light business model throws off a lot of free cash flow, while the firm returns cash to shareholders via buybacks and dividends.

By Brian Nelson, CFA

On July 23, Visa (V) reported mixed fiscal third quarter results with the company missing expectations on the top line and the firm’s non-GAAP earnings per share coming in-line with the consensus forecast. We’re not reading too much into the company’s mixed fiscal third quarter results and remain fans of the company’s competitive positioning and asset light business model.

During the quarter, net revenue advanced 10%, while GAAP net income increased 17% and GAAP earnings per share increased 20% on a year-over-year basis. On a non-GAAP basis net income increased 9%, while earnings per share increased 12% from last year’s quarter. On a constant-dollar basis, GAAP earnings per share increased 22%, while non-GAAP earnings per share growth was 13% on a constant-dollar basis. Payments volume increased 7% in the fiscal third quarter, while cross border volumes increased 14% and processed transactions increased 10%, all on a constant-dollar basis.

Visa pays a healthy dividend, and the company bought back $4.8 billion worth of stock during the June quarter. It has $18.9 billion remaining under its authorized buyback program as of the end of June. Total cash and investment securities totaled $19.7 billion at the end of the quarter, while long-term debt was $20.6 billion, revealing a modest net debt position. For the nine months ended June 30, cash flow from operations fell to $13.3 billion from $13.8 billion in the year ago period, while free cash flow dropped to $12.3 billion from $13.1 billion in the same period a year ago.

Looking to the fourth quarter of fiscal 2024 and for all of fiscal 2024, net revenue growth is still expected in the low double-digit range. Operating expense growth is expected in the high single-digit range for the fiscal fourth quarter and the high single-digit to low double-digit range for the full-year 2024. It had expected operating expense growth in the low double-digit range for fiscal 2024 previously. For the fourth quarter, diluted class A earnings per share growth is expected in the high end of low double-digit growth, while low-teens growth is expected for the full-year 2024, in-line with its prior forecast.

—–

NOW READ: 12 Reasons to Stay Aggressive in 2024

NOW READ: 2023 Was a Fantastic Year! Are You Ready for 2024?

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.